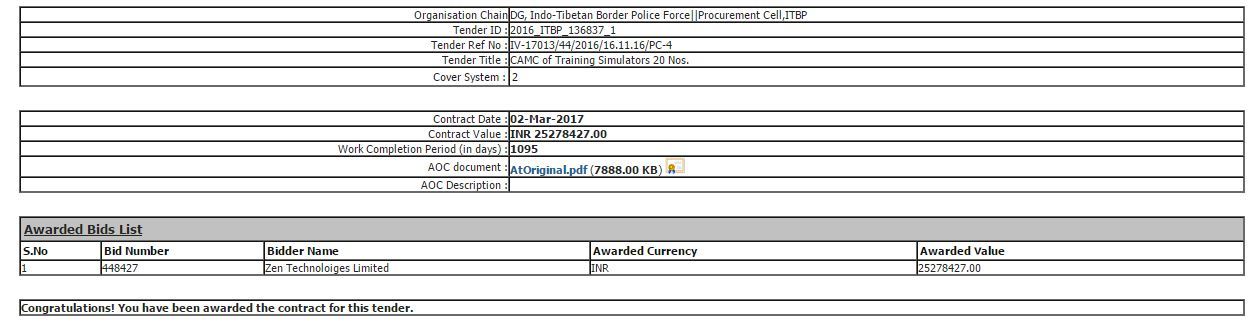

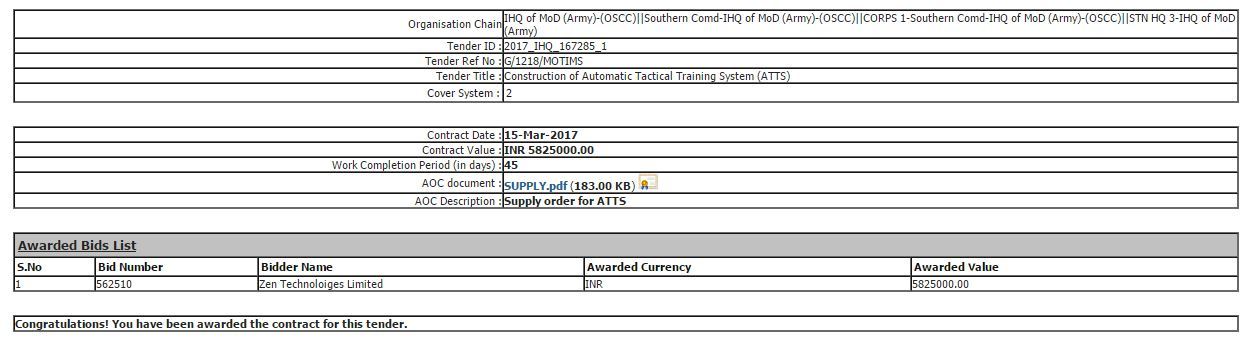

Another recent order win for Zen Technologies. Although these are small tenders, finally the logjam seems to be clearing.

2 Likes

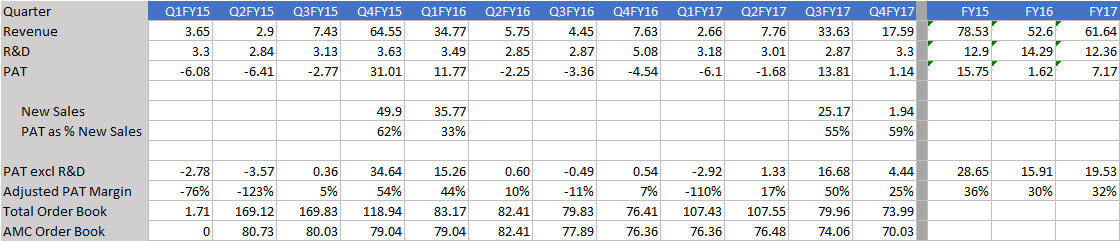

Zen Technologies came out with a poor set of numbers - as expected ![]()

However, the company is on the cusp of an inflection point. This company is earning 30% PAT adjusted for the R&D expenses. Once the large orders from FY15 start kicking in on the AMC side, the company will have the cushion to absorb all the incremental R&D. Hence all new orders will directly hit the bottom line. Interesting times ahead!

Disclosure: Invested.

2 Likes

http://www.bseindia.com/corporates/anndet_new.aspx?newsid=a3a5515a-50d8-4d1b-82e1-a5e18a8b77ec

