Q1 generally remains lean for construction equipment sector. You can check the past sales data also.

1 Like

ACE will now go into time correction in my opinion because their products are bought more in the first phase of any capex cycle.

1 Like

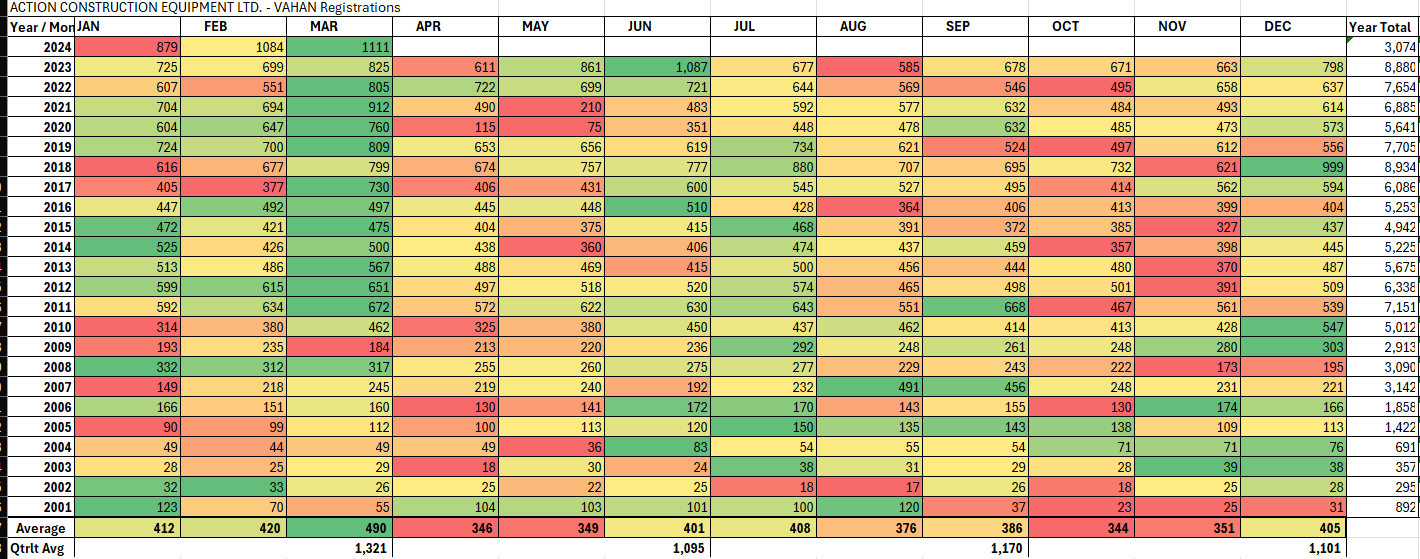

The below is a monthly VAHAN registrations that i have been tracking for ACE. You will notice (last two rows in image), that APR, MAY, OCT and NOV are the months when sales are usually down.

MAR is usually a peak in most years. JAN-MAR quarter is always the best, APR-JUN is the lowest in terms of registrations.

- Please note VAHAN registrations is just an indicator, actual sales might vary since there could be some equipment (non road) that will not be VAHAN registered.

Will the dip be a buying opportunity, we need to watch for next few months. For some reason last 1 year, the HOLD approach has worked out in most counters due to followup factors.

