Hi Mohit , what is the easiest way to understand the chart basics…any course/books you recommend for same.

1 Like

Hi @Mohit_baid can you show how you arrived at 35FPE?

Earnings will at least grow by 70-80% (YoY) from here so do the math…how did I arrive at 70-80% earnings growth? you can look at the past few quarters and see if the factors that contributed to the past growth continue to exist, will they grow stronger, or will they fade away also the promoters have guided for an even better growth rate going ahead.

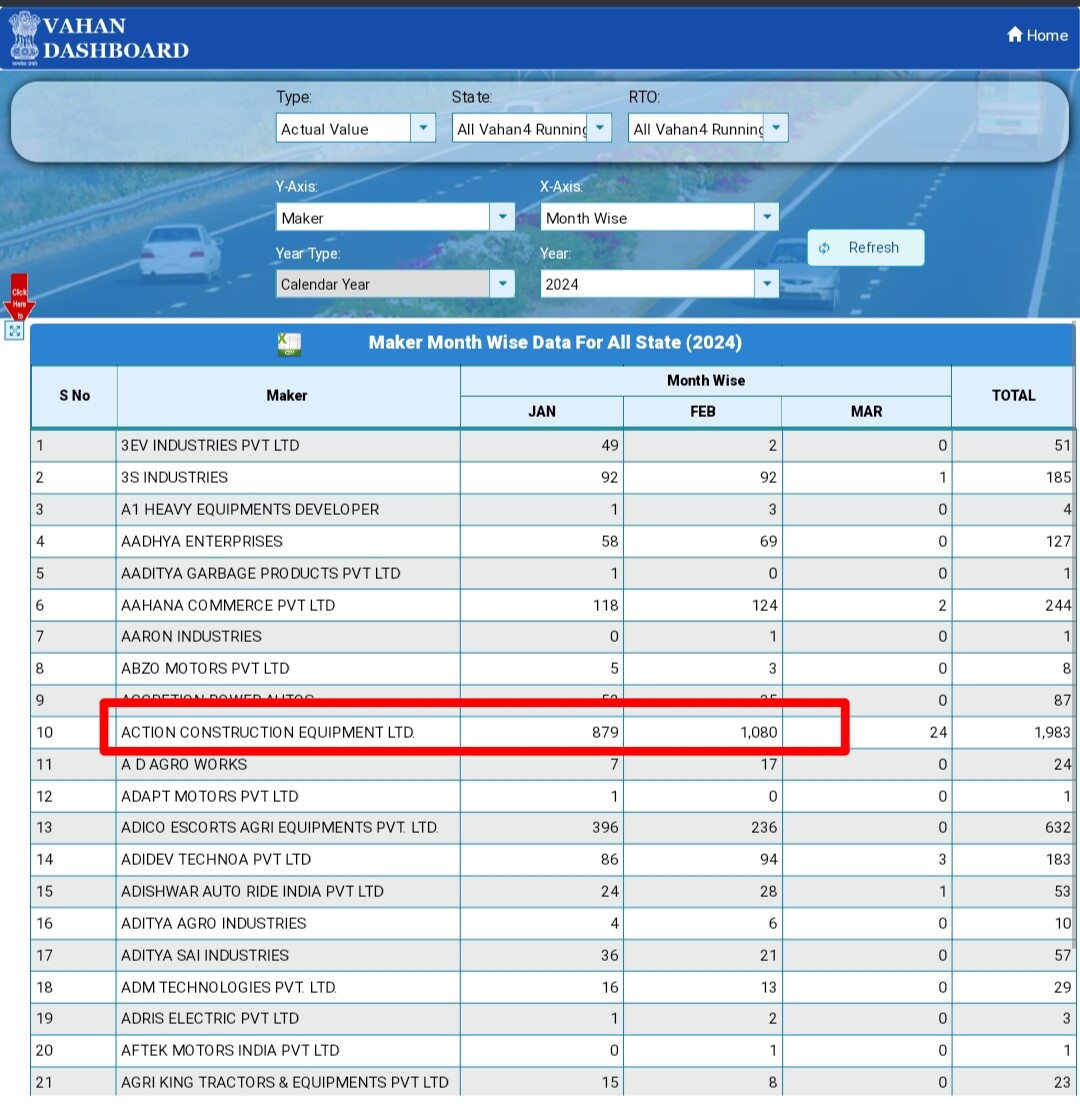

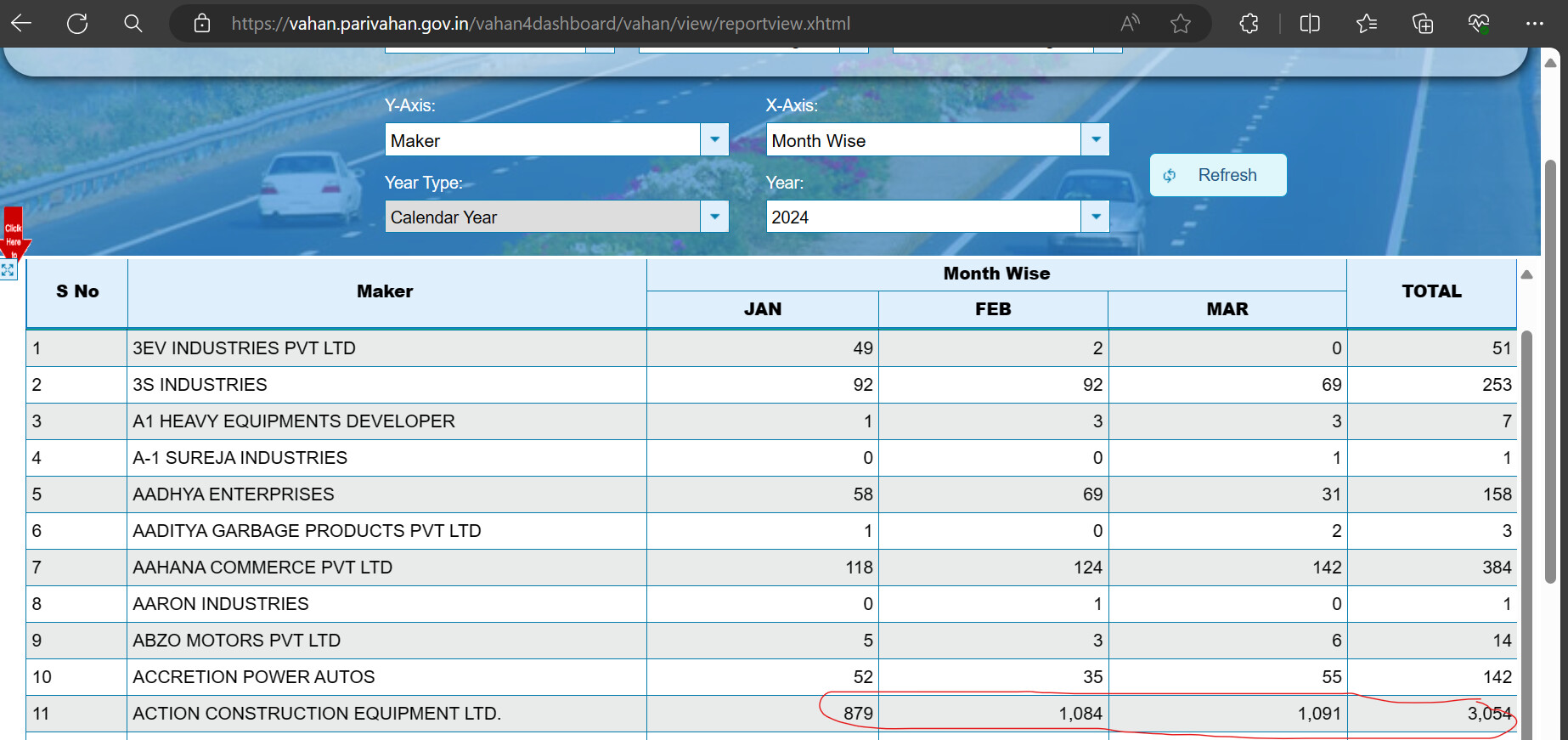

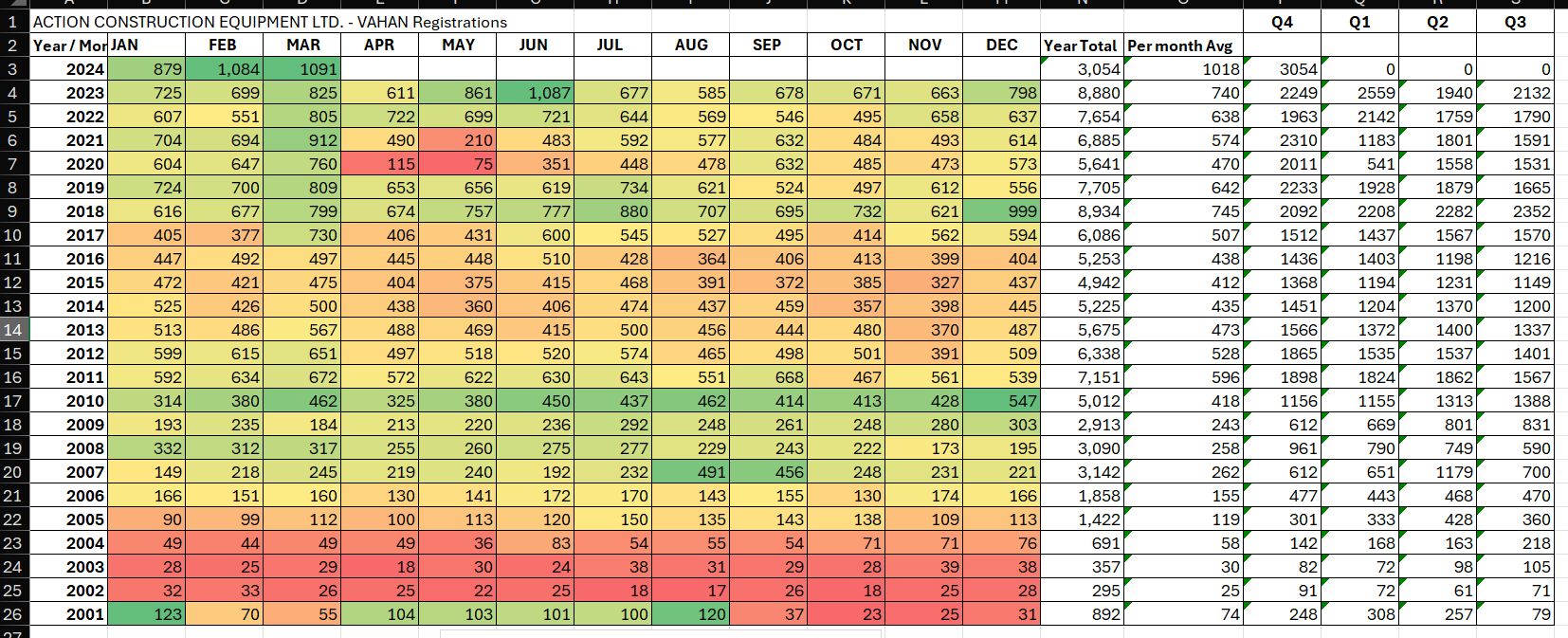

Thanks for the Vahan data reference.

I got all the ACE data from VAHAN dashboard from last 20+ years to see the registrations trend, and it is rocking now. Excuse the Years data in reverse, so read accordingly.

14 Likes

