Action Construction Ltd

Annual Report 2017

Promoter – Vijay Agarwal , Mona Agarwal, Sorab Agarwal

Company Overview

ACE is India’s leading Material Handling and Construction Equipment manufacturing company with a majority market share in Mobile Cranes and Tower Cranes segment. ACE also offers Mobile/fixed Tower Cranes , Crawler Cranes , Truck Mounted Cranes , Lorry Loaders , Backhoe Loaders/Loaders, Vibratory Loaders , Forklifts., Tractors and other Agri Machinery.

Industry Overview

It was difficult year for the global economy , characterized by low growth and geopolitical uncertainties.

In India rural demand continuous to be sluggish in the early part of the year , The overall market showed signs of recovery in the later half year of the year but faced a temporary slowdown in November due to demonetisation.

Indian construction equipment market is projected to reach 131 thousand units by 2022. The Indian construction equipment industry is projected to exhibit a cumulative annual growth rate of 19 % during 2013-18. There is a cautious optimism that by 2018-19, the industry will be back to an output level of 70,000 units that was achieved in 2011-12.

The union budget for FY18 has allocated infrastructure development Rs 3,96,135 Cr being 14 % increased compare to last year. The Earthmoving and Construction equipment (ECE) is back on track driven by roads and highway sector.

With projected forecast of good monsoons after a gap of two years , the demand for Tractors , Harvesters will increase the volumes of Tractors , Harvesters and Rotavators launched in recent past.

Operations

Company is focused on marketing , vibrant customer relationship , coupled with investing in R&D is the Mantra to ACE next level of growth. Company is investing in creating capacities and expanding manufacturing base , products and product support network this will enable to CATER the demand as it picked up. Company is working toward cost optimisation , lean processes and proficient operations to enhance profitability .

Company have R&D centre at Jajru Road , Faridabad and Dudhola link Road, Dudhola Village , Palwal.

Company Products :- Mobile Cranes - 3-50 tonss , Forklift Trucks , Mobile Tower Cranes , Tractors , Lorry Loaders , Vibratory Loaders , Backhoe Loaders , Motorgraders , Crawler Cranes , Tower Cranes ,Concrete Placing Booms

Company has changed Audtiors from M.S Rajan Chhabra & Co to Mr. BRAN & Associates

Total number of employees stood at 1014 compare to 1062 last year.

Under Amalgamation Action Construction Equipment Ltd allotted 1,83,83.000 equity shares and 3,02,19,380 cumulative Non-participating redeemable preference shares to the shareholders of ACE TC Rentals private limited. Further company had applied for listing and trading approvals from both BSE limited and NSE Ltd and approval has .

Risk

-

Depreciating rupee will drive pressure on margins

-

Volatility in prices of raw material will add pressure on margin

Segment wise performance

Company operate in three segments

-

Cranes

o Revenues increase by 19.46 % in the financial year

o Profit increase by 3 % in the financial year

-

Material Handling / Construction equipment

o Revenues increase by 62.13 % in the financial year

o Profit increase by 695 % due to increase in revenues and various cost initiative by company in the financial year

o Heavy investment in various infrastructural projects by public and private enterprise in areas like road construction , its maintenance , ports , power plants , telecommunication sector, urban infrastructural developments , smart cities , clean India and fast train projects, etc

o Major challenges faced is accurate shortage of skilled manpower both at worker and supervisory level as well as lack of experienced construction equipment engineers.

-

Agri-equipment

o Revenues down by 0.52 % in the financial year

o Profit increase by 173 % due to cost initiative taken by company in the financial year

-

Company proposes to transfer Rs. 200 lakh to the general reserve

-

Total amount of Rs 3,206.11 lakh had not been paid to income tax due to various disputes going on regarding Income Tax , Excise Duty , Service tax , SAD Refund and Sales tax.