9 Likes

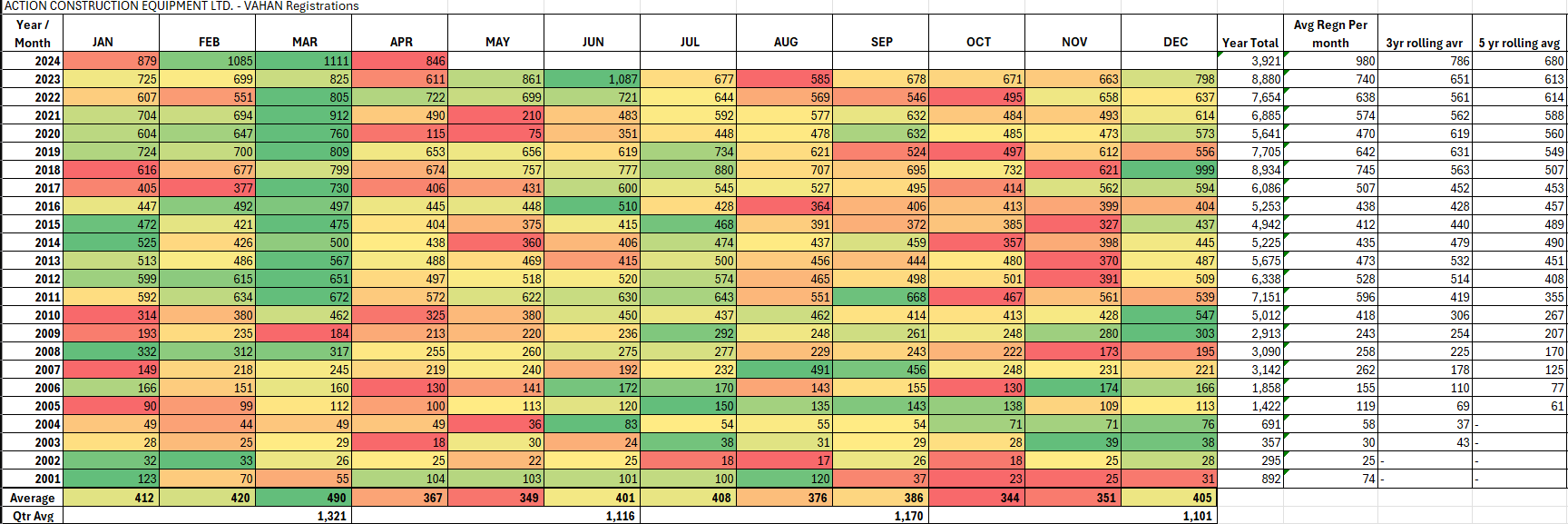

Even by Vahan regs, FY25 April is highest till date they have done in an April month of any year.

4 Likes

VAHAN regn as of 1st May.

Apr’24 is lower MoM, but is the highest ever Apr month VAHAN Regn. Seasonal trend seems to have kicked in, with lower volumes in Apr-Jun qtr. If Apr/May Regn volumes are a bottom kind of figure, it still works out great for ACE in FY25, time will tell. On target to cross 10K Regn for CY 2024.

The other updates on 80 Acre land acquisition, capex, defence orders, etc might have to be seen from company for valuation upside.

Do Note VAHAN Regn will be directly related to ACE sales numbers, but will not capture non-road equipment sales.

5 Likes

Anyone knows what initiatives ACE is taking to increase its share in the backhoe loader segment?

JCB used to be my client & I know they do close to 12k crs revenue from India - mainly from backhoe loaders. The market size just for backhoe loaders today would easily be around ~$2bn given JCB’s market share of around 60-70%

All that I noticed in ACE’s presentation on backhoe loaders was focus on distribution but focus on tech?

2 Likes

From LinkedIn it is evident they’ve sold about 25 backhoe loaders as of Sep’23 i.e. in H1. I’ve got not clue as to the how much each of those contribute to revenues though ![]()

4 Likes

ACE declared the FY24 results today.

FY24 NP at 328 Cr vs 172Cr in FY23. EPS is Rs.27.5 Vs Rs 14.4.

Q4FY24 NP at 98 Cr vs 51.99Cr in Q4FY23.

Link: Action Construction - FY24 Results

Need to see the conference call updates from mgmt on order book. As of now, results seem to be inline, but maybe Rs.1-2 below what market was building. Company has done really well in Q4, but from VAHAN numbers we are going to see degrowth (for MoM or QoQ numbers, YoY it is better). Can mgmt assure that they do see a reliable order pipeline to compensate for reduce VAHAN numbers?

1 Like

@ashwind - If you see volume for ACE in VAHAN for last 6 years too, in 5 out of 6 years April registrations for ACE has been significantly lower as compared to January or March of same calendar year.

I dont think it is degrowth, but kind off pattern. This April’s registration has just been 3-4% lower than Jan’24.

2 Likes

Your own number of vehicle registration for Apr-23 is 699 whereas for Apr-24 is 861 which is a growth of 23% YoY. What kind of de-growth are you talking about?

