If someone has on-ground experience in this field, I wanted to know two things:

What is the competition scenario. This would decide if the 12 to 15% margin will be maintainable in the future.

Is the cost of 1.25 to 1.5 cr per MW justified. I am unable to understand how Waaree is performing so well on margin front as compared to Sterling Wilson. Could there be any benefit due to the presence of parent group in manufacturing of modules?

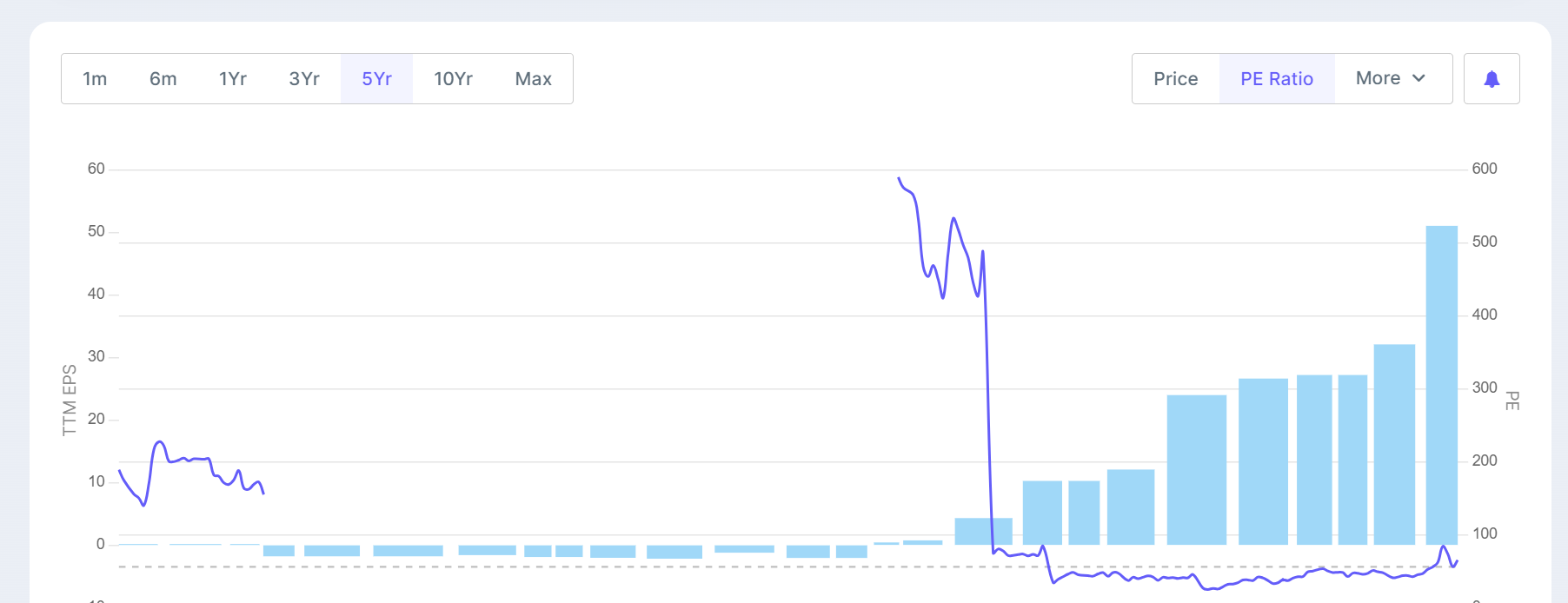

@Worldlywiseinvestors Sir waaree renewables sales growth Q3 2024 was amazing. Earlier PE was 598.7 but after eps growth it is 65.1 and it’s median PE is 55.9.

So is it worth to buy at this point or it is expensive now.

Its 1 year return is phenomenal.

Please advice how to look this company at this valuation.

Waaree Concall + Q3 FY24 Result + New Order received

By 2027 solar would be about 206 gigawatt up from 70

gigawatt today.

