@Yogesh_s I like the way you bring out different perspective . Here I would like to add some contra points so that we all can learn more …

Lets start with your theory that High quality stocks do well in market downturn . Lets go through a piece of history from US market in 1970s when it suffered 10 year downcycle from 1972 to 1982 …

This was unique time when in down cycle high quality stocks did lot worser than other index stocks .

Why did this happen ??

Is there a lesson for all of us to learn ,. Currently we have a similar situation in Indian market … when few stocks are trading at crazy multiples and rest of market has been in grip of bear market . Would like your thoughts on the same …

Hi @Yogesh_s, wondering if you’re still tracking NGL Finechem? This came under my radar recently and I think it’s on the verge of good prospects ahead with their Tarapur plant expected to start operations soon. Can you please share your views if you’re following it?

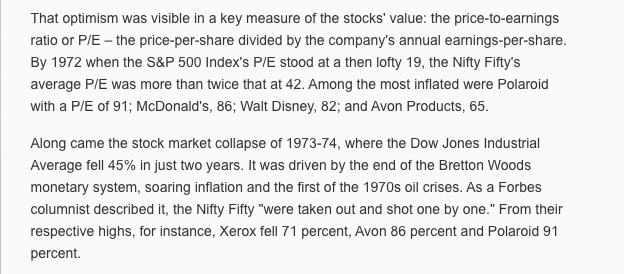

Late 1960’s saw emergence of ‘quality at any price’ investment philosophy. After WWII there was a surge in GDP growth coupled with emergence of corporate management as a profession (especially after work of Peter Druker). Both these factors together gave rise to fundamentally strong companies that posted a long stretch of consistent growth over several years something that investors never really saw before. Such consistent growth led many investors to believe that fundamentally strong companies can be bought at any price and held onto forever. No large economic shock hit the US economy until 1974 so this theory was never put to real stress test.

A series of macro events that hit the economy in mid 1970s acted as a wake up call. Not only did the valuations came down, earnings also came down. combined effect of this resulted in one of the worst bear markets.

Many Nifty Fifty companies as they were known actually lived up to their reputation for growth. They grew into stronger, bigger better companies over next several decades. So investors were right about their assumption of growth, just that it could not come at any price. That’s the real lesson from this episode. Everything has a fair value.

Valuation is just as important as fundamentals. There is a misconception among members of this forum that value investing means investing after studying fundamentals of the company. That’s true but that’s just the first step. Next step is to value the company using the insights gained from fundamental analysis. And final step is buying the companies that are selling significantly below the fair value and selling those that are selling significantly above. Third step is really easy if you follow the first two correctly.

Valuation becomes more important when price goes up. one needs to be doubly sure that a company deserves a high valuation. Similarly, fundamentals become more important when price goes down. one needs to be doubly sure that long term fundamentals are intact in such case. That’s another lesson.

@vardhmanchhajed I don’t actively track NGL Finechem as I am not invested in it anymore. But this is a company without many moving parts so not much changes often any way. Its a small mid growth company with average fundamentals. I don’t see this company growing sales and profits 10x over next 5 to 7 years so unless the price drops to a real low, there is not much reason to get interested in it.

Okay! And I also saw your comment mentioning that you exited Salasar Techno. Just out of curiosity, what are you tracking these days and do you think that this is a good time to enter small-caps?

Thanks much!

Yogesh, just wanted to mention a study on Nifty Fifty that I had read a year back (don’t have source now). The study checked Nifty Fifty returns for 20 years from top and a few months before the top. Surprisingly, someone who bought collective Nifty Fifty at very top and held for 20 years made same returns as S&P 500 index. If someone bought a little early, they beat S&P 500.

Not saying that quality at any growth is good idea. Just that it’s not as horrible idea as losing 80% in suspect managements and certainly not as bad as we always think.

Problem is holding for those long periods with nil/negative returns, sometimes for multiple years is very difficult. Even the passive investors seem to churn their portfolios once in 2-3 years. The more often one tracks their portfolio, the more the certainty of churn because its extremely difficult not to act. One can’t underestimate the psychological effect of it, for the many minutes, hours, days, weeks, months and years that the effect gets to wither away the patience.

