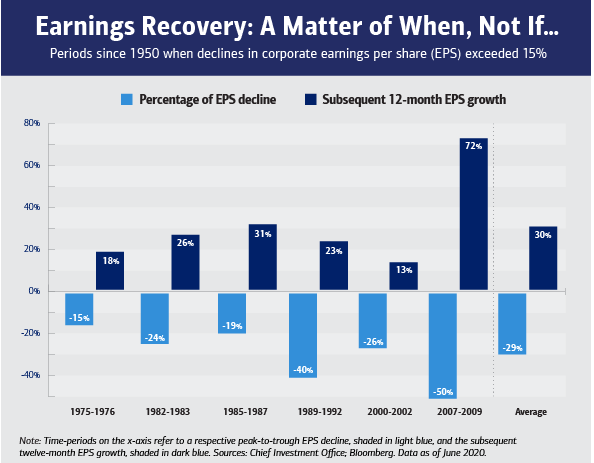

This is data for the US markets, but something worth considering. The magnitude of fall is proportional to the magnitude of the rebound.

This is data for the US markets, but something worth considering. The magnitude of fall is proportional to the magnitude of the rebound.

Here is something I recently shared with our investors. The idea is to think through what you are doing and why you are doing it. If that part is clear, then most other considerations, like tax etc will become irrelevant.

@yourraj What you are asking would each cover a separate blog post or chapter in a book

Maybe someday when I have the time, I will try and collate my thoughts on each of the topics and post.

One simple point - India does not have a demand problem. Ever. In anything. Our overflowing population means that we are always in need of more and more stuff - be it houses or food or cars or underwear!! So, people creating an investment thesis on aggregate demand on anything is missing the point.

I have made this mistake in the past. India is a hugely power deficient country. So, power discoms and power producers ought to do well always. Practically, never really happens. Same story in nearly all real asset or infra related businesses.

So, assuming that demand will always be there, let’s look at some of the critical supply factors for real estate:

Currently, credit is practically drained out of the system from small and mid-sized builders. The biggest source of credit to them where players like Indiabulls, DHFL and other such NBFCs who have now severely cut back and practically stopped lending. So, the next step is a massive consolidation in the industry, which seems to be already underway.

There is huge inventory pileup across all major cities which the builders are sitting on and unable to sell. Those would need to get sold first, probably even at a discount to prevailing market rates.

Supply of real estate in suburbs will likely go up as demand from semi-permanent WFH category starts looking for larger homes at a lower cost point.

In summary, the situation is going to be interesting and I personally feel that the real estate sector, though, may see some near term pain can actually be a very good performer over the next 10 years.

Note to self - The real estate theme can be played through the real estate players or through the ancillaries like Kajaria, Cera, HSIL, Somany, Asian Paints, Berger, Pidilite, Century and Greenply etc.

There are two predominant fears for investors – the fear of missing out, better known as FOMO and the fear of being invested, whom I call FOBI. For those who love to time the market or continuously have different opinions about the market and its future direction, these are the two most important considerations.

FOMO is when you are not invested in a stock or a sector and it starts running up a lot. FOBI is when you are invested but are fearful that the market will crash and take away your gains or your capital.

Both are equally dangerous for investment health. Both make you do irrational things, which in hindsight you regret. And everyone has them at some point in time or the other, even the most seasoned investors.

The way I try to deal with the FO cousins – FOMO and FOBI is through a couple of ways. Firstly, for tackling FOMO, I invest in a momentum portfolio using my quant strategy, quantamental Q30. Here, the system picks up the stocks which are doing well, for whatever reason. I have designed the system so that it catches short to medium term trending stocks and ride the trends in them. So, I am invested in those “runaway” stocks like Adani Green, Alkyl Amines or Laurus Labs and don’t have the feeling of having missed out on any significant rally.

Secondly, I have a written down investment plan for myself which is, to me, a sensible way of long term investing. It includes dividing the portfolio into long term stocks, turnarounds, dividend plays, growth stories or some combination of these.

In my long term portfolio, I very rarely try to time the market in an absolute sense. I may calibrate positions from time to time, but very rarely do I get in or out in one go based on valuations or market levels. I am comfortable knowing that investing in equities is the best way to participate in the wealth creation journey of a business. There is likely to be a lot of ups and downs but since my investment duration is the next 30+ years, I am not very concerned as long as I know that the businesses will perform well over a business cycle.

