Curious about whether your investing style is agnostic to thematic opportunities @Yogesh_s , the reason i ask is the improved earnings momentum from a temporary industry disruption is unlikely to lead to a profound change in targets derived off longer term projections, given the inordinate weightage the terminal growth and discounting assumptions will logically play.

Admittedly, this boils down to being able to be astute where timing of entry and exit is concerned but the payoff seems worthwhile if discipline is maintained.

A specific opportunity i’d like to get your opinion on is with respect to the API production disruption in China and more specifically the potential for a company like Hikal to benefit from this. My DCF based valuation yields a roughly 10% upside but the possibility of heightened profitability over the next couple of quarters makes me keen to set up a small position despite minimal margin of safety

@akbarbadri

If a company is going through earning momentum, I incorporate that in future cashflow expectations and discount that to arrive at present value. Depending on how long the momentum continues, I adjust the cashflows accordingly. If the momentum is expected to be short term and unlikely to have any structural impact on profitability of the company then DCF will not show any material impact on the fair value.

To me it looks like your DCF valuation shows only a 10% upside but you think in the short term stock could trade at higher valuation due to earnings momentum and near term returns could be higher than 10%. It’s possible if others think the earnings momentum could last longer than what you expect and price the stock accordingly. But this rationale banks on greater fool theory. If you think the momentum is only temporary (and that’s why your valuation shows only a 10% upside) why do you think others will think it will last longer and price the stock higher?

In some cases, when a company reports good numbers, investors get excited and extrapolate that to 10 years and price the stock accordingly. If you see evidence of that happening, you can take a position. However, when the company reports bad numbers, investors extrapolate that also to 10 years and send the stock crashing.

Specifically for Hikal, I don’t like the company due to its poor ROE/ROA, poor working capital management and high debt. I don’t think investors will get excited if it posts good numbers for a quarter or two. It is already trading at a PE of 21 and even that is trending down.

Very much appreciate your well thought out and articulated response Yogesh!

To answer your query about why i believe others will think growth will last longer than it actually might:

a) i’m a believer in semi-efficient markets vs perfectly efficient ones, so bouts of euphoria from spurts of growth could result in a dislocation from sound valuation principles amongst investors as you suggested

b) in markets like today where there is considerable herding amongst investors (given that regulatory or valuation hurdles have resulted in a very limited quantity of investable companies),people tend to overpay for ephemeral growth believing its a better alternative to alpha generation vs similarly valued companies who havent experienced a sudden spurt because of the outside chance this growth will be sustained

c) Growth and its longevity are the parameters with arguably the least predictability ergo the biggest dispersion in models in my opinion

I do appreciate your views on Hikal as well! If i may pose another question: In your past experience trading Indian markets, which companies have proven to be most resilient during downturns outside of the large cap / blue chip names ?

Hi Yogesh,

From Beekay AR, I see below growth triggers

- The company intends to monetize its large land bank in Howrah (off Kolkata) and use the proceeds to invest in its core business.

- The company intends to enhance the utilization of its TMT bar capacity and embark on doubling the capacity through another plant of a similar size across the next couple of years.

- The company intends to extend its business into a new product segment (flats) through a jobwork engagement with a large Indian steel manufacturer.

- Any idea how these will help the topline?

- How do see the steel demand for next few quarters?

- Any other growth triggers for the company apart from the above?

Thanks.

Hi @Yogesh_s Sir, you used to have coal india in your portfolio. Are you still having it? I think coal india gives good dividend. But in term of growth, I dont see company growing. So wanted to know your thoughts?

Semi-efficient markets and herding behavior can work against you as well. The way it drives prices higher, it also drive prices lower. So if you are banking on getting the timing right then you have an advantage.

The ones that did not go up a lot during the upturn did well during the downturn ![]()

I know this is not the answer you are looking for but most cases will fit this narrative. There are not many companies that proved resilient for two or more successive downturns so can’t count on many to be resilient during the next downturn. FMCG companies, companies with growth visibility, companies with low debt are generally resilient.

