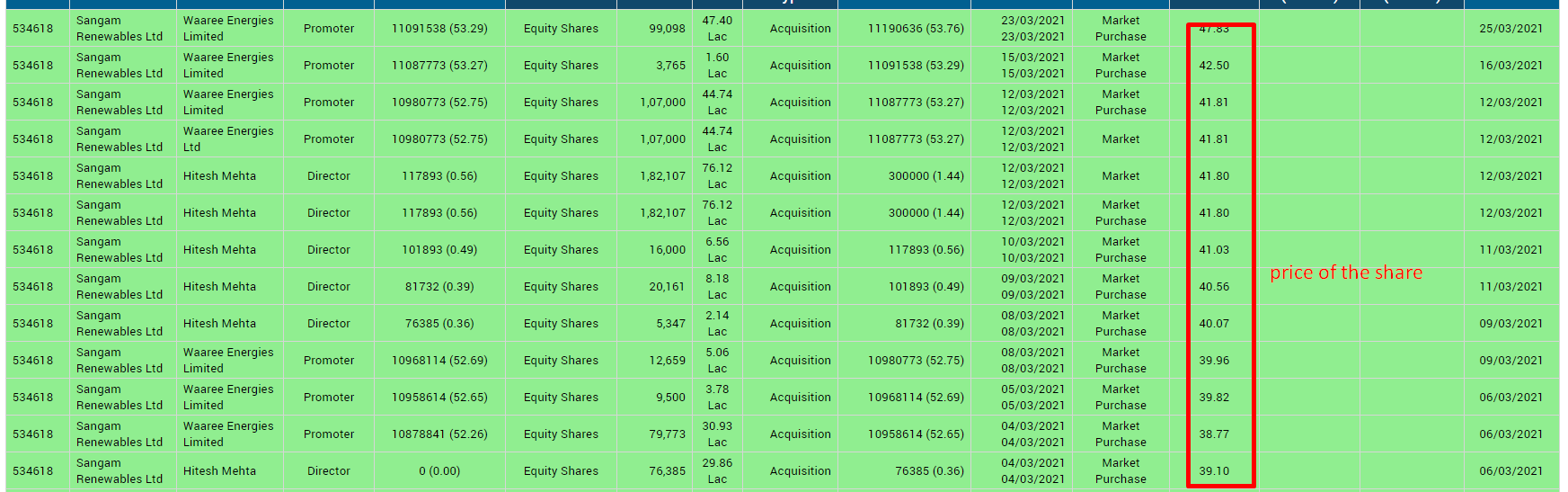

Promoter raising money and selling shares in listed company…do they augur well for reverse merger???

I think they will require 800 crores as Waaree energies is highly leveraged.(Earlier newspaper reports also suggest). Out of which they have managed to get 200 crores via debt .

Promoter selling might be due to both companies getting merged as sangam has already taken approval to raise authorised share capital to 70 crores .

Waaree has 7.22 crores shares issued and promoters hold 99%holding . So any which way if both companies merge they should be having decent Promoters holding .

Interesting thing is who are the buyers as this company is not widely tracked and absorbing 8 lacs shares is not easy for share with average vols traded in few thousand shares .

Promoters selling suggest that the dilution would be more ( vs initially expected ) and probability for merger increases further as Waaree is 99% owned by promoters .

http://www.bseindia.com/xml-data/corpfiling/AttachLive/e2b16c1d-8095-4ac3-a832-f09641522bee.pdf

Board to consider raising funds via issuing equity on 30/01/2018.

1 Like

http://www.bseindia.com/xml-data/corpfiling/AttachLive/f5a96a1c-a128-40e7-bdd3-3a02dd463d53.pdf

Right issues for 240 crore, I dont think any minority shareholder is going to subscribe the issue considering the fact that there is no business as such carried out by the company. Any idea what can be the purpose of this issue since the order in hand also do not require more than 100 crore of equity plus reverse merger seems to be a distant dream now.

What now? No rights issue. SPV to be launched. What would be the impact of latest ann.

Finally at the most oppressed price of 18.5, Pref Allotment and Open Offer has ensued.

The turnover of Waaree Energies Ltd. for March 18 was 1277 cr as per ROC data with 25cr PAT

1 Like

Change of name to Waaree Renewable Technologies Limited from Sangam renewables

.

Appointment of Heema Shah as company secretory ( Also company secretory of Waaree energies ltd )

.