@Mohit_baid @ashwind how much risk do you guys see from rising commodity prices. We are still in a inflationary environment and inflation can comeback in commodities like steel. Has management made any comment on how much margins can fall in case of steel price increase?

Market risks like higher commodity prices will always occur, but with Japan & EU in recession, China trying to kickstart growth, what is putting pressure for higher commodity prices?

Mgmt believes Commodity prices get passed over a gap of a quarter, so impact will be limited and margins should revert in a quarter. Below from their recent Conf call in Feb’24.

3 Likes

I like the clarity in thoughts of Mr. Sorab and how he is articulate to understand the market dynamics. He has so far proven to be real successor for Mr Vijay Agarwal. He seems to have a vision for the future. He has been conservative in giving guidance previously (in concalls). I have super conviction in ACE and the management so far. India needs at least 10 years of continuous investment in the infra sector to even think of trying to compete with China.

Discloser: Invested from very low levels since Covid crash in the company. It has the highest allocation of my folio. 35%.

5 Likes

Can you provide for the same??

Corporate Presentation - Impressive

https://www.bseindia.com/xml-data/corpfiling/AttachLive/c0ca75e4-ea36-4880-8335-8b09e3f9d5b0.pdf

3 Likes

Notably Manish Mathur, the CEO of Cranes at ACE, mentions “For example, let’s take tower cranes—an essential product in our range. Currently, our market size stands at 1000 units. In comparison, China has close to 100 companies involved in tower crane manufacturing, with the top companies producing an impressive 11,000 machines at their peak. Despite this, our total market share remains below 1000 units.”. Is is possible to get data on what is the Chinese market size and how it compares to India to validate his statement? Also guaging how China has shaped up in last 20 odd years, will help understand how Indian market for cranes will probably shape up.

