@phreakv6 You have beautifully articulated the whole situation. It will be interesting to see how it eventually pans out.

A TREAT, your description of the drama. Thanks.

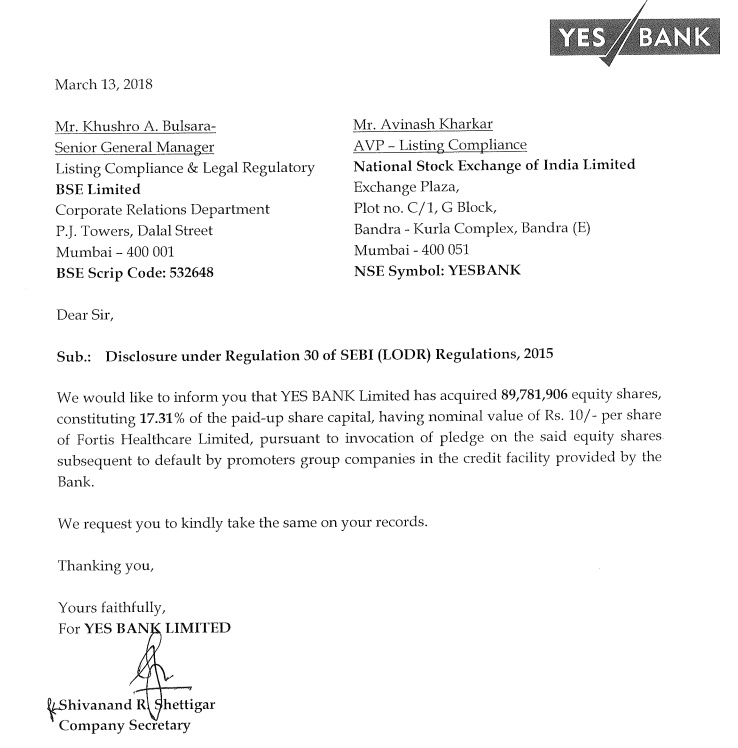

I understand Yes Bank gave personal loans to Singh Brothers against pledge of Fortis Health Care shares. As Yes Bank had acquired 17% stake in the company, it is clear that the Singh Brother has not repaid the loan.

Has Yes Bank declared that loans as NPA and made adequately provisioned?

And what is the acquisition price for these shares for Yes Bank?

given the fact that yields are rising…and yes bank seems to have a low casa ratio…will the cost of funds for yes bank raise and dent the profit spread ?

Any comments would be appreciated

P.S Invested heavily have 2K @ 350

1 Like

There was a time, I guess 4/5 years back, Yes Bank was dependent on wholesale funds. Since then Yes Bank has transformed themselves and their CASA ratio is around 37-38%.

On top of that, they are raising money through different instruments (like MTN, which I am afraid I have no idea).

Over the next few years, they are looking to increase their NIM towards 3.9-4.00 percent in next 2/3 years, which seems achievable in my opinion. Due to current PSU banks condition, they are getting an entry into big corporate clients, which they were finding it difficult few years bank. Yes Bank believes they can grow upwards of 25% CAGR for few years, which seems plausible if they handle NPA issues reasonably in the short term.

However, in the short term, there are a few headwinds like recent RBI guidelines related to declaring NPA. Additionally, RBI highlighted NPA divergence for the year ending FY15/16 and FY17.

I guess Yes Bank would take (hopefully) extra care this time in making sure that divergence for FY18 is less.

In Summary, short-term looks cloudy, but they are one of the big beneficiaries of value migration from Public sector banks to private sector banks.

Disc- Invested, so the view could be biased.

2 Likes

Thanks for your reply…Is there anyway we can know which sector does yes bank have most exposure rather have given more loans? now if you take all the NCLT cases are related to steel sector.but i think the biggest stress is in power sector…if they start assessing that more stress will be in the banks which have lend to power sector

1 Like

Plans to roll out the above solution to 2000 corporate clients.

4 Likes

Financial sector is ripe for disruption. As expected now age financial behemoths like Yes Bank, Indiabulls Housing Finance and bajaj Finance are leading in this area. Like other sectors, disruptee would loose their pants and disrupters will lead the next leg of growth.