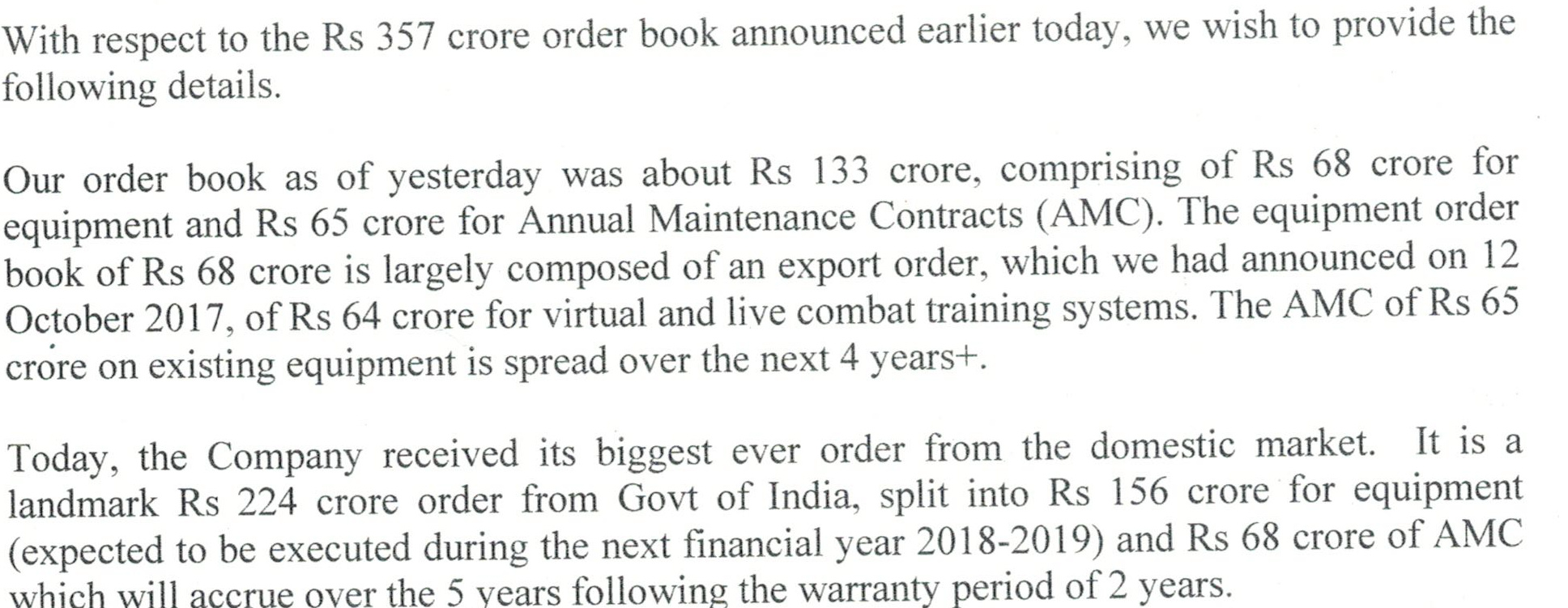

We hereby inform that the Company has signed the biggest export order till date of about INR 64 crores. Zen Technologies won the contract for live and virtual combat training systems against tough international competition. This order is expected to be executed in the first half of next financial year 2018-19.

Export business slowly picking up.

This appears to be a great news that allays ( to some extent) one of the fears I had on the Company - Since it supplies to defense segment / where generally L1 wins over the best quality. I was thinking that the Company may not be able to get export contracts where high quality is a key decision maker.

Great announcement of order book over the last couple of weeks. Augurs well for a multi year performance and things seem to have just started.

A shout out to all experts on this counter…Pls validate my thought process and share your views.

With Zen Tech @ 118 wanted to do some back of envelope calculation to get to the expected EPS for the next yer to determine possible target.

Historically over the last 5 yrs for a topline avg of 60crs, avg expenses were aprrox 55crs and an avg bottomline of 5crs. Looking at the averages because Zen been a product company once we have identified the approximte fixed expenes for the year, we could try to extrapolate the same for a higher topline.

For the next year the company announced the equipment orders of 68crs + 156crs = 224crs

Plus an exiting annual AMC of approx 13crs which was also mentioned in the annoucement send to the stock exchange.

So approx topline of 224+13 = 237crs (for now ignoring any other ongoing project income). Lets keep a conservative number of 190crs topline.

If double the expenses to 110crs, the bottomline comes to approx 80crs. Additional 30% downside buffer gives bottomline 54crs.

Even a 54crs bottomline will mean 8-10 times increase over the avg of last 5 yrs.

At the bottomend of 54 crs and with an equity base of 8crs, EPS comes to 8 and @ 15 times comes to price of about 120 and 20 times comes to 160.

Back after a long time. Bhai your top line calculations are fine not about expenses. This is not a services co that will double its expenses with sales doubling. With product cos the great beauty is of a J curve effect. To that extent my estimation is of a 15 to 19 Rs estimation for a turnover of approximately 230 crore.

3 Likes

Anyone tracking this can highlight what is recently happening with Zen? They invested in US arm and acquired some stake in another company. Some insights into it?

I attended Zen Tech AGM for FY19 & following are some notes ->

Investor PPT

PPT that was presented in AGM can be found below ->

Notes

- Most defense companies get their technology from DRDO, Zen created its own IP

- The company has installed close to 1000 simulators so far since inception. 825 supplied in last 2 decades. Average life of a simulator is 15 years.

- Zen Corner Shot - this simulation product provides count of hits & misses which is missing in actual training.

- The company had 1 product in 1993 & today company has close to 50 products.

- The company estimates that training requirements of Indian army is 8000cr. (This is company’s estimate & actual sales might vary). Global market size is estimated to be 8bn $.