The best way to tackle FOMO & FOBI is to have a long term plan for investing. Having a well laid out strategy for your own investing is critical. As I keep saying, more than three-fourths of investing is behavioural psychology and you should be aware of the fact and program yourself to circumvent the various inevitable biases.

(This article was first featured in Economic Times - https://economictimes.indiatimes.com/markets/stocks/news/fomo-is-gone-its-cousin-fobi-haunts-investors-now-how-to-deal-with-them/articleshow/77926851.cms)

Sir, Also is see valuations of most HFCs at Rock bottom apart from the likes of canfin homes, HDFC etc. Do you think the real estate cycle can be played via HFCs too? Some names like repco and LIC HFL have given close to nil returns in the last 10 years despite consistent growth and are available at all time low P/Bs. Do you think playing real estate cycle via HFCs will bring better rewards or it is better to stick with consumers side of real estate sector in stocks like pidilite, cera etc as you mentioned?

| Description | Rs in crs |

|---|---|

| Large cap | 1,93,24,362 |

| Mid cap | 26,11,351 |

| small cap | 16,87,726 |

| Multicap fund size | 145000 |

| Large cap | 101500 |

| Can be in large cap | 72500 |

| Have to move out of large cap | 29000 |

| Capital to move as a % of mid cap | 0.56% |

| Capital to move as a % of small cap | 0.86% |

Even if I assume a low free float of stocks at an aggregate level, the numbers are too inconsequential to bother about.

We may see some rally based on herd behaviour of investors, but I would be surprised if we see any major sustained rally in mid or small caps due to this.

Also, mutual funds will surely look at other options like merging with other schemes, renaming/reclassifying etc before investing a lot of money in illiquid smallcaps.

Hi Abhishek,

My view is that the flow will be focused on select few companies in the mid and large cap space.

The choice of companies around with their free floats may lead to re rating of those companies

Technofunda investing is when you use both fundamental analysis and technical analysis in your research process. For many years, I used to be a purely fundamental investor. My primary focus was on understanding the business as well as possible, its triggers, the management and what impacted their performance, the competition. Over the years, I could figure out that I was missing out on something, but I could not figure out what.

I would buy stocks which would be growing so inevitably my errors of commission were very few and far between. Around ten years back I started the active process of reviewing my portfolio and thought process in an active manner every year (and then every 6 months). I could see that all the stocks I were buying were making money. I started feeling very good about my stock picking abilities. This continued for a few years.

But this changed after two consecutive years of the ValuePickr Goa meets where I and Hitesh Bhai (@hitesh2710) , both being relatively early risers, would get up in the morning and go for a walk on the beach. In those hour-long sessions, I could see a completely different approach that Hitesh Bhai followed. Of taking more frequent and sometimes very large bets, which was something very different from my style. And boy, was it working well for him. Explaining with a cricket analogy, my style was more like that of Dravid, slow and steady, whereas his was more swashbuckling, like Sehwag. And we still remember Sehwag for being the only Indian to have two triple centuries in Test cricket and a double century in the one-day format.

So, I started learning technical analysis (which later led me to the quant side because of my programming background, but that’s a story for another day). What I immediately could see was that the mindset required to do fundamental and technical analysis was different. So, I did the first thing I thought was logical. I decided that I was the most comfortable as a relatively long term participant. I did not want to be stuck in front of a trading terminal throughout the day, so longer timeframe charts was what I started looking at. I could sense that if I could merge the two analytical disciplines together it would be greatly beneficial. I did not like the constant bickering and egoism of the two camps. The fundamentalists thought the technicians were snake-oil salesman and the technicians thought the fundamentalists were prized smug idiots!! I could see that in the annals of investors and traders with great long term track records, I found people across the spectrum of styles. This led me to believe that there is no style which is good or bad, it’s how we use it.

Once I knew both fundamental and technical analysis well enough, I found I could make much better sense of the markets. I could see why something was happening. So, another level of information flow started opening up in front of me. What other market participants were doing. When coupled with your own analysis, it can be a potent force.

Hitesh Bhai and I have been collaborating on our own investing for a while before we started Hitpicks. Hitesh Bhai uses a lot of technical analysis and some proprietary indicators and patterns for identifying stocks that can potentially move up before they make a move. This fascinated me. He called it the Prognostic pattern (after all he is a practicing doctor!!). It is a not a foolproof method but when it works it does really well. Added to good quality stocks and favourable fundamentals, it is a good option for those who want to play a medium-term game (between 3-12 months). That’s what we try in Hitpicks, the advisory service we run.

