I am really trying to understand this. I understood that three factors, ROE, ROCE, and PB are relevant. And I would want a high ROE/ROCE and a low PB.

That way PB of TCS being high is a negative.

But should I divide the ROE by PB to arrive at the correct assessment?

This is a new idea, and thanks for it. But I want more on this.

You are spot on. I used to have similar thoughts and realized that it’s a short-term cost one pays for being late in the money compounding party of a good business.

Most of the good businesses sell at multiples of BV due to above average and sustainable ROE. Incase the business continues with it’s past performance and keeps reinvesting most (90% +) of the earnings, the immediate ‘low looking’ ROE for our capital starts to become respectable (20%+) from 5th yr. onwards.

On the other hand, market cap/our capital should (for idealistic scenario) more or less mimic the earnings growth all these yrs.

FYR:

|

Yr-0 |

Yr-1 |

Yr-2 |

Yr-3 |

Yr-4 |

Yr-5 |

Yr-6 |

Yr-7 |

Yr-8 |

Yr-9 |

Yr-10 |

Yr-11 |

| NI |

45 |

63 |

89 |

125 |

175 |

246 |

346 |

486 |

683 |

960 |

1349 |

1895 |

| Equity |

100 |

141 |

197 |

277 |

390 |

547 |

769 |

1081 |

1518 |

2133 |

2998 |

4212 |

| ROE |

45% |

45% |

45% |

45% |

45% |

45% |

45% |

45% |

45% |

45% |

45% |

45% |

| Dividend Payout % |

10% |

10% |

10% |

10% |

10% |

10% |

10% |

10% |

10% |

10% |

10% |

10% |

| Investors. ROE |

4% |

5% |

7% |

10% |

15% |

21% |

29% |

41% |

57% |

80% |

112% |

158% |

1 Like

Well there are no clear cut rules, if you will. If the high ROE/ROCE is due to high leverage then even a low PB may not cut it. That’s not theory; there was a time in early 2000s when shipping / offshore business showed the above; but then went kaput (Mercator / Aban Offshore) when the tide turned and leverage worked against them.

High PB need not be a negative in many business that require very little capital. In fact US tech firms operate at very very low equity; sometimes negative equity because of stock buy-backs. Also dividing ROE/PB results in Earnings Yiled or 1/P/E - so has no more information than you already have from the PE ratio (even as I find the PE ratio non-intuitive)

A general observation / drawback with a good number stocks in India that have structurally high ROE is that the firm tends to generate far more cash than it needs. That cash creates problems because (a) if it’s hoarded up it brings down Returns (usually Indian firms are not that acquisitive) and has a tendency for poor capital allocation (b) if it is given away by dividends / buybacks, it results in a HUGE frictional cost of taxes that effectively brings down the return again.

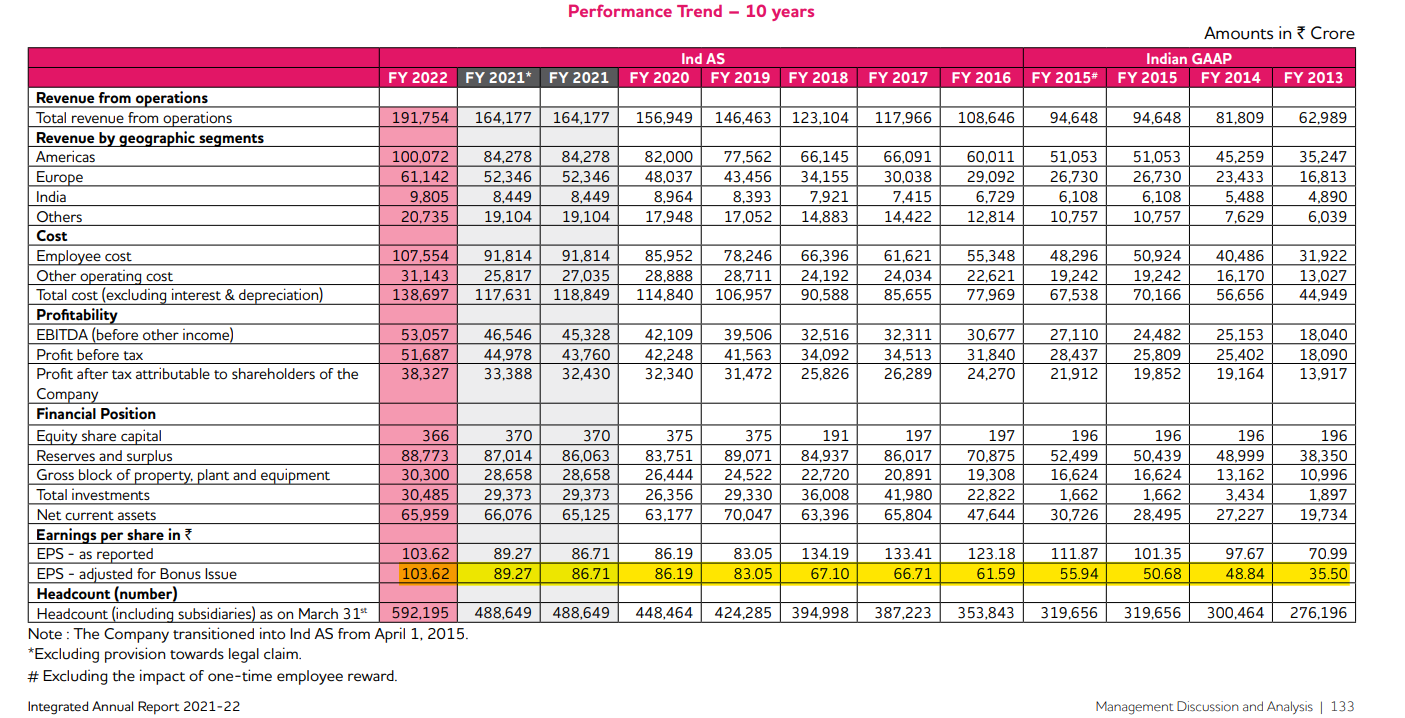

The same may be seen in TCS as well. While the magic of compounding shows a firm that retains the cash to grow at high ROEs dramatically increasing its EPS, reality is often the above problem (excess cash). The below shows 10 year EPS earnings of TCS from AR 2022 (highlighted in yellow)

You may see that the earnings for every share held grew by just 2.91 times, or about 12.5% pa, over a 10 year period, far lower than what its RoE of 40-45% with high retention may have indicated with continuous compounding. That’s because it pays out about ~ 75% of what it earns (dividends/buybacks). But then that 75% paid out to you will be lower by tax rate*dividend; typically resulting in 50% net payout. One may argue that any dividend can again be reinvested. However you are getting to reinvest only about 2/3rd of the profits and that creates a big drag on compounding.

To sum, most high RoE businesses do not compound their earnings per share as implied in the RoE; even as they maintain their RoE.

14 Likes

Interesting how head count ballooned in FY2022