-

Long term borrowing increased by 57 % from 2,396.89 lakh to 3,765.67 lakh

-

Short term loan decrease by 69.91 % from 8,242.37 lakh to 2,480.12 lakh

-

Finance cost has been reduced by 6.86 % from 1,401.67 lakh to 1,305.25 lakh

Company Subsidiaries

-

Frested Ltd , Cyprus – wholly Owned Subsidiary

o Company has granted a loan worth Rs 2745.72 lakh to Frested Ltd, Cyprus and waived off interest in following loan , repayment is schedule at 31-03-19

-

SC Form SA , Romania – Fellow Subsidiary

Top Ten Shareholding Pattern

Sr No Name % holding beginning of year % holding at end of the year

1 India Opportunities Growth Fund 2.43 1.36

2 Edelweiss Trusteeship Co Ltd 1.23 1.08

3 Dileep Madgavkar 0.76 0.89

4 Chander Bhatia 0.91 0.91

5 Union Small and Midcap Fund 0.37 0.51

6 Indianivesh Securities Ltd 0.01 0.48

7 Rahul Dhruv 0.27 0.48

8 Anuj Anand Didwana 0.13 0.37

9 Nitin Kapil Tandon 0.40 0.4

10 JV and Associates LLP 0.32 0.27

Financials

Segment Wise Revenue % Change FY17 FY16

Cranes 19.45 % 47,565.14 39,816.96

Material handling Equipment 62.12 % 10,151.76 6,261.62

Agri Equipment -0.52 % 15,230.97 15,310.62

Excise Duty 16.89 % 4,603.13 3,937.70

Segment wise assets % Change 2017 2016

Cranes 2.16 % 47,978.21 46,960.12

Material Handling Equipment 31.25 % 6155.18 4689.53

Agri Equipment 5.68 % 3924.87 4161.55

Unallocated 10.57 % 9,178.02 8,300.10

Segment wise Liabilities

Cranes 31.86 % 14,487.76 10,987.12

Material Handling Equipment 92.43 % 2,435.80 1,265.76

Agri Equipment 6.40 % 3,982 3,742.46

Unallocated -3.71 % 46,330.72 48,115.96

Segment wise Capacity Utilisation Installed Capacity % Change Production

2017 Production

2016

Cranes 7500 22.41 % 3572 2918

Material handling Equipment 1300 61.16 % 888 551

Agri Equipment 6000 -2.95 3594 3491

Turnover 2016-17 2016-17 2015-16

Qty Rs Qty Rs Qty Rs

Cranes 24.53 % 19.45 % 3599 47,565.14 2890 39,816.96

Material Handling 48.16 % 62.12 % 846 10,151.76 571 6,261.62

Agri Equipment 0.37 % 0.52 % 3460 15,230.97 3447 15,310.62

S.No Particulars Amount (Rs. In lakh)

1 Capital Expenditure 2.93

2 Revenue Expenditure (Incl Salary to R&D Staff and other related expenditures) 659.67

662.60

Sr No Name and Description of main products/services % of total turnover of the company on the basis of Gross Turnover

1 Cranes 65.20

2 Material Handling/ Construction Equipment 13.92

3 Agri Equipment 20.88

Indebtness at the beginning of year Changes in the year Indebtness at the end of the year