The biggest advantage that I have seen in using a Technofunda approach is to be able to concentrate significantly when both the fundamentals and technicals are aligned. That provides a much higher CAGR to the portfolio than otherwise possible. But it also has its downsides as well. This approach does have higher churn than a simple buy-and-hold strategy. Some like I keep saying, only those with a particular mindset can use a strategy like this.

Should we give more weightage to technicals or fundamentals while picking a stock?

It depends on the time frame. If you are a long term investor, then fundamentals would take the most weightage. The shorter the time frame, the more important technicals become.

The Scam – The Harshad Mehta Story is a recently launched web series on SonyLiv. It is very well made, fast-paced, and sticks to the storytelling instead of digressing here and there. It is the best market-related movie (I include all video content in this “movie” class) on Indian markets by a long way.

I have read the book on which this is based on. The book had all the original names of the people involved. For some reason, a few people got renamed in the show. So, characters portraying Ajay Kayan, Rakesh Jhunjhunwala, Radhakishan Damani were not called out explicitly.

Although, the book is a great read and the web series is an even better watch, here are some to the lessons that I took away from the whole period and sequence of events.

Unbridled Ambition - I think this was the main reason why Harshad got into trouble. He did not know where and when to draw a line. He came from a modest background and wanted to grow too big too fast. He did not consider the consequences of his actions, because he always wanted more.

Leverage Kills – Ultimately, it is when you are over-leveraged is when you get into real trouble. Liquidity is king. Harshad’s efforts were concentrated on leverage to pump in liquidity. The problem is no one is bigger than the market. In his hubris, I think he forgot that.

The End Do Not Justify The Means – Harshad used to say that what he was doing was being done by everyone else. All the big players were following the same corrupt practices. Actually, it makes no difference if everyone is doing the wrong thing. It is still wrong. The problem with being on the wrong side of the law is that it’s a slippery slope. You start with a small digression, and very quickly it snowballs into something out of control. This is exactly what happened with Harshad which led him to eventually claim that he bribed the then Prime Minister.

Market Personified – When he was leading the markets he became a media darling, the first real Big Bull. His ostentatious lifestyle, his Lexus, his larger than life image in the media were also major contributors to his downfall. Firstly, it attracted detractors who felt sidelined or spited or were simply envious of his meteoric rise. Secondly, it gave a face to the good and equally importantly, the bad of the markets. So, when the markets crashed, it was Harshad who had to take probably a larger share of the blame. Personification is a concept popularized by Daniel Kahneman and it played out perfectly in this instance.

Alternate Histories – Radhakishan Damani, RKD as he is more popularly known is believed to have told a few of his friends: “Agar Harshad saat din aur apni position hold kar leta, toh mujhe kathora leke road par utarna padta.” (Had Harshad held his position for seven more days, I’d have taken a begging bowl and walked on the road). At that time, no one knew how the dice will get rolled and that RKD would become a great businessman and investor. The same is true of Rakesh Jhunjhunwala. Always be aware that winners and losers are known only in hindsight and the most intelligent course of action is to be conservative and prudent while investing.

Karma Catches Up – Ultimately, Harshad was running a sort of Ponzi scheme, where increasing amounts of cash was required to keep the markets propped up. His wrongdoings brought down so many people who trusted him blindly and bought shares based on his advice.

A great study in contrast is Warren Buffett and Charlie Munger. More than their investing acumen, I am a great admirer of the way they have conducted their life and business.

Hi @basumallick . I really liked your posts on full time investing and on narratives.

In my opinion, 2009 to 2015 was a very good time for a fundamental based investor. Because you had earnings growth, consistency and good valuation ( After 2015, only 1 or 2 names had consistent earnings growth until covid. Of course, there was stock price growth in many quality names).

I think investing ( for lesser mortals) is very difficult when earnings are not consistent. I liked your post where you talk about debt portfolio taking care of expenses. That makes sense. However, even though one can live off debt portfolio, one many not be able handle the notional loss in equity. During every crisis, there will be a lot of negativity. And we are worried about the near term or long term earnings, no matter how good the company is. Only in hindsight, things will look good.