Daniel Kahneman puts it across more succinctly

“If owning stocks is a long-term project for you, following their changes constantly is a very, very bad idea. It’s the worst possible thing you can do, because people are so sensitive to short-term losses. If you count your money every day, you’ll be miserable.”

Someone who doesn’t mark-to-market his portfolio on a regular basis and for whom the money invested is out of sight, out of mind will certainly do well in these long periods perhaps.

That’s an interesting post and the way you juggle is inspiring. Can you tell how much cagr have you got over long term, say 5, 10 and 15 years, by juggling between defensive and enterprising? Thanks

You touched my favorite topic, low maintenance contrarian portfolio. So here it goes

CAGR returns for last 1,2,5 and 10 years are listed below. I started this in 2006 so 15 yr returns are not yet available.

CAGR Returns

Nifty 50

Defensive Investor Portfolio

Enterprising Investor Portfolio

Blue Chip 10 Portfolio

1Y

3%

13%

-9%

4%

2Y

10%

10%

7%

9%

5Y

11%

9%

13%

12%

10Y

15%

21%

17%

19%

Since Incp (Jan 2006)

11%

17%

15%

16%

Same portfolios but returns listed for each year.

Annual Retuns

Nifty 50

Defensive Investor Portfolio

Enterprising Investor Portfolio

Blue Chip 10 Portfolio

2006

40%

43%

58%

50%

2007

55%

17%

107%

62%

2008

(52%)

(28%)

(56%)

(55%)

2009

76%

76%

139%

82%

2010

18%

40%

15%

19%

2011

(25%)

(2%)

(35%)

(28%)

2012

28%

27%

44%

32%

2013

7%

31%

(2%)

10%

2014

31%

29%

43%

38%

2015

(4%)

6%

(9%)

(2%)

2016

3%

(5%)

7%

18%

2017

29%

8%

42%

25%

2018

3%

13%

(5%)

5%

YTD 2019

(1%)

0%

(2%)

(0%)

Finally, current portfolios

Defensive Investor Portfolio

Enterprising Investor Portfolio

Blue Chip 10 Portfolio

Asian Paints Ltd

Axis Bank Ltd

Bharat Petroleum Corporation Ltd

Hindustan Unilever Ltd

Bharat Petroleum Corporation Ltd

Hero MotoCorp Ltd

Housing Development Finance Corporation Ltd

Eicher Motors Ltd

Indiabulls Housing Finance Ltd

Infosys Ltd

Hero MotoCorp Ltd

Infosys Ltd

ITC Ltd

Indiabulls Housing Finance Ltd

ITC Ltd

NTPC Ltd

Larsen & Toubro Ltd

Power Grid Corporation of India Ltd

Power Grid Corporation of India Ltd

Maruti Suzuki India Ltd

Sun Pharmaceuticals Industries Ltd

Sun Pharmaceuticals Industries Ltd

Reliance Industries Ltd

Tata Consultancy Services Ltd

Tata Consultancy Services Ltd

Titan Company Ltd

UPL Ltd

UPL Ltd

Yes Bank Ltd

Yes Bank Ltd

Observations:

Over long term, defensive and enterprising portfolio returns are close to each other with defensive portfolio outperforming enterprising. I never really though it would but it did. I think next 10 years defensives may not outperform enterprising but they might given the history.

Both these portfolios outperformed Nifty 50 so selection matters.

Enterprising portfolio is hugely volatile with sharp gains followed by huge drawdowns.

Defensive portfolio is much less volatile with very little drawdowns (except 2008).

Whenever Nifty 50 produced decent returns (> 15%) it was almost always because of enterprising stocks. That’s probably why I kept on investing in them but key is to get out them after a huge rally, else the oncoming drawdown will offset any past gains.

Many of the defensive stocks are really boring but they did produce good returns in the long run. So keeping investing boring does pay off.

Given huge difference between performance of defensive and enterprising portfolios on an annual basis, a timely switch between these two should outperform Nifty 50. That has always been my objective. Key is to get in/out of enterprising stocks at the right time but that’s has proven to be the hardest part.