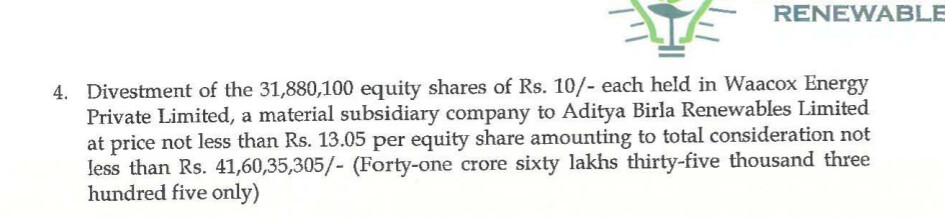

As per last year aggrement selling the majority 51% stake at 46 Crore its’ subsidory waacox energy pvt ltd.

to aditya birla renewables

.

recently Waacox has provisioned 16MW solar power

.

q4 2021 announced

yea, looks like its going the patanjali- ruchi soya way , makes sense to file drhp for capital raising and then later file addendum.

Waaree Renewable Technologies (Quick analysis)

(Prepared incorporating the Q4FY23 concall discussions)

Key Investment Thesis and Outlook

- Huge megatrends - with support from govt

- Successfully installed 10000+ solar projects, with a total operating capacity of 600+ MW.

- Strong pickup in financials, since Mar 2022. Quarterly OPMs vary significantly from 10% to 48%; Future OPMs will range from 15% to 25%

- Cumulative orders done till date is only 600 + MW. In FY23, executed orders of 300 MW

- Have unexecuted orders of 870 MW, which are to be executed over 15 months (70% of these projects are excluding modules); They are bidding for projects of 3 GW and expect a 35-40% bid conversion. Hence, potential order intake is very high.

- 70% of orders are excluding modules (lower margins relative to projects with modules) - Cost is Rs 1.5 cr/MW. 30% of orders are including module in the contract (Cost is Rs 3.5/4 cr per MW)

- Govt has allowed delaying the adoption of ALMM on solar modules/cells (approved list of models and manufacturers) for 1 year. This is expected to benefit Waaree RenewableTechnologies

- FY24: Indicative revenue estimates by analysts suggests Rs 1000 cr revenue (from Rs 350 cr in FY23) with OPM ranging between 15-25% . Assuming worst case scenario of net profit margins of 10% ie Rs 100 cr profit ie nearly double FY23 profits.

10 Likes

just a correction Unexecuted orders worth are 817 crores.

2 Likes

Hi Gaurav / VP Folks:

1- Did you get the real intent of reverse merger to become public in FY17?

- No external fund rasing happened after this event.

- Parent company could have executed the EPC business on it’s own.

2- Why OPM fluctuates so widely (15% to 24%, considering only the real business of the last 2 years)?

--------------------Notes on shareholding and company information changes from the ARs ----------

-

2015: Corporate information Sangam Advisors Limited Is engaged in business of financial consultancy, & dealing in shares & securities. The Company is a Listed Public Limited Company.

-

2017:

- CORPORATE INFORMATION Sangam Advisors Limited was incorporated on June 22, 1999 as Sangam Advisors Private Limited. It was converted into a public company on November 18, 2011. The Company is engaged in the business of providing diversified financial services with primary focus in assisting small and medium enterprises (SMEs)

- CHANGE OF MANAGEMENT/PROMOTERS Pursuant to Share Purchase Agreement dated April 18, 2016 with the existing promoters of the Company and subsequent open offer in accordance with Regulations 3(1) and 4 of the Securities And Exchange Board of India (Substantial Acquisition Of Shares And Takeovers) Regulations, 2011, as amended from time to time, Mr. Pankaj Doshi, Hitesh Doshi, Binita Doshi, Pujan Doshi, Kirit Doshi, Neepa Doshi, Rushabh Doshi and Bindiya Doshi (“Acquirers”) had taken over the control of the management of the Company by acquiring 44.44% equity of the Company. The entire process has been completed on and report dated July 28, 2016 as required under regulation 27(7) of SEBI SAST Regulations, 2011 has been filed with SEBI.

-

2018:

- CORPORATE INFORMATION: SANGAM RENEWABLESLIMITED (erstwhile known as SangamAdvisorsLimited)(“ theCompany”) wasincorporated on 22nd of June, 1999 as a private company limited by shares. It was converted into a public company on November 18, 2011. The Company is engaged in the business of generation of power through renewable energy sources and also providing consultancy service in this regard. It has its registered office in Mumbai and its energy generation site is located in state of Maharashtra.