2 Likes

In private sector banks, HDFC Bank, ICICI Bank, Kodak and Axis are big banks, so they do not have to make extraordinary efforts to protect their fort. Even if they try to match other financial startup ideas, they will continue to grow. However, all these private sectors banks are on the forefront of technologies themselves (if one read their annual report). They are using different technological innovations to acquire more customers and gain market shares.

Two years back, when RBI announced license to payment banks, the market got jittery about private sectors banks and sold their shares. Fast forward 2 years, I have not heard that these payment banks or new age private sector banks are giving serious threat to the private sector. I believe some of them would be struggling to keep them afloat, without raising further funds from investors.

I believe that these financial technologies are accelerating the movement of customer- big and small- towards private sector banks or startup in general, at the cost of PSU’s.

Sharekhan’s latest update on Yes Bank

“Probability of MTM hit due to Fortis stake sale: Yes Bank had acquired 8,97,81,906 equity shares (At a face value of Rs 10 per share) of Fortis Healthcare (FHL) on 16 February 2018, pursuant to invocation of pledge due to a default by promoters in the credit facility provided by the bank. Consequently, Yes Bank became the biggest shareholder of Fortis Healthcare (FHL) with a 17.31% stake in India’s second-largest hospital chain. The board of Fortis Healthcare announced the sale of its hospital assets to the Manipal-TPG combined along with the sale of 20% stake in its diagnostics arm in a complexly structured deal, which prima facie values the Fortis Hospital stake at a significant discount. Post the announcement, the stock price of the entity too witnessed a correction. A section of minority investors (collectively holding ~30% of Fortis shareholding), have opposed the deal and seeking to annul the deal apart from taking steps to replace the current board and call for a fresh and transparent auction process of Fortis to the highest available bidder. Hence, while there are several hurdles before the deal goes through, there has been a significant correction in the FHL shares post the announcement. Consequently, Yes Bank, as per our calculations is likely to see a noticeable provision due to mark-to-market (MTM) provision requirement in Q4 FY18E, which is likely to crimp Q4 performance and may be a dampener in the near term for the stock.

Outlook - Long term prospects remain bright, but brace for probable near term MTM hit: Apart from the probable adverse MTM hit scenario which may be an overhang due to the likely MTM provisions l crimping Q4 FY18E PAT expectations, we believe that the bank’s prospects remain bright. It has been proactively de-risking and ring-fencing its exposures over the period. As a consequence of these proactive actions and effective monitoring, we believe that Yes Bank may have only a minimal impact on its portfolio due to the pursuant to the implementation of NCLT Framework and IBC Loans. We continue to be positive on the outlook of the bank’s performance based on asset quality and growth.

Valuation: The stock of Yes Bank is currently trading at ~2.4x its FY2019E BV, which we believe is reasonable. Notwithstanding the strong overall performance and positive outlook, we believe that near term niggle of higher provisions can be an overhang on the stock performance. We maintain our rating to Buy, with a revised price target (PT) of Rs 360.”

3 Likes

Very little information by sharekhan.No mention of loan extended to FHC or the exposure amount being referred to nclt etc.

2 Likes

Bond yields to further go down

A critical article by Tamal Bandyopadhyay on Live Mint. Please read through this to understand the rot which may lie with some of the private sector banks.

I picked up few paragraphs of the article which point the fingers to certain banks. As I have limited knowledge about the inside happenings in the industry, I could not guess against whom he was pointing the fingers. People in the know how if you can shed your thoughts on these points could be enlightening to everyone.

-

It is being done by giving fresh loans to an arm of a corporation which is on the verge of turning into a defaulter. This practice of “ever-greening” is rampant in some PSBs, too, but private banks are more innovative. At times, they give a loan to an entirely different company with an understanding that the firm will pass on the money to rescue a defaulter. This art was first perfected by a large private bank and emulated by a few others.

-

There is another ingenious way of bad loan management. When a string of accounts are on the verge of turning bad, typically a pool of debt is created covering all, gets rated by a not-so-reputed rating agency, and is sold to relatively smaller banks, including cooperative banks. This practice of down-selling or palming off of bad loan has been invented by a private bank which enjoys the blessings of a politician, who also wields enormous influence on some of the cooperative banks.

