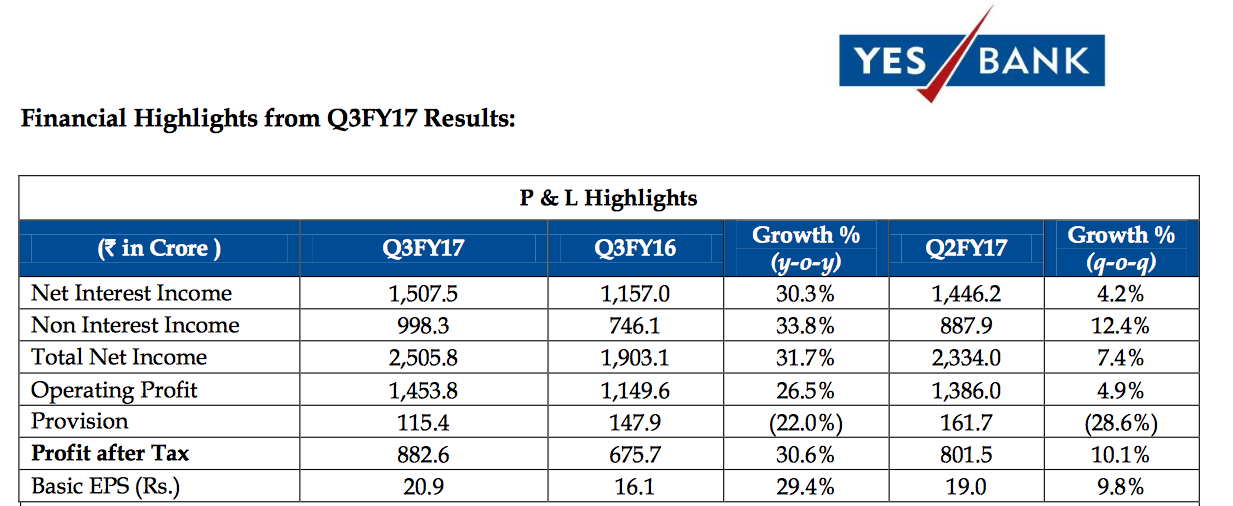

Yes Bank has posted good quarter from last few years.

Only thing people were interested is their NPA numbers and YES bank has posted reduction in GNPA and net NPA this will be positive for the market…

Yes Bank has posted good quarter from last few years.

Only thing people were interested is their NPA numbers and YES bank has posted reduction in GNPA and net NPA this will be positive for the market…

Sir, I recall the demon qtr also had a growth in profits YOY. Just to check I went on the BSE site to the result posted on 19 Jan 2017:

BTW, there is no mention of divergence in today’s filing. Does that mean Yes Bank and RBI’s assessments have converged?

GNPA and Net NPA declared by Yes bank has never been a problem. The problem is the divergence from the RBI posted NPA numbers for the bank. Going by the low NPA numbers disclosed by the bank, we have to take it with a pinch of salt till the RBI numbers are disclosed.

As per result slides, loans from the ones classified as standard in previous quarter have been recovered and there has been no delay or issue with recovery. Does this indicate that the RBI classification of NPA was incorrect and bank was more accurate in marking them as standard and not NPA?

Tho whole divergence saga was a false alarm if that is the case!

Jeevan

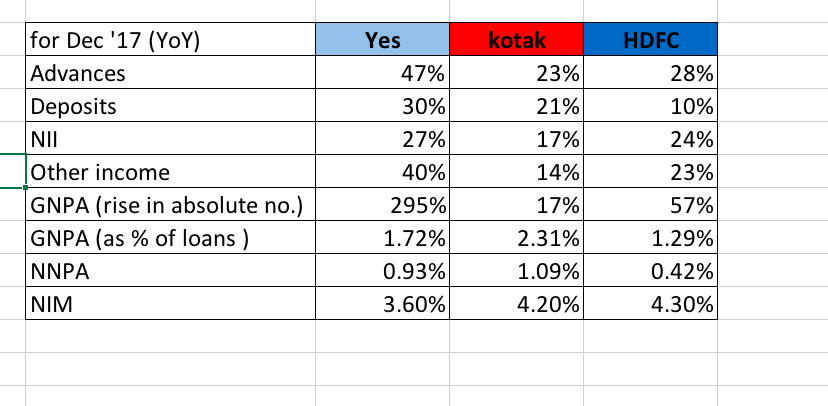

At this stage of the economic cycle, growth in advances is more important than asset quality.

Asset quality is important when GDP growth is slowing down as that’s when NPAs begin to rise and its not clear how bad its going to get. Now that GDP growth is picking up, worst of the NPA is behind us. Even PSU banks are reporting decent numbers. Asset quality will improve from here. There may be some book entries regarding recognition and divergences but situation on the ground will improve.

So the key moniterable is how the bank is participating in the up-cycle. At 46% jump in advances, Yes is ahead of the curve and with recent 5000 Cr QIP, it has enough ammunition to stay ahead.