- Company’s business model is based around 4 pillars - simulators, combat training centers (CTC), annual maintenance contracts (AMC) & exports

- Competition - Mahindra, L&T, TATA. The company claimed that these players have stopped competing because they did not have good after sales support.

- Based on cost saving calculations of company, CTC product payback is < 1 year.

- The time taken for actual live training is 1 day which can be drastically reduced with simulators.

- The company has no done any offset business so far - because that opportunity is for manufacturers & company is not the manufacturing company. The company wants to focus on IP creation.

- Regulatory tailwinds - Make II & IDDM regulations allow orders to be supplied by single vendors & this shall help Indian innovators like Zen. Above recommendations were finalized despite not being present in Dhirendra Committee report.

- The exports are ~5cr/quarter.

- Change in export mindset - The current government has instructed embassies around the world the facilitate sales of defense products from Indian players. Defense attaches & even secretaries come to export exhibitions and the are being asked to support Indian private industry.

- The company had won 224cr (160cr equipment, 66cr AMC) order in previous years. 57cr was supplied in FY19, 45cr was supplied in Q1 FY20 & rest of the order will be executed in Q2/Q3FY20. AMC contract starts after 2 years & it is for the duration of 5 years.

- The company has bid for 5- contracts. Axis Cades, Mahindra are other players who have bid. The last tender was awarded 2 years back.

- The company is working on sales funnel of 1200cr (domestic - 600cr, exports - 600cr) over next few years. These consists of 6-7 orders on domestic side. The company expects 1-2 orders to come through in near future & is hoping to cross sales of 100cr in FY20.

- The process to get NOC for exports is faster now. There is no restriction on exporting high end products as well as sales are to friendly countries.

- In simulator segment, 95% of domestic sales are captured by the company.

- The company expenses out R&D expense as & when it happens. Assets created through 250-300cr of R&D are not reflected in balance sheet.

- The company closed the Himachal Pradesh plant in 2017 & all the assets have been moved back to Hyderabad.

- Next generation - Arjun (Purchase) & Anisha (Admin) - are getting involved in the company.

- The company is also working on futuristic battle products like - drone simulations, drone cities, AI etc.

- The acquired company - Unistring Tech Solutions (UTS) - has expertise in Radar simulation.

Disc - token position to attend AGM, not a buy/sell recommendation. Mistakes are solely mine.

9 Likes

Very poor results for Q2. In AGM if they have spoken about completing orders during this quarter than it has definitely not happened… Hopefully management will provide some statement to quell investor concerns.

q2.pdf (1.1 MB)

My 2 cents on the business:

- Product revenue (~85% in FY20) is lumpy in nature – in FY17 it was INR 49 crore which de-grew to INR 18 crore in FY18 and grew to INR 70 crore in FY19 and INR 127 crore in FY20 – historically this has impacted the company’s profitability metrics (especially in FY17).

- Management has consistently highlighted that increasing competition due to entry of foreign defence companies (through alliances) may adversely impact its profitability

- While Management has talked about growing the services revenue stream in their MD&A commentary in the last 2-3 years, the same has not been reflected in the financial performance of the company

- Management has been highlighting that there are large export opportunities in Middle East, CIS and Africa since the last 2-3 years – they received an order of INR 64 crore in October 2017 – but post that there is no commentary on additional export orders

- The Company major customers are Government, Government Bodies and Government Controlled Agencies – which may delay payments though usual credit terms are 30-45 days.

- The business is working capital intensive – average DSO for FY18, FY19 and FY20 has been upwards of 120 days – receivables as a % to revenue was 58%, 80% and 30% in FY18, FY19 and FY20 respectively. They seem to have collected some old receivables in FY20. In FY19, they had to borrow ~INR 32 crore working capital and do a preferential issue of INR 20 crore due to the increase in receivables from INR 23 crore in FY18 to INR 73 crore in FY19.

- Due to high working capital intensity, the business will need to either (a) improve its collections (b) draw working capital to grow in the future. Improving collections will be a challenge given that its clientele is Government – so it will have to avail working capital lines and/or keep raising funds to grow.

Disc: Not invested; not tracking

1 Like

Not sure if anyone is still tracking this company but they have had some interesting developments. All their simulators have been added under the none import list and even though this may just be in spirit since Indian army hasn’t been using European or American simulators but it signals good intent.

Their drone detection and neutralisation system can be a massive opportunity not only for the defence forces but also the private sector where the procurement cycles are much shorter. Attaching a PDF of their ADS and inviting views from people with more knowledge on the matter zen-anti-drone-counter-drone-system-brochure.pdf (3.3 MB)

Any news on the order book pls share

Their order book is shared in their investor presentation of Q3 results

AMC book = 125.75cr

Equipment order book = 73cr

Thanks for the information.

I came to know about this company through this forum only.

Its business model surprised me.

The last interview on cnbc through some light on the business prospects.

The promoter was saying about getting business under Aatmanirbhar scheme.

If anyone has the information pls share.

New Drone Policy by the Govt. Will it not help Zen Technologies?