Hi guys

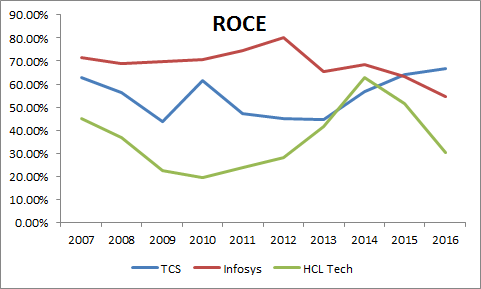

I was just going through the ROCE’s of these three marquee indian software companies. I am not an IT guy so i dont know much about the specific competitive advantages of these 3 businesses. All i know is that they make software and provide services. The relative differences in the ROCE’s however tell a story that even someone as uninformed as i am could use to make some intelligent investments. Here is the chart. Clearly from ROCE trend TCS wins hands down. Since 2007 its return on capital has increased from 62% to 67% & has been increasing since 2012 whereas infy ROCE has decreased from 71% to 55% over the same period. HCL Tech is even poorer - from 45% to 30%.

The PAT margins are also telling. Since 2007 , HCL tech margins have ranged between 10% to 20% , Infy margins between 20% to 27% and TCS margins within an even tighter range of 20% to 23%.

And the PE’s of all these 3 reflect that - TCS - 17.06, infy - 15.3 and hcl tech 14.78 ( data from screener )

TCS comes out as a strong winner in my opinion its got incredibly stable margins, a ROCE which is increasing.

These are the numbers. There are many IT guys on this forum and i am just highly curious to know what is that TCS does that makes it relatively more valuable. Purely from an education point of view if anyone can throw light on this it would be awesome!

ROCE calculated as PAT/(Equity + Debt - Cash - Short term investments) & data is from ratestar.in