If a company derives most of its value from terminal value in a DCF model, a hiccup for year does not really have a lot of impact on valuation. However, when companies reports a bad year, investors tend to extrapolate that 10 years and sends the stock lower. Only when they are assured of long term growth and terminal value, they tend to ignore bumps on the road.

Beekay will benefit from growth in capacity as they are already operating at near full capacity. They make TMT bars which is a commpdity so there should not be any problems in finding buyers. They also export so market is large for their products.

Steel demand doesn’t very too much from year to year. I don’t really track quarterly demand / supply situation and Beekay is a rolling mill not an integrated steel plant so lower prices and higher volumes will be good for them. They are likely to report inventory losses in Q3 but volumes should be good going forward. Construction activity is picking up so demand for TMT bars should be good. Auto is slowing down so flat product demand may be soft.

How quickly they build capacity and how quickly they ramp it up is the key. I think they are conservative so they won’t spend too much too quickly. Last time they did that, they were sitting on underutilized capacities for a while so I think they will be cautious going forward. \

Stock price can grow due to rerating if they maintain margins as they are operating at high utilization.

I don’t know what is the value of the Howrah land bank and if they are likely to actually conclude a sale anytime soon. If that turns out to be a high value asset and benefits of the sale flow to minority investors, there will be some rerating.

I sold Coal India in 2017 as higher employee costs were eating into dividends. Company was also not able to ramp up production and inventory was growing at power plant pitheads.

Dividends cannot be looked at in isolation. Its the total return (dividends + capital appreciation) that matters. I think Coal India, even if dividends continue to come out, capital growth is uncertain.

Are you still holding Eris Lifesciences?

I am!

I have exited my Eris position last year. I still like the company but I was not comfortable with the high valuation and the growth rate that they are likely to grow. until now their bottom line is has grown much faster than their top line mainly because of rising margins but margins are unlikely to go up further and future growth will come top line growth. Recent acquisitions are taking longer than expected to make an impact on bottom line.

Top line growth organically will be limited to 10-12% and some more can come from acquisitions. I am generally skeptical of growth from inorganic route. Long term company can deliver 15% cagr but I was not comfortable paying 35 times earnings for that when there are better bargains available elsewhere.

I can still consider this if price falls further as business is stable and balance sheet is good.

Okay! Thank You sir!

When I recently spoke to an employee he was really upbeat about the company and was telling me about the Medtronic JV and how the management is very cost sensitive.

I am now much more confident about Eris than before although I totally agree with the points you have raised. Growth is slow and yes acquisitions are taking too much time to throw up numbers!

Yogesh,

Do you see Yes Bank under Rs 170 now…, soon to go under new leadership - a value pick / buying opportunity for 1-2 years horizon?

Would you include this in your top 10 portfolio?

Going through this thread, I realise Dec 2018 post suggests Yes Bank already included in 2019 portfolio… all the same your comments on the current range bound stock price movement welcome.

how would you classify the current scenerio where the consensus is pick up in growth is going to come but prices are falling(esp for the small and mid caps).?

Do you take a contrarian view to what the street is saying or what it is doing?

My contrarian approach is described here.

We all have a peculiar investing style that suits our temperament, skills, experience, biases etc. Typically such a style has been developed over several years of mistakes and successes. However, we all know that it doesn’t work all the time and that’s true even for most successful investors. This is because market at different stages of the bull-bear cycle reward different styles differently.

I am not trying to find a style/strategy that works all the time because I don’t think there is such a strategy and even if there is one, actual outcome will depend on how well it is timed and executed. Instead, I have been thinking about what strategies work in different stages of the bull-bear market cycle and how can we adopt those and more importantly time it and execute it well. This is like trying to select right type of clothing for different seasons of nature except that different phases of the market cycle are not as predictable as seasons of the nature.