12 Likes

2 latest interviews:

One for guidance on capacity expansion and other for next 2 to 3 years outlook

5 Likes

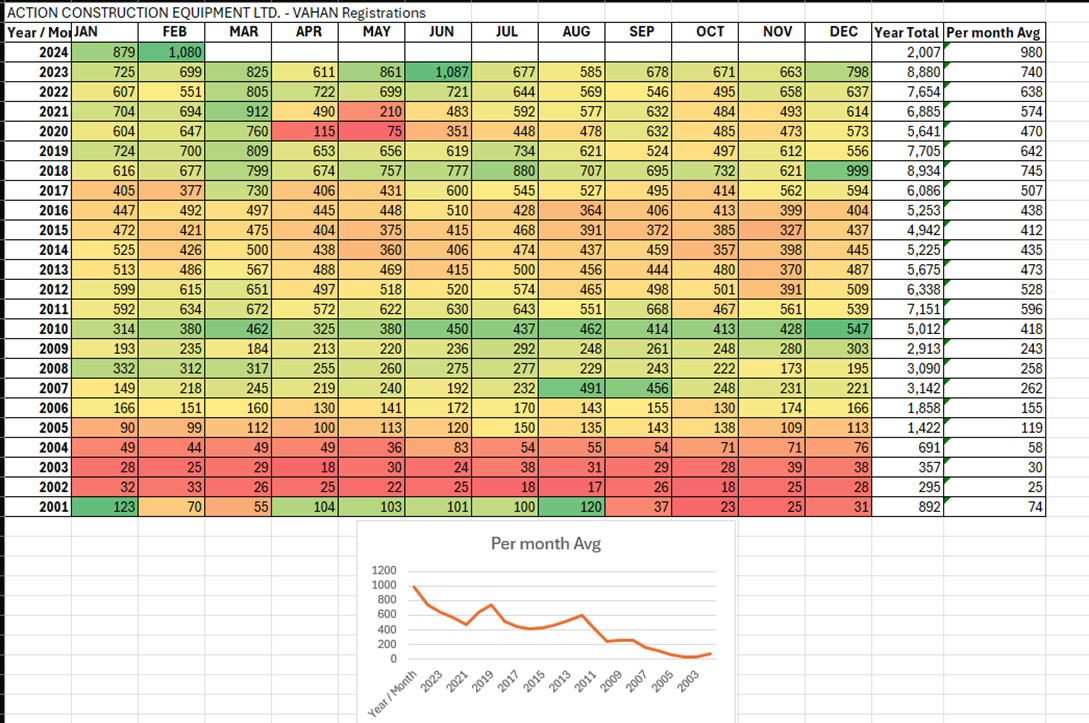

As of Mar 31, Action has sold 3054 (highest quarterly ever) VAHAN registered vehicles in Q4 (Jan-Mar) FY24 qtr. This was 2132 QoQ, and 2249 YoY, nearly 40% jump. If there are no other -ve surprises, we might have a good possibility of hitting Rs.10 EPS for Q4, and Rs.30 for entire FY24. Super Bumper results can be expected.

Note: After Covid years, the Q1 of a FY has been bigger than Q4 of previous FY for last 2 years, so if we see that happen this year, that will be icing on cake. Not sure if Elections are going to have any -ve impact, will see in the VAHAN number by end of April/May.

Monthly VAHAN numbers:

24 Likes

How likely is the growth to sustain? Concern right now is valuations. At the end of the day underlying industry (infra) is cyclical and idk if we are at the starting of cycle or its getting moderated? FY25 budget has pegged the infra allocation growth at 10% YoY from the earlier 2-3 years when the overall allocation grew at 25-30% CAGR.

Just wondering if there’s space for the stock to compound at say 40-50% CAGR from current levels?

1 Like

Valuations are very high right now. Might not sustain these levels going forward and PE will contract and valuation will become reasonable. But it has run in steep mode and high chance of crash in valuations the only question is When. My 2 cents.

Short Answer is a Big No.

They will continue to do well. But CMP is at a premium PE now. I expect a time correction now at this range. Further increase will take some time.

Disclosure: Invested in Family Accounts.

1 Like

The base is already high when it went to Capex spending on infra went 11Lakh crore last year, so it only makes sense to have a more moderated growth in spending, increasing it at a rate of 25-30% CAGR isn’t sustainable, but you have to note that its already a high Capex spend, they are the market leader in crane segment, and ACE’s capacity can be increased much further when you compare them to other global leaders that manufactures crane. But the stock compounding at 40-50% CAGR from current levels, is an insane ask tbh ![]() The budgeted spending is intact and there are no issues with it as per me.

The budgeted spending is intact and there are no issues with it as per me.

They will need more capacity, to deliver growth, they are currently incurring CAPEX, and also have set target to double revenues by FY26 or FY27 if I remember it correctly.

(Btw, what stock will do, no one knows)

disclosure : invested.

3 Likes