-

Yet another clever way of managing bad assets is sanctioning two loans at the same time. While the first loan is disbursed immediately, the disbursement of the second loan is typically kept on hold and, only if a few years down the line the first loan turns bad, the second loan gets disbursed to help the borrower service the first loan. Thus, a loan does not become bad at least for three to four years.

-

The art of “creating” handsome fee income was perfected by a large private bank in the second half of the 1990s and early this century; later, a few other banks opted for this and, currently, one of them thrives on this. Why do the banks do this? Market valuation. The community of analysts and investors love fee income since it is considered a risk less steady stream and does not consume capital.

How does this work? Well, suppose company A is taking a Rs100 crore five-year loan at an interest rate of 13%. With the consent of the borrower, the interest rate will be brought down to 10%, and 3% will be converted into fee. However, this will be booked at one go and not amortized over a period of five years. That is Rs3 crore multiplied by five years, or Rs15 crore. For this, the bank’s sanction limit will be raised from Rs100 crore to Rs115 crore. The fees can be for processing and/or structuring the loan and, ironically, paid out of a bank’s loan itself.

By front-loading the fee income, the bank gets a lump sum at one go, which bolsters its profit. On the flip side, the bank will always be under pressure to book more and more fees every year to remain at the level achieved in the previous year. -

There has been at least one instance where a private bank diluted the importance of risk management. When it got a new chief risk officer (CRO) a couple of years ago, it changed the reporting structure. Instead of reporting to the CEO, the CRO was asked to report to the chief financial officer of the bank. By virtue of reporting to the CEO, the CRO would have been attending the board meetings by invitation; but now, that is blocked. In other words, in the new reporting structure, the board would not get a first-hand account of risks in the system. Incidentally, going by the Basel Committee on Banking Supervision Guidelines for Corporate Governance, the CRO should report and have direct access to the board or its risk committee without impediment.

For point (2) my mind says it could be the politician named Powar (you know whom I mean). But I am more interested to know which Bank Tamal is pointing fingers at.

As for point (4), my mind veers towards Yes Bank. Because this is one bank which has good fee income growth, a bit more than some other banks.

As for point (5), this appears to be Axis Bank. Here is the article which covers this subject.

14 Likes

Good information.The bank in question be either icici bank or kotak mahindra bank.The experienced boarders may pl. enlighten on the issue

Point 1 pertains to ICICI bank…they are pioneers in ever-greening loans made to large corporates.

A lot of these sound like ponzi schemes and will most likely end up in bust and bailout scenario. We are in general very good at papering over the cracks (jugaad), instead of permanent fixes and I think most of these are remnants of the 2008 crisis which we probably never handled with honesty.

This deleveraging cycle has started probably with steam only around 2016 when Rajan started to put pressure to disclose and account for NPAs in the system. No one wanted to reveal the rot at once but have instead been revealing them piecemeal which is just fundamental dishonesty.

In no other business is the product same as the unit of payment. You cannot pay your creditors will steel or toothpaste but in the banking business, you can. Self-referencing systems and feedback loops (strange loops) caused by such systems will invariably lead to booms and busts. This deleveraging is certainly the bust part of the cycle and it doesn’t look like its anywhere close to completion.

3 Likes

This is true for overall human behaviour.

When PNB announced Niraj Modi fraud, they announced with smaller number and them bumped up the number higher.

Similarly, a company announced layoff (more a developed economic phenomenon), which are then followed by subsequent lay off announcements.

Disseminating a bad news in pieces is quite common in the investment world, and Warren Buffet has aptly summarised this when he said: “There is rarely one cockroach in the kitchen”.

2 Likes

Not correct. As per Information available to me, this is not Yes bank, irrespective of amount of Fee Income in their books.

Also, Tamal had good but not the absolute understanding of Banking Industry. Many a times what he writes/has written is sheer hearsay.

1 Like

@Yatharth, we would love to hear from you more on this topic.

For point (2), someone said the politician name is correct as per the rumours and the bank happens to be Yes Bank.  Remember it is hearsay. But I am ready to trust the hearsay than the MSM, particularly TV channels on what the peddle.

Remember it is hearsay. But I am ready to trust the hearsay than the MSM, particularly TV channels on what the peddle.