I did not find a chatter focusing on the newly listed entity Aarti pharma labs. I see it an interesting space and an interesting company. Here is my basic research.

Manufacturing facility in Maharashtra, has Genral API, corticosteroid and oncology API production blocks with US FDA and EU GMP accreditation.

Have a strong backward integration strategy and in the API segment where they produce the essential raw materials for their products.

Generic API products lists:

Cardiovascular

Anti asthmatic

Anti-cancer

Anti-coagulant

Anti-diabetic

Arthritis

Cns agent

Skin care

Calcimimetic

Decongestant

Anti thalassaemic

Analgesic

Ophthalmologic

Manufacturing.

Six manufacturing plants and 2 R&D centres.

Customers

Supplies to Beverages, Nutraceuticals manufacturing companies, and Pharmaceuticals Industries across the world.

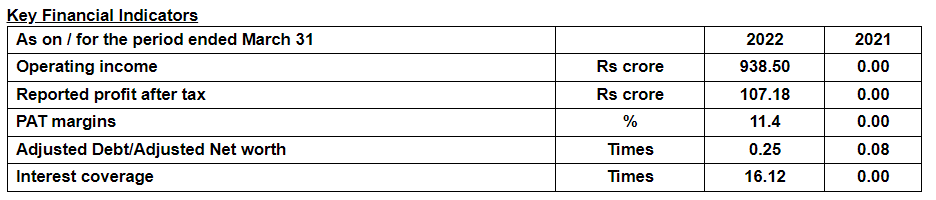

Many thanks for starting this thread. Attaching the link for CRISIL rating report dated Feb. 2023. It provides a glimpse to the financial profile of the co. post the demerger.

What’s the difference between aarti pharmalabs and pinnacle life science which is a subsidiary of aarti drugs…? For eg. aarti pharmalabs has a oncology product Bicalutamide which is also available with pinnacle…some of the board members are also same across these companies…

Have been going through the Company, Looks Interesting and Cheaply Valued on the Face of it.

They should do Revenues of 2000 Crores as of FY23 with a PAT of close to 200 Crores. Market Cap at 2500 Crores gives it a PE of 12-13x FY23 Earnings.

The Company has historically Grown at 20%+ and has been able to maintain Margins on the higher Teens end for the last 3-5 years except Fy23 where the Margins should remain close to 15% mark (The Operating EBIT Margins)

Given the Industry is a Neglected One, with the Group as well not doing well, This might be one of the Opportunities to look for.

An Additional Capex of 300-500 Crores is expected to come on stream between FY23/24. Some Scale up from here should help as well.

Wanted to know if someone else is working on the same and Has some Anti Thesis or Thesis here.

This is my first post on the forum so apologies if I get anything wrong!

Disclosure : Invested in the stock ~ hence, biased

I did some calculations a couple of weeks back, when the stock price was around ~ 300 level

Bearish : Assuming a time horizon of 4 years, and a conservative growth in PAT of only 8% p.a, and assuming PE ratio at 10 only at time of exit, then market price shall be 300, thereby protecting capital - entry below 300 will provide a good margin of safety

Bullish : In a scenario of growth of 10% PAT p.a., and 20 PE, then market price shall be 649 thereby providing CAGR of 21% p.a.

I also did a write on the company from ground up to cover all the basics for someone who might be new in the space - for my own internal thesis/journal - & it’s a mashup of information gathered over the internet including annual reports and latest credit ratings.

Also I was hearing that there is significant shortage of many cancer / oncology drugs in the US - don’t know much this would have a impact on Aarti pharma but may indicate that the down cycle if any may be short lived

Given that their reported profit after tax in FY 22 was only 107 Cr basis CRISIL report what is teh confidence that it has doubled to 200 Cr in FY23 ? Is there so much of margin xpansion with incraesed sales growth ? Is there a one off ?

Finding it difficult to reconcile such a large increase in net profit

Found this in the con call scripts from which I guess you got the numbers ?

Nitin Agarwal: Sir, last one, on Pharma business, how are you planning to share more details on

the business? Anything which is planned sir, if you can share it on this call?

Rajendra Gogri: Basically, 9-month results are already in public domain in Pharma. So, EPS for 9

months was about Rs. 16.6, annualized EPS about Rs. 22 for Pharma. On an

absolute number, PAT is about Rs. 151 crore and EBITDA is Rs. 264 crore for 9

months in Pharma and then after Q4, obviously, there will be a regular interaction

for Pharma.

They have reported the numbers. Even I have been having a Hard time reconciling the numbers given the increase. The Ratings Report has a very different number though. Don’t really know how is there such a large difference.

This Quarters Results and Concall should clarify a lot of doubts and should help us understand the vision and way forward.

Was reading more on Synthetic Caffeine Industry, here are my findings:

Global Market Size: 120,000 tonnes (USD2.4bn appx)

Global Growth: 5.4% CAGR

US is the largest market (40%), followed by EU.

South Asia is the fastest growing market at 14% CAGR growth

End Usage: 55% Foods, 10-15% Pharma

Major Manufacturers

CSPC Pharma Group

Aarti Pharmalabs

BASG SG

Spectrum Labs

Kudus Chimie

Shi Yao Pharma

Minerals Ltd

Indian Players

Shri Ahimsa Mines

Micro Labs India

Chinese have 40% share of global production of Synthetic Caffeine

During my scuttlebutt one of the dealers mentioned about some chinese firms dumping at much lower costs in Q4, any edge on current pricing will be extremely helpful!

Usually during IPOs and spin offs there will be such huge jump in numbers. Only then they can sell the story that the IPO/ Spin off will create value. Base on that we cant expect what FY24 numbers will look like. However Assuming a 180Cr-200Cr PAT for FY23 it is trading anywhere between 13-15x FY23