Waaree Conversion of Bid vs Received is around 30-40%.

Current bid of 9 GW is in pipeline.

Present Order book (unexecuted) is 1.1 GW.

Past 9 month FY24 Rev/ MW is Rs. 0.784 Cr.

New Order of 0.41 GW Order is (Rs. 1.32 Cr)

Solar Analytics to capture the data on the generation capacity during various periods of time based on illumination, and to find efficiencies or inefficiencies.

Waaree executes EPC contracts with buying Land and setting up Solar plants for clients (Rs. 3.5 Cr per MW) and also just putting up Solar Plant on clients Land (Rs. 1.3 CR/ MW- Rs. 2.5 Cr/ MW).

Taking Orders from Pvt Sector is their Focus area.

Some illustration on If

================================

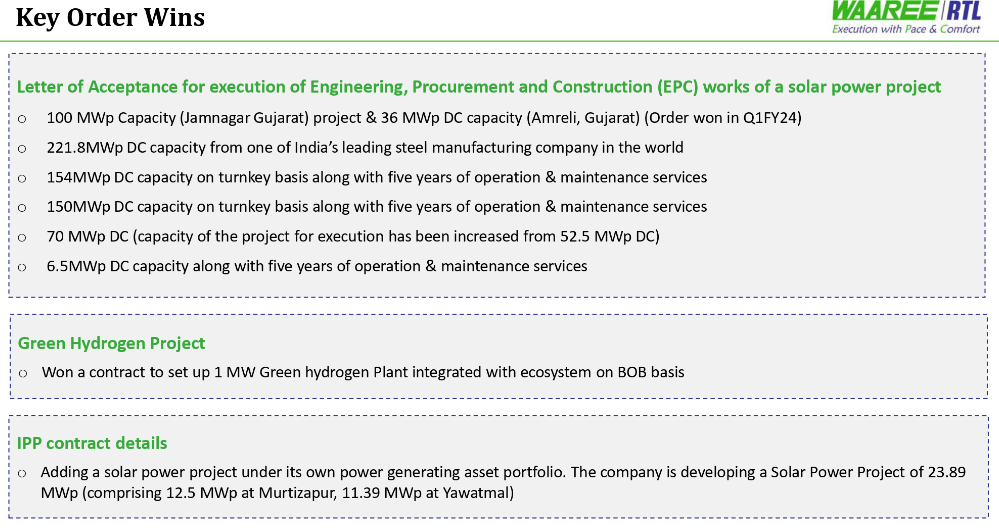

Waaree RTL received a “letter of award (LOA) for the execution of engineering, procurement and construction (EPC) work for solar power plant of 980 MWp on turnkey basis”, it said, adding the company’s unexecuted order book now stands at 2.141 GW.

The project is scheduled to be completed within 12 months as per the LOA

It does not have any moat…solar EPC is not very high end in terms of engineering, very low margin business. Dont know what the Energies businesses are but if its solar module manufacturing that too will not have any moat.

My suggestion will be to avoid the group. They are trading at very high valuations which will not be sustainable.

Don’t think so. The reason for such high valuation can be attributed to; a) sector tailwinds in renewables, b) topline growth due to point a ; and c) guidance provided by management for Q4. Management expect that for full year they will deliver approx 900 to 950 MW and in first 3 quarters they have delivered 473MW.

As per the yearly numbers reported here - Year wise Achievements | Ministry of New and Renewable Energy | India, India seems to have added 10GW per year in 2022 and ~7GW in 2023, the estimates of 10GW and above per year looks aggressive to me. It doesn’t account for slowdowns where we might see a dip in new commissions. I would like to understand what changes for the company for every 100MW increase in the order book, does their working capital cycle increase, does the debt profile change significantly. Understanding these may help us arrive at a sustainable growth rate. Let me know if that makes sense.