What I noticed is that, narrative based investing has given phenomenal returns. ( For example pharma api, agri, telecom, US tech etc recently). Of course, its not easy to catch the signal early. I am also saying it with the benefit of hindsight.

In that context, I was just thinking about the asset allocation. Lets say one’s networth (Investable liquid networth) is 10 crore. Don’t you think, it would be a better strategy to invest 8 crore in debt and use 2 crore for the narrative based investing?. (By that I dont mean pure speculative investment. There has to be some short term earrings growth. 10 crore is just a random number. Replace with any number). Somehow I feel, this would be better than high equity allocation and buy and hold type of investing. I know there is no right/wrong answer for this. But I would appreciate if you could share your views. That will really help.

Running an advisory for the last year and a half, I have had the opportunity to interact with a lot of investors. One question that keeps cropping up from time to time and has increased in the last few days is, “The markets are at an all-time-high, should I invest now or wait for it to fall?”

Here is what I usually tell them:

Mismatch of timeframes

One of the biggest mistakes we make is looking at the market through a short term lens when we are trying to invest for the long term. We say we want to invest for the long term, implying atleast five to ten years but keep looking at the markets on a day to day basis.

Two main drivers – FOBI & FOMO

Investors are driven by two primary thoughts – i) the fear of loss (FOBI – fear of being invested) and ii) fear of missing out (essentially greed).

When markets are falling people are scared about losing money in their investments. They try to look the other way or panic into selling at the most inopportune time.

When the markets are rising people become greedy and scared at the same time. Greedy because they want to participate in the gains. Scared because of their past experience of losing money in the markets, they are afraid it would be the same again.

Future is uncertain and unknowable

No one knows what tomorrow brings. All the great gurus use different techniques to interpret the conditions of the present and try to extrapolate to the future. They can use varying tools to do this – fundamental analysis and technical analysis are the two most prominent ones. People do use other tools as well, like macro analysis, astrology, numerology etc. The main point is no one knows.

Just as an example, when Bajaj Finance was at 2000 in late May 2020, investors were waiting for it to go to 1000. Or that they will buy it when it went to 1200-1400. Neither prices came. Today it is 4000+.

Invest regularly

If that is the fundamental truth, then the best course of action is to be conservative, prudent and systematic. That is why I like the concept of SIP (systematic investment plan). You invest NOW. You don’t wait for a better day. Because you never know if tomorrow will be a better day or worse.

Can’t agree more with the quote below -

While I also am somewhat tentative towards infusing fresh investment at this time but I always keep in mind that my time horizon is far lengthier.

However, I found that being vigilant towards your portfolio composition and having a systematic framework of booking profits is also beneficial. But being much junior to you would love to hear your thoughts.

Regards

SIP in the early years. Once the portfolio reaches a good size relative to one’s income (or even relative to savings per annum), then asset rebalancing/asset allocation strategy becomes more important. Anyway, by the time their portfolio reaches a good size, many folks would have figured this out.

Portoflio composition should always be kept in mind. Systematic selling does not make any sense unless there is a reason to sell.

The one thing I missed is even when you are starting off, if you are a serious investor and intend to invest in equities directly at some point in time in the future, it is better to do it yourself and invest in equities directly. The learning keeps compounding. And it is something you miss if you go the indirect mutual fund route.

Hello Sir,

I wanted to ask you a question regarding SIPs in the market.

Lets say I want to invest 1 lakh in a company whose stock is quoting at Rs.1000 today.

So if I want to wrap up my investment at one go I would buy 100 shares of the same.

While this method is good when a stocks valuation is extremely favourable (Eg. April-May 2020), it has backfired if the stock is very volatile/is rising.

Currently I make 40-50% of my investment and leave the rest to luck to see if I can get lower prices or I would buy the rest if a quarters result has been encouraging.

What structure would you suggest I go about making an investment especially in a company where the stock is rising and is offering no opportunity to enter.

Thank you.

Seeing your and some of the other’s example, i also thought it make sense to invest in equities directly - initially one might incur losses but experience gained and even if moderate success achieved helps in life as an additional skills set, in case things go bad in other spheres of life. If one achieves moderate success that provides a mental comfort that, something that is of one’s own making.

and by luck and god’s grace if one gathers wealth via equity route, equity investing requires decent effort and keeps one engaged which if achieved via MF will never do.

Your views?