Portfolio may be defensive but we are talking about most aggressive(controlled) companies their respective fields which have huge addressable markets . So results are likely to be always superior.

Indeed thats the hardest part. Subconsciously I always knew that it may be time for switch but never did it until recently when I saw the pain of holding good (not great) companies in a downturn…i now want to practice this art…great to see you already doing it since many years and as expected this practice would have many learning in execution. It would be really helpful if you can mention the way you execute, the pointers you see, the risks and learning in executing the flips between 2 portfolio types…btw it’s amazing how much data you have maintained for every year!!

If the allocation % in the 3 PFs is different from Nifty-50’s then the two cannot be compared. For eg. the Index allocates 0.83% to Eicher, whereas the Ent PF may have allocated 5%. So the two cannot be compared.

Asian Paint, HDFC, HuL are solely responsible for the defensive pf doing well. So, the success of the 3 PFs over Nifty may be due to your ability to pick good companies out of the entire Index; and no other principle.

This way we will never be able to benchmark any fund manager’s performance vis a vis any index. A fund manager/stock picker can tweak both choice of stocks and allocation to each of those stocks.

Within large cap/NIFTY50 one can view it as an elimination exercise - decide what you do not want to buy/hold & when and your job becomes simple. Within mid cap/small cap it becomes an exercise in stock selection since one needs to zero in on those 15-20 names out of 3000+ stocks. For this very reason the ability to beat the market is highest in the sub large cap segment during most market conditions.

As long as one is competing in the same asset class and category, comparison can always be drawn as to which approach was better over a period of time. That is, compare a large cap portfolio against the NIFTY 50, compare a diversified portfolio against the NIFTY 500, Small cap portfolio against the appropriate index.

@ Yogesh - Returns calculated using XIRR (value weighted) or NAV (time weighted)?

What are your views on Hero Motocorp? A proven business selling a ~15 P/E and almost ~3.50% Dividend Yield. At least, I think it makes for a good defensive stock.

Comparisons are a tool for fund managers, to contrast their results with others and thus attract customers.

Whereas, for investors comparing/benchmarking is futile. Because returns are always risk adjusted. At the core of it, he is investing or managing his money in a particular way to suit his own temperament.

A future trader earns 4% a month on his net worth, but he also sees a drawdown of 10% on a regular basis. His temperament allows that level of risk.

A small cap investor regularly sees his investment thesis being turned into a joke, but he also gets paid handsomely when the going is good.

The point is, I think, investors amongst themselves should discuss various aspects of risks, operational discomforts or DDs (insecurities) he experiences in his style of investing. In efficient markets like ours, the returns will be commensurate to the risk one is taking.

Have you considered a strategy to mix up Defensive portfolio with some enterprising stocks ( lets say 70% defensive and 30% Enterprising) ? I hope yields would be even better.

Hi Yogesh, Did you evaluate any of below stocks for experimental stocks?

Thyrocare - I think need of health care service will keep on increasing with health awareness among people like getting annual health check up etc. Companies like Dr Lal path, Thyrocare will get benefit along with hospital business.

update - i heard con call of Thyrocare. It seems there is lot of competition with unorganised sector. Also i read Thyrocare thread and some people have raised concern over accuracy of thyrocare test.

Inox Leisure - As salary keep increasing and lifestyle also getting change, people will spend more and more money on food and leisure. So people will spend money on watching movies. Problem with Inox Leisure or any such business is the CAPEX requirement to open new multiplex.

L&T Technology Service - It seems company is into niche areas like robotic automation, Machine learning etc. I need to explore it more to see what all clients it has and geographies of the client.

update - i browsed through the company website. they are working in engineering related technologies. I dont think TCS or Infosys have such expertise. They are working in IOT. But L&T TS seems have edge since L&T is already expert in engineering related technologies.

Need your expert thought on it in case you have explored any of these companies.

I liked your philosophy of having defensive and enterprise stocks. I am also planning to follow it like putting 60-70% in large caps(blue chips), 20% in mid caps and around 10% for experimental ideas.