May’24 is likely to be a degrowth both on a MoM and a YoY basis… if not YoY, then a low single digit growth. I do expect PE derating unless they come up with some explanation.

Given the elections and also the seasonality one can expect the slowdown in Q1 but if you look at the CWIP and Capex this year it does point towards a very strong outlook for the company. In terms of de-rating, a stock which can provide you 30%+ EPS CAGR for next two year with a net cash balance sheet and RoE of 25%+ paying mid 30’s is not bad for an Industrials stock.

4 Likes

Hey, on the market numbers it does look like they have exceeded EPS expectation by 6 off %. Market was asking for 25.9 vs they delivered 27.6%. There should be potential upgrades for FY25/F26EPS too given the better base now.

3 Likes

True. After today’s result, P/E has fallen about 15% from 67 to 57. I expect it to go back to 65-70 range in a week’s time.

That would be about 1750-1850 range.

ESOP Filing Company has Employee Stock Options (“Options”) plan with a exercise price of Rs.1450/share, 1/3rd vesting every year. Interesting to see which level of employees this is being offered to. My understanding is that Employees will find this interesting/profitable if the price remains above (hopefully significantly) Rs.1450 (during each exercise period i.e. May 2025/26/27), since they have to pay the exercise price.

Maybe a indicator of mgmt expectation of company performance (indirectly translating to stock price) in coming years.