FY 18 Q3 Concall Highlights (source: capital market):

Each of these three have some factors better than the other two e.g. advances of Yes are the best but NIMs are the lowest.Which ones out of 6 should get more weightage to draw a conclusion and the reasons thereof? Your GNPA (rise in absolute nos) is not clear.could you give figures for Yes indicating 295% rise in GNPA.

Thanks in advance

I think the interest rates are already going up in the system

Is it a matter of time when RBI raises the rates again?

If the rates raise NBFC’s and banks will under perform i am not wrong?

Just saw historical rate hike by rbi in 2011 to 12 where it raised multiple times to contain inflation

I think that time banks did under perform

Any insights on this theory?

PS Holding 1K shares

Era of consistent increase in Bank Rates:

19 Mar 2010 - 5% till 16 Apr 2012 - 8%

In this period, Nifty - 1%

HDFC Bank - 44%

Indusind - 103%

Kotak - 56%

Yes Bank - 54%

Era of consistent increase in Bank Rates - II -:

26 Oct 2005 - 6.25% till 30 Jul 2008 - 9%

In this period, Nifty - 80%

HDFC Bank - 79%

Indusind - 17%

Kotak - 223%

Yes Bank - 98%

Though 2008 is a different story.

I do not remember what exactly happened at that time. But a look at my transaction log reveals, I bought more, and in 2 years time it doubled from that price.

My thought process is, I only have a vote, but no say in how a company runs. So rather than trying to think what they should have done, I listen to what they did. That reveals their attitude and gives me enough clues if I should stick with that company or not.

All financials are getting beaten up? is this a reason rising yields or some large FLL’s are booking out due to LTCG benefits?

Yes, large FII sell outs - mainly due to global macros (and in line with global weakening of markets) and not necessarily due to LTCG

Really? DOW and other markets had been up yesterday while our NIFTY has fallen today!

In fact SGX NIFTY was up in the morning before market open following the lead of US markets but nevertheless we ended in red!

Not talking about one day market. Its the general market trend over the past 4 weeks across the globe (non-US markets)

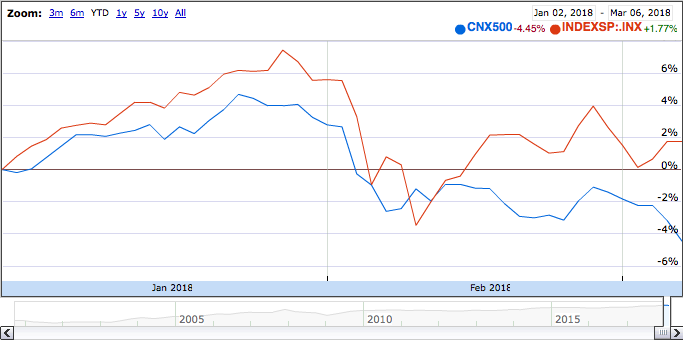

CNX500 v/s S&P500

If you see we have massively under performed US in 2018.

Despite rest of the global markets falling the markets in the US have been gaining in the past 2-3 sessions is because the increase in import tariffs augers well for US companies. However this may lead to a trade war globally and as discussed in the article, Europe and other countries might adopt similar strategies in

retaliation. In my opinion this was the

reason for the sharp fall in our markets in last hour. I won’t be surprised if the US market correct in next 1-2 sessions.

Based on the latest news feeds, fear about a trade war is already subsiding.

I am not sure what will happen in future. But fact remains that India has under-performed US and other emerging markets in 2018.

While many people attribute this under-performance to varied causes. I attribute it to two things:

In a group of hawks, doves, retaliators, bullies and prober-retaliators, when a dove fights a dove, they both make a lot of noise about doing this and that to the other knowing fully well that they will do damage to themselves in the process if they proceed and so the fight goes nowhere and ends without damage to anyone. When a hawk fights a dove, hawk wins and the dove loses but with minimal damage as it knows when to back-off. When a hawk fights a hawk, its blood until last-man standing.

When fights follow round after round in multiple iterations, one can have a memory of past actions and act accordingly. A retaliator will attack only if attacked. A prober-retaliator will start an offensive to test the waters and retaliate if there is retaliation or keep bullying. A bully will act like a hawk and when it meets a dove, will win always but when it meets another hawk, will run away.

With that background, Trump tries tariff on Steel and Aluminium imports. EU retaliates with tariff on Harleys, Levis and Bourbon and hits where it hurts - the American heartland. Now if the US and EU are both hawks, this could go on forever and could end up derailing international trade and globalisation but trade isn’t a zero-sum game and globalisation can be win-win (non zero-sum) which is why it has been successful so hawk-hawk strategy is improbable.

Now if Trump were a prober-retaliator and the EU retaliator, it would again be a similar to a hawk-hawk strategy leading to complete demolition. If Trump were the bully (most likely) and has met a hawk in the EU, in all probability, Trump will run away i.e reverse his stand. However, considering this is politics, this is in all likelihood a dove-dove fight with a lot of noise and no action - None of the tariff actions will be committed to paper and will go away after everyone has scored political points.