Zen recently bagged a 35cr order from some Middle-Eastern customer which is 20cr for sale of equipment and 15cr as AMC, which will continue for four years. So three years of 15cr revenue guaranteed after sale of equipment. As per the article, the company expects the equipment order to be carried out within the next 3 quarters.

Anybody have any idea/rough figures of Zen’s margins in AMC business and in equipment sales?

Link to article: Zen Technologies wins Rs 35cr export contract in Middle East - Business-News-Today.com

Typically, after completion of the 20 Cr equipment order, there will be about 1-2 years of warranty period and the 15 Cr AMC will be @ 4 Cr/year for 4 years(approx) after the completion of warranty period. That is how you need to interpret the cash/revenue flows. This is my understanding of how orders work ,from some of their earlier calls.

2 Likes

Does anyone else think that the stock price at this point in time has left no margin of error for further investment?

Fundamentals:

At ~1500 mcap and ~500 P/E, it seems that all the expectations are priced in and market is either expecting their AMC business to ramp and/or for them to start getting bigger orders. Latest quarter presentation says that their order book stands at ~450cr, which is 1/3rd their mcap. With net profits margins that haven’t shown sustainability it is hard to assume what it could be in the future.

I have heard people talk about the negative list that the government announced, which included simulators that Zen makes. But has that negative list come into effect? I would assume order book would have reflected this by now if it had come into effect.

Techincals:

Since the recent run-up, the stock price has gone into a consolidation zone but I can’t directly equate that to market having found a decent price for future growth since it seems that the stock has since been on the ASM list (which to my understanding is that only a few PAN cards are doing most of the trades on a daily basis).

Is there something about the business I am missing here?

Disc: Invested from lower levels

1 Like

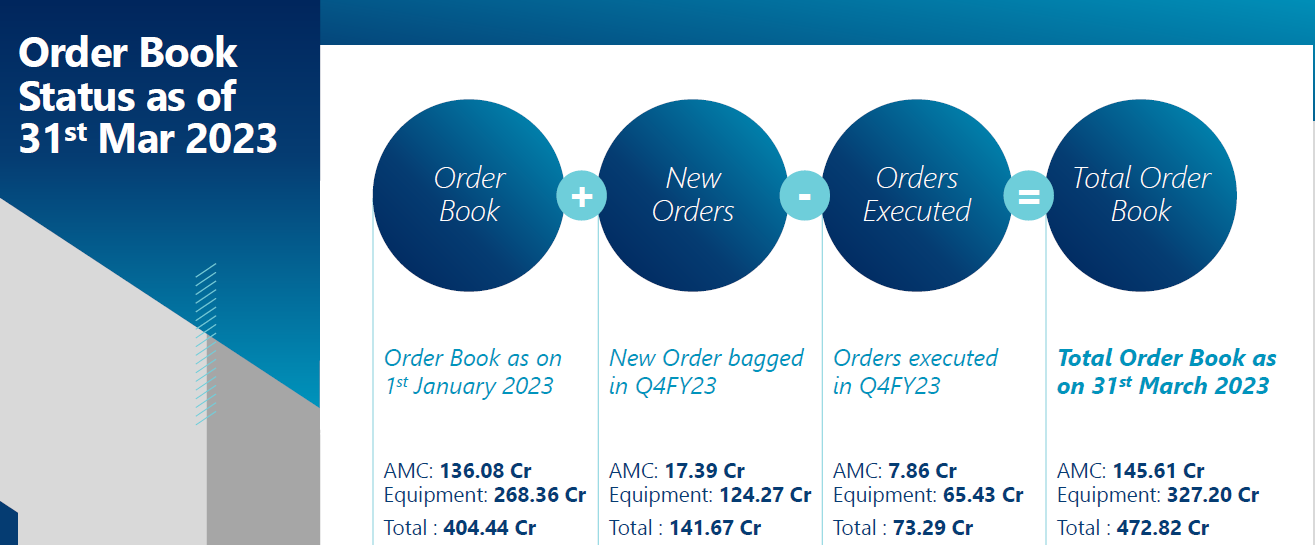

Current order book over four hundred Cr

Does Zen benefits with below announcement from the Government?