12,426.54 Cr -4084.01 Cr 8342.53 Cr

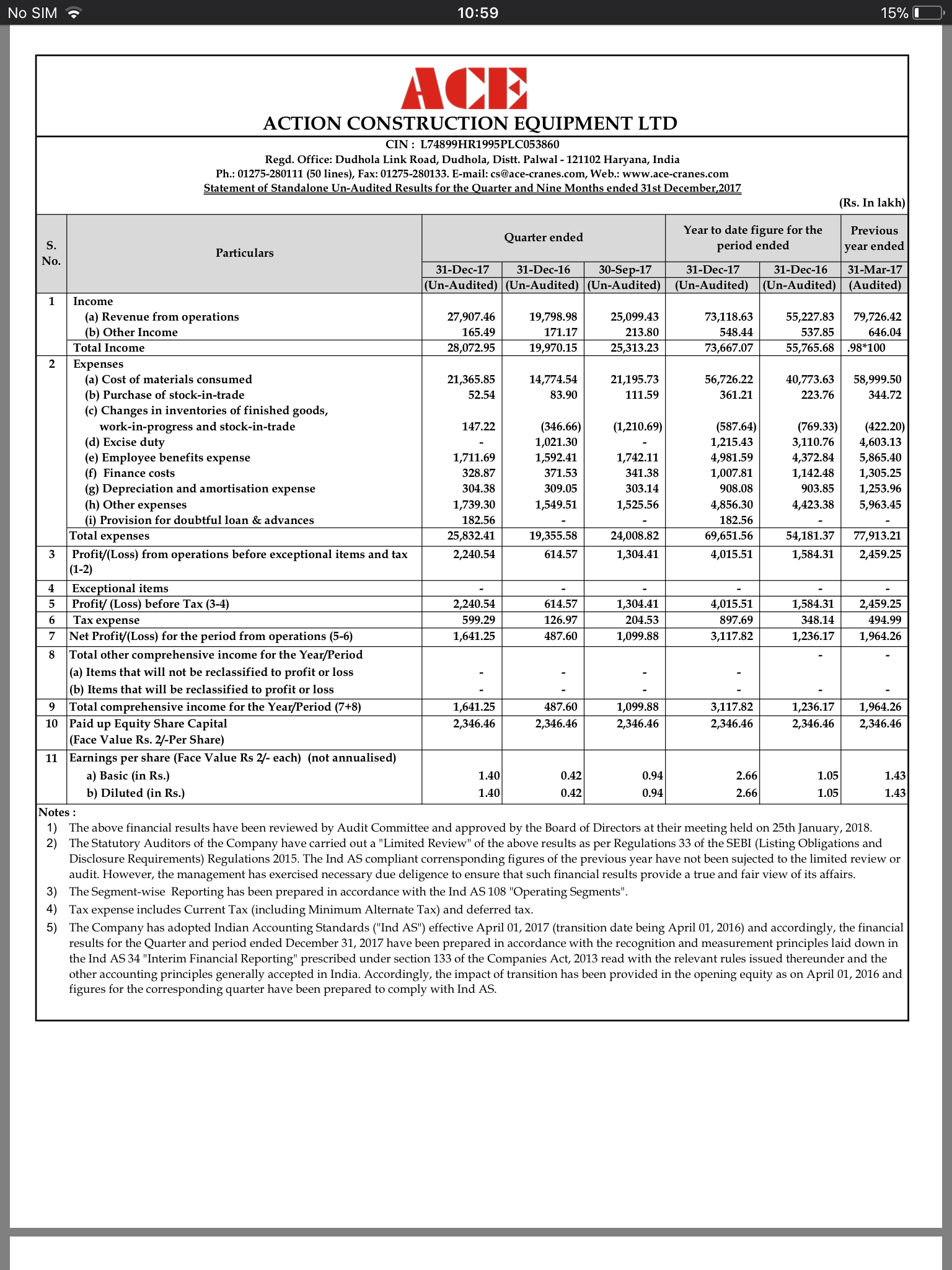

Particular Dec-15 Mar-17 Jun-17 Sep-17 Dec-17 Mar-18

Sales 187.78 229.86 188.96 250.99 279.07 367.46

Sales YOY% 19.60 21.45 22.76 39.86 48.62 59.86

EBITDA 11.24 8.96 9.39 17.35 27.08 38.31

EBITDA % 108.92 -31.39 1.73 66.03 140.93 327.57

PAT 4.88 2.10 3.77 11.00 16.41 21.46

PAT % 188.76 -51.72 24.83 146.64 236.27 921.90

Particular 2013 2014 2015 2016 2017

Sales 667.85 614.93 597.65 637.30 751.23

Sales YOY % -21.94 -7.92 -2.81 6.63 17.88

EBITDA 29.72 39.49 20.97 30.95 43.72

EBITDA YOY% -43.38 32.87 -46.90 47.59 41.26

PAT 7.21 4.02 6.75 8.81 19.64

Cash Flow 2013 2014 2015 2016 2017

Cash from Operating 42.33 36.86 39.19 57.43 71.74

Cash from Investing -44.98 -19.92 -14.00 -24.73 -11.12

Cash from Financing -1.62 -19.33 -26.06 -33.00 -54.03

Balance Sheet 2013 2014 2015 2016 2017

Borrowings 156.21 149.61 137.72 124.26 83.43

Liabilities 219.43 222.01 235.27 238.58 298.70