- Promoter sold 6% shareholding in Open Market

-

2020: 71.52% shareholding | Waaree Energies Limited : 52.26 % - 99% Preferential Allotment, Rest Open offer

-

2022: Company Overview: Waaree Renewable Technologies Limited (“the Company”) is a Public Limited Company. The Company is engaged in the business of generation of power through renewable energy sources and also providing Engineering, procurement, and construction (EPC) services in this regard. It has its registered office in Mumbai and its energy generation site is located in state of Maharashtra.

4 Likes

External Funding did happened at the parent company level ( Waaree Energies) primarily via short term debt as the rates were low and later via Equity . There were very few listed comparable company in the renewable space during 2017-2018 except Adani which also was product of Demerger .

Getting directly listed - I presume constraint was valuation benchmark - Maybe the promoters had projection of the tremendous oppouurtunity in the sector but without signed contracts , getting proper valution would have been a challenge .

Secondly for small EPC company one big large order can change the fortunes of the company - which happened with this company .

Thirdly it was easier for parent company to raise equity capital as because valuation benchmark for the listed subsisdiary company was already there .

Lastly reason for taking epc buiness into seperate company was maybe getting debt funding from investors ( Initially main underlying business of the company was Manf of solar panels) Lending Institutions are wary of funding large epc contracts as risks associated with them are quite large .

Latest round of valuation had happened @ 13k crores for Parent company .

Disclosure : I still hold the stock so maybe my opinion maybe biased .

1 Like

Hi. thanks for referencing this thread. I wasnt aware one existed. Given that the captioned corporate development is old news now, I guess we can now change the name of the thread to the company’s name and discuss further.

Yes i am invested here for around a year, so views are (not “may be”) biased.

Company has started coming out with press releases, results presentations and also held 2 concals, most recent one being yesterday (28th) for its Q1-f24 results.

Being involved in solar epc, the company is likely to benefit significantly from industry tailwinds driven by government support to move to renewable energy.

But epc does not get counted as a high quality business, and often scale works to the contractor’s disadvantage.

Unless the company is able to maintain the same financial, business, and operational discipline that it would have maintained when it was smaller.

We have WR (waaree renewables) as a smaller co and we have Sterling Wilson as a company to learn from given its vintage - what are the risks, what can go wrong, how any company can get affected by its decisions, by sector dynamics etc.

While benefitting from industry tailwinds, WR would need to ensure they try not to commit mistakes that plagued SW (from which it seems to be turning around).

During both concalls, and in their press release / presentations comments, the WR management has referenced several times their focus on ensuring profitability, being prudent in selecting and executing orders, endeavoring to ensure control over debt and working capital and achieve positive cashflows. Investors would need to keep track of these as they grow.

Apart from solar epc, there are optionalities of green hydrogen, solar+wind hybrid projects, and (perhaps) pumped storage that the company is exploring / executing.

Operations and Maintenance of solar plants is another attractive line of business with high profitability, low investments and high returns on capital. Compared to epc, which is a bulk business, OnM income is relatively granular and will take time to build up. However the company seems to be focused on this.

Their 3rd line of business is IPP, where they set up solar plants, and operate them by supplying power to the grid. They indicated they might also sell the plant to other investors if the offer is attractive. They also have stated their intention to be prudent in this business as it takes up relatively higher capital than epc.

Coming to financials, being a relatively young operating company, their quarterly financials have been a bit over the place, especially in the profit margins department. While sales growth has been decent, margins have been fluctuating.

From the recent call we can draw inferences of how much revenues they are likely to generate. They have an order book of 850MW to be executed over 9-12 months (some delays may happen). 20-30% of this is with modules (as per their Q4-f23 concal) and can generate Rs. 3.5-4cr per MW and the rest is without supply of modules which can generate Rs. 1.2-1.5cr per MW. They guided for 12-15% ebidta margins (after having indicated the range to be 15-25% in the Q4-f23 call). This I think (my assumption) refers to the epc business. The OnM can possibly contribute an additional 1-2% on overall basis. Currently there is little/no debt. We can assume depreciation, and tax and come to a PAT number (my guess is pat margins would range between 5-6% to 8-9%).

We also need to track order wins. Given the govt relaxation on ALMM rules and the decrease in module prices, epc contract enquiries and order awards/execution is likely to pick up pace. Which augurs well for WR.

These are my broad views. If there are any specific points , we can try to discuss them.

13 Likes

Any take on the resignation of CFO? He will continue as Executive Director though