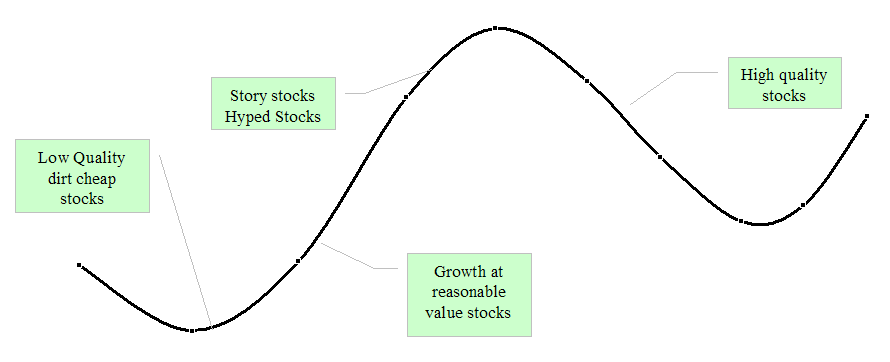

Chart below represent different types of stock that outperform during different phases of bull-bear cycle.

Stocks that outperform in different phases of market cycle.

This diagram is prepared based on my experience of several bears and corrections watching low quality stocks posting huge returns, hyped stocks reaching unbelievable levels, spectacular crashes, secular growth stories, die-hard stocks etc.

For years I have been focusing on growth-at-reasonable-value approach to investing. That’s been my style. As this diagram suggests it does not work all the time as growth stocks don’t grow all the time and even if they do they don’t remain at reasonable value all the time. Especially during the bear markets, its frustrating to watch prices go down when companies are posting good numbers. That’s because the style is out of favor. Its like wearing shorts in winter.

In a market like we are now, we can see that high quality stocks like HDFC Bank, Asian Paints, HUL, TCS etc just refuse to drop while low quality stocks are unable to find a bottom. But when market turn, these low quality stocks will be the biggest winners to the frustration of the stock pickers who focus on quality. However, such low quality stocks quickly go out of favor as sooner than later price catches up to their fundamentals.

Action then shifts to growth stocks that are still selling at reasonable value. Depending on how long the bull lives, and economy remains in goldilock state, these stocks can provide good compounding.

Eventually though, herds drive their valuations to dizzy levels and the only ones that appear fairly valued are the story stocks or hyped stocks as their valuations are not based on tangibles like sales and earnings but intangibles like future prospects, management vision, emerging moats etc.

Such castle in the air stories finally begin to crumble under their own weight and we know who’s swimming naked. Strong, high quality, somewhat unexciting companies with proven track record suddenly appear good investments and such stock defy gravity and stay strong while rest of the market rapidly reverts to mean and then overshoots on the downside. And the cycle completes, only to restart.

Investing in each of these phases require different skill set and temperament and that’s the reason no one can beat the market all the time. Its difficult to switch from one style to another quickly, if at all. Imagine someone selling HDFC and buying DHFL. Timing is the key here since strategies quickly go out of favor.

Sticking to a strategy that works over a market cycle is not a bad approach but one must understand when their strategy is unlikely to work and its better to stay out of the market rather than trying to outsmart the market with skills that have little chance of success. I have to say I learned this lesson the hard way.

What’s worst is adopting the strategy that has worked in the recent past. Its like wearing winter jacket just when winter is ending. Its like switching to HDFC after losing money in DHFL. Personally, I am testing waters with strategies that I either haven’t practiced until now or didn’t time it well. Will know in a year if I sink or float.

Wish I could give more than one like

Dear Yogesh, this is one of best comments and analysis i have ever read on valuepickr. You have a lonh way to go. Great summery.

Dear yogesh

I would suggest that you read the book by Ken Fischer " the only three questions that count" . I did read that few years back and it has real practical info for investing in different market cycles. The book kind of categorizes investment in two scenarios , first where the interest rate are high and hardening and second when the rates are falling and are low. There is also a detailed chapter on the yield curve and how to use it a leading indicator for investing. I did find the book pretty useful and will update as and when I reread it .

Regards

Divyansh

Respect sir  Hope you can start your blog or write a book someday. You are able to convey a lot effortlessly and it’s always straight to the point.

Hope you can start your blog or write a book someday. You are able to convey a lot effortlessly and it’s always straight to the point.