1 Like

Was studying the company recently from a quick fundamental perspective. Sharing for reference. Disclosure: Not invested. Please see attachment for more details

Zen Technologies - Quick Analysis.docx (26.6 KB)

CONCLUSION/SUMMARY

Market Cap: Rs 2500 cr; Price~ 300

PE: 48x (on annualised profits of Q3FY23)

Business Thesis: Niche player supplying simulation training equipment (design to after sales) for Defence (R&D spend is over 10% of sales). Revenue mix is 70% equipment sales and 30% AMC. Order book at Rs 404 cr is strong at 2.7x revenues with further orders expected, given that the company is the only player in this space. Net profit margins are as high at 20% and can lead to profits more than doubling to Rs 80 cr in FY24 if orders are well executed. Business, revenue flow and operating margins are lumpy, as it is a tender business; operations are highly working capital intensive. Scale can deliver higher consistency in margins and profits. Rakesh Jhunjunwala exited in 2013, under buyback @ Rs 70.

Technicals: Sharp upmove after cup breakout in week ending Feb 13, 2023; price more than 15% higher than 11 WEMA. Better to wait for tightening or pullback as risk return is not favourable now. RS and ADX strong

7 Likes

Just sharing, no position.

2 Likes

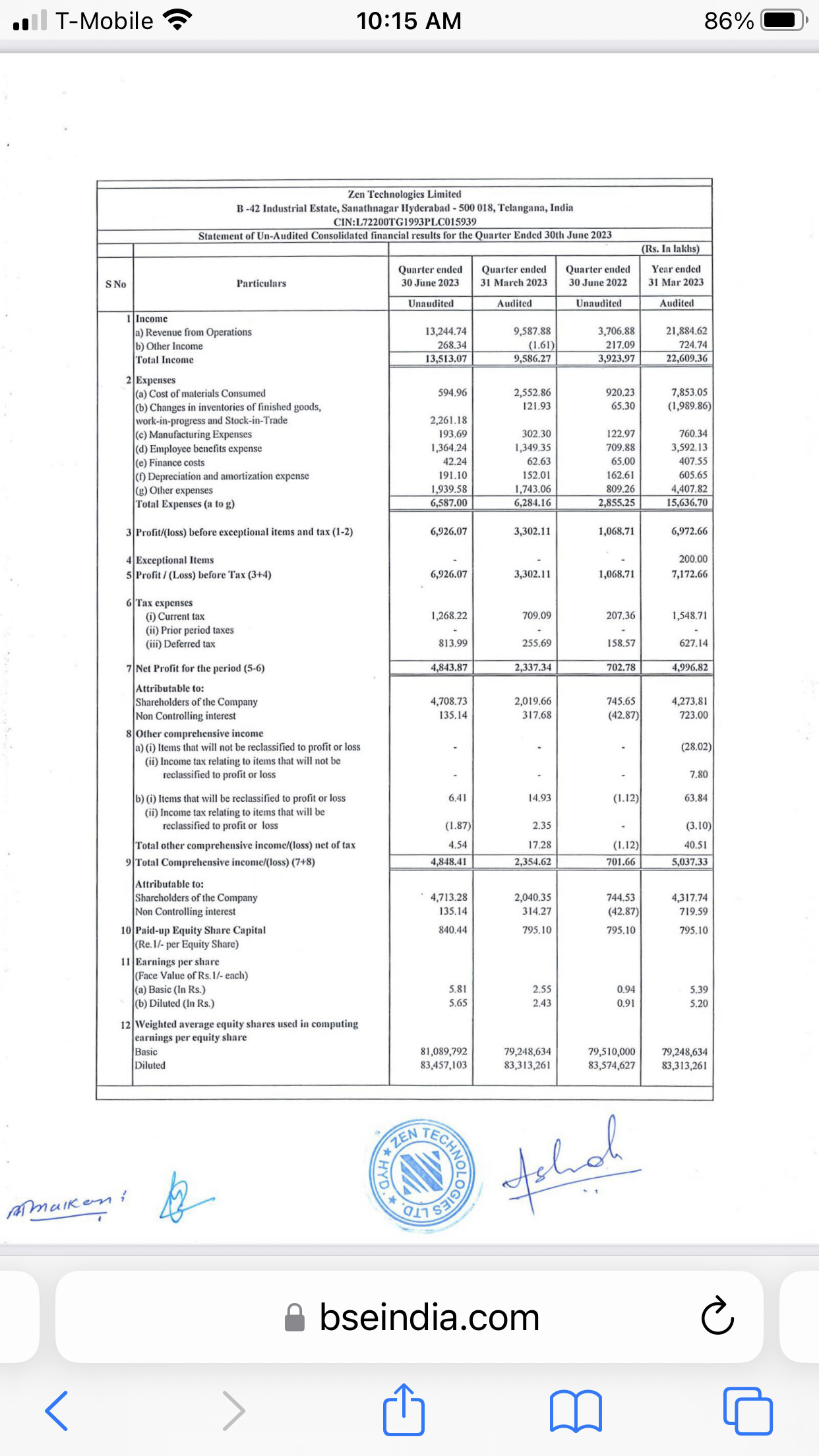

Very Good Results for FY 23.