Link : ESOP Announcement

1 Like

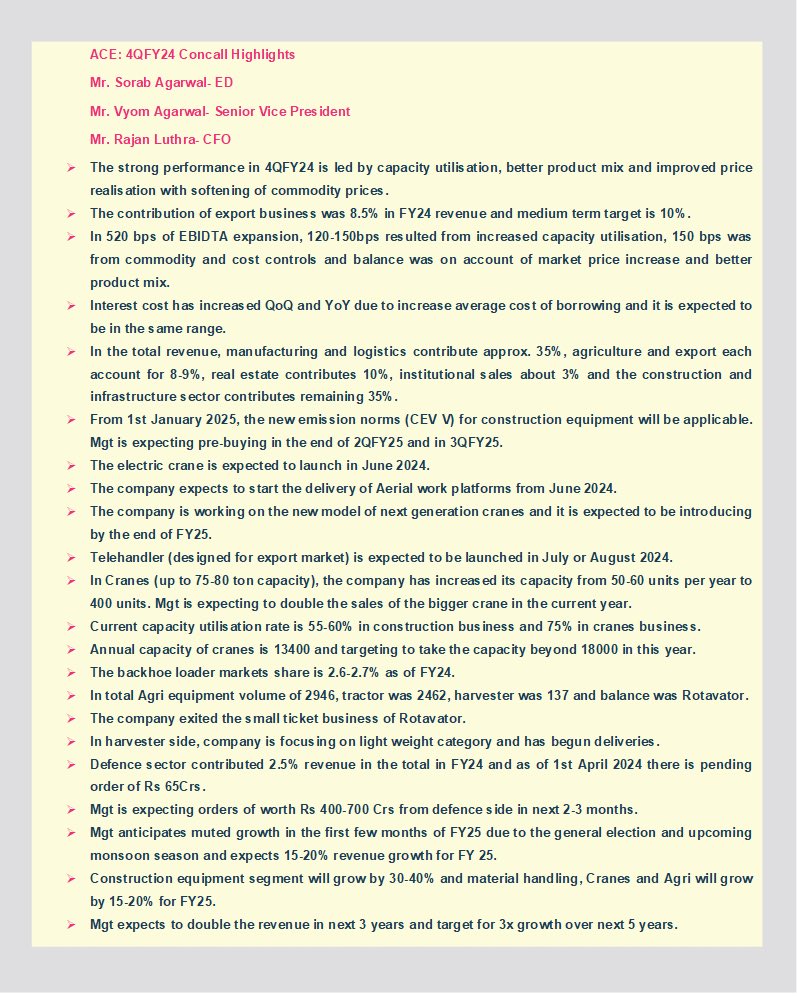

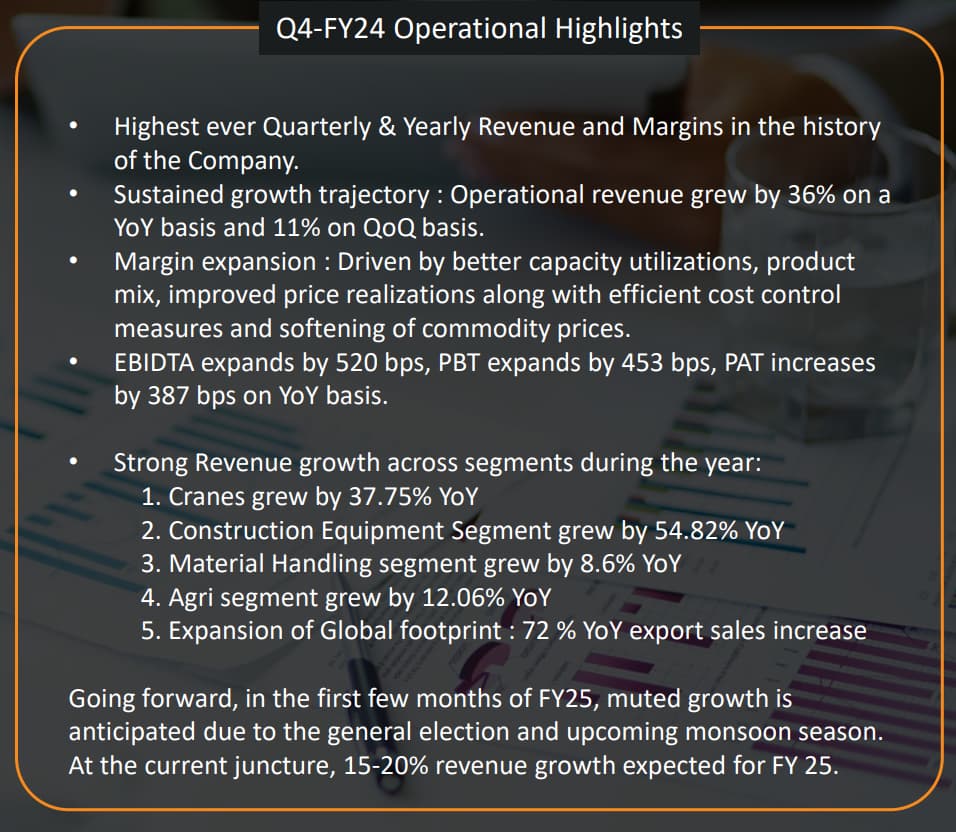

Summary of presentation - slide 9:

- Highest ever Quarterly & Yearly Revenue and Margins in the history of the Company.

- Sustained growth trajectory : Operational revenue grew by 36% on a YoY basis and 11% on QoQ basis.

- Margin expansion : Driven by better capacity utilizations, product mix, improved price realizations along with efficient cost control measures and softening of commodity prices.

- EBIDTA expands by 520 bps, PBT expands by 453 bps, PAT increases by 387 bps on YoY basis.

- Strong Revenue growth across segments during the year:

- Cranes grew by 37.75% YoY

- Construction Equipment Segment grew by 54.82% YoY

- Material Handling segment grew by 8.6% YoY

- Agri segment grew by 12.06% YoY

- Expansion of Global footprint : 72 % YoY export sales increase

Going forward, in the first few months of FY25, muted growth is anticipated due to the general election and upcoming monsoon season. At the current juncture, 15-20% revenue growth expected for FY 25

Link: FY24 presentation

5 Likes

Important points from the interview -

- 15-20% is a very conservative guideline. It should definitely more than this.

- Maintain revenue guidance of 4400r in fy26 and 5500 in fy27.

- Possible to do 3x revenue (of fy24) in next 5 years.

- Every 500-600cr revenue growth add to about 80-100 basis point to bottomline.

- Price increase taken from 1st of Jan benefit of that will kick-in from March onwards.

- Looking for an acquisition inside or outside the country.

- Cash 700cr and capex plan - 80-100cr

- Capacity at present for about 4500cr revenue and after this year capex they will go up 5500cr of revenue.

- Debt free.

8 Likes