2 Likes

1 Like

Zen Technlogies secures another major order of ₹160cr from the Government of India.

https://twitter.com/ZenTechnologies/status/1677198246354223104

2 Likes

I am a long term investor. I had here started a thread ‘Buying and Forgetting: Is it a Myth?’

But then experts also say that along with timing the buy right, it is also important to know when to sell.

The infrastructure, defence, railways, ev stocks are flying. They continue to get orders, so market is going ga ga over them.

But they are also becoming expensive. For example, Zen Technologies has a PE of 110! And this is not the only stock where the valuations have run so high.

So, too expensive is something which is costing more than its inherent value.

I would like the views of more experienced investors here.

Disclaimer: I have a small investment in it.

2 Likes

I would not term myself as a very experienced investor and had positions in Zen Tech which i exited when the PE went close to 120. Nothing wrong with the company, it is just how the market is reacting to the latest news, getting an order is one thing but execution takes time and the getting payment from Govt. itself is a task. From their concalls, they already have a backlog from previous orders which will be serviced this year. Getting new orders is good for any business, the real question is when will those orders get booked into actual operating revenue.

Disc. Exited but still tracking for potential buying opportunities

1 Like

A great time to be a shareholder in Zen. As per Q1 con call I have worked out below please correct if any mistakes. For FY24 he had said 3x Fy23 but then had changed to 450CR Revenue so i have assumed appx 500cr given the current order book.

Q1FY24 Rev 132.45CR PAT 47.1CR EPS 5.6

- Huge improvement in the quarter, they have made more profit in the Q than they did the whole of last year.

- Sitting on order book of over 1000cr post 500cr of order booked in July.

- They feel story has just started.

- AMC was 7.68CR and Equipment was 125CR in Q1. AMC revenues was targeted to be 115CR this FY will they achieve that?

- Simulation framework from MoD that was announced by the gov has been a godsend for the company.

- 275CR cash in the company

- Export break up - Sims - 25% Anti-Drone - 75%- mainly Middle East and africa

- Future pipeline - Still might confirm some orders in Q2 with domestic orders. Overall there is a huge sense of urgency in both sims and anti-drone. Market size should be 15000cr for sims over the next 2 years

- 18 months should execute 1000cr order book

- EBIDTA margins are sustainable at 50%

- Internally they have targets for growth which he has described as ‘obscene’ but they will not share numbers - fantastic 3-4 years.

- FY24 will be 3x FY23 and FY 25 - 2xFY24

- BHEL is competition but not much other domestic competition in antidrone. 3-4 RFP for anti drone and he is confident of winning.

- Not much competition in simulators, army sims especially they are very strong domestic driving sims etc there is some competition.

- Has 8.5acres land available for CAPEX if really needed but dont have many capex plans at the moment.

- May look at acquisitions but otherwise will return to shareholders, doesn’t seem to be anything in pipeline.

- Only risk is China doing a blockade of Taiwan

- They are very successful in winning orders and are currently participating in 400-500cr orders

| FY23 | Q1FY24 | FY24E | FY25E |

|---|---|---|---|

| 220CR | 132CR | 500CR | 1000CR |

| 50CR | 48CR | 100CR | 250CR |

| 5.38 | 5.6 | 11 | 25 |

9 Likes

Another Order worth of 65 Crore:

5 Likes

Total order book - 1450 Cr

AMC (incl above) - 250 Cr

Timeline - 18 months

FY24 - 500 cr

FY25 - 800- 1000 cr

PAT - 25%

EBITDA - 35%

Export / Domestic - 50:50 - next 2 years

Edge - Indian IP . Rest all have IP taken from outside.

Chnages - Regulartory changes - Move to stimulators is mandated / International Defence issue and inadequately trainded personned. Conter drone is more imp than drone. new threat

Export - friendly countries. Govt promoting Indian IP companies

Cost of manufacturoing is very low due to 30 years of reserch. if someone import, all margins go there.

6 Likes