Recently BM created good wealth for his subscribers by first day first show via DMart@585 n Bandhan@ 480-90 as per grapevine.

1 Like

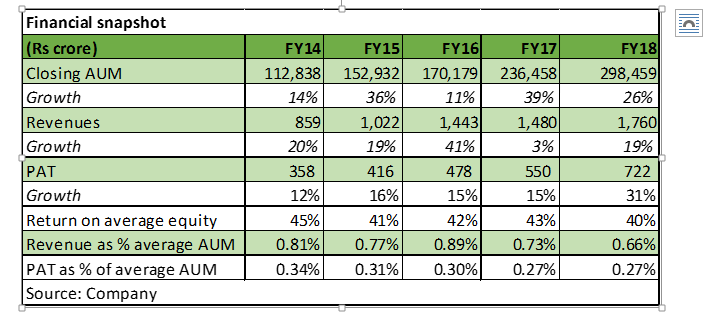

BM has stated in past interviews that he likes stocks that have a very high growth rate and opportunity. Some if his recent picks have been super high growth stocks like Dmart - 40% Growth, Bandhan and Bajaj Finance - 30% + growth.

If you see PAT of HDFC AMC has grown at > 20% in only one of the last 5 years. Plus HDFC AMC is far more cyclical stock than something like Dmart.

Only thing is for sure that predictability of earnings is very high because of HDFC name. It seems to me that market will continue to keep such businesses valued at a premium. Case in point being Gruh Finance.

5 Likes

Views invited on TCS and L&T technology services. Prospects seems good for both cos in view of depreciating rupee,good bounce in US economy,outsourcing gathering pace in continental europe,good demand due to increasing digitalising and advent of latest technologies like Cloud,AI,Blockchain etc,excellent management and good opp size against which mktcap is still attractive IMHO.

discl-invested

2 Likes

What i like about LTTS is its not a vanilla IT company. Its a pure play E&RD with a strong engineering DNA thanks to its parent L&T. They operate in some niche areas like Robotics, IoT, Smart Factories which are expected to grown more than traditional IT services in future. 5G, Real time monitoring medical devices, Autonomous cars are expected to provide huge opportunities and LTTS is in pole position here.

LTTS is a company which adds value to its customer (unlike traditional IT companies which are struggling here) and its reflected by the 90% repeat business they get from their top 30 customers (its a risk as well). They have 50+ customers from the world’s top 100 R&D spenders and the list is growing.

Return rations like ROE and RoCE are at the higher end of the spectrum and their 5 year plan for doubling their FY21 revenue to $1 billion USD is on track.

6 Likes

Manorama Industries Ltd IPO — should we invest

dont track it. Too many ipos expected by sep 30 as DRHP validity is getting over. Be v selective in sme IPOs as approval is not done by SEBI .

1 Like

All the IT companies are operating in the “cutting edge” areas. I don’t see any reason to single out LTTS no matter what company is proclaiming.

Please do compare the success/ faliure of the entire industry before you take a call on investing in LTTS.

Disc: Not invested in any IT names

Do “All the IT companies” have any other choice but to change themselves as per the emerging industry landscape? Its not about operating in cutting edge areas. How many are able to capitalize based on their expertise in those areas is a question. If you are working in IT (I am at a senior position) you must be aware that even though companies know that they have to adopt to the new emerging landscape, its not easy to change/train their workforce. In fact, most of the current workforce is not up to the mark and not skilled enough to manage the upcoming realities of the market. Many are not even ready to CHANGE. LTTS scores here. They are E&RD company and R&D and innovation is what they do. Its a day to day business for them.

As i have mentioned in my original post they have around 30 of the top 50 R&D spenders as their customers for a reason.

And finally you can’t compare LTTS with a traditional IT company. They are different. If you want to compare then you compare L&T Infotech with other IT companies.

Regards,

Suhag

3 Likes

Hi Vivek , Any SME IPO you are applying recently ?

No Too many ipos expected by sep 30 as DRHP validity is getting over. Be v selective in sme IPOs as approval is not done by SEBI .

L&T Technology Services (LTTS) wins USD 40 million Engineering Content

Management (ECM) Deal in Europe.

Very few stocks are showing resilience in the falling market and LTTS is one of them.

Regards,

Suhag

Hi Vivek,

Can we have a separate thread on Focus Lighting ?

Few updates on Focus…from AGM.

- Partial Capex done for Ahmedabad plant… Plant will be operational in 2019.

- Revenue from manufacturing will grow 50%+…while overall revenue cagr will be 25/30%.

3.They are entering into retail with one or two stores… Depending on the success they will further plan for retail foray. - Exciting thing is they have added IKEA as their customer. They have now contract for one store.

Regards,

2 Likes

Any updated on SSINFRA ?

Ssinfra became one of few sme cos to declare the dividend albeit a small one of 30 paise. My bet remains on promoter who are competent architect n civil engg of repute having passed out from good colleges and having good experience as well. But they seem to be pure technocrats and financially not very savvy . Things shud improve going forward qith new financials team in place.

Sme stocks have been butchered tks to risks associated with some.small.cos n fin frauds whivj have happened in some of them like Ashapura Momai etc n all sme stocks have been impaceted

One needs to revisit one checklist and buy more or stay invested if the story has not changed . Ssinfra with an order.book of 130 Cr pe of around 4 to 5 Opm of 35% n Npm of 16% implying good hold in its niche business of defence enabong orders on nomination basis n good dividend yield which is expected to.improve in future along with earnings shud entail more digging. Here Hyderabad based VPers can help similar to.the scuttelbutt done in Sheetal.Cool.which created good wealth . Pl help

Risks remain small.size of co n promoter now in 50s n they being financially not v savvy n poor travk record of LM Pantomath

Discl invested sine ipo

Sorry missed your earlier message. Everything moves in cycles. I had entered in HFCs like GICHF ,PNB HF, Mosl HFc arm but exited at good profits.

Feel excessive bearishness happened on these HFCs and quality will again prevail

1 Like

Superb reading of IRB Invit. I applied but luckily converted the same into Bh Rasayan at a small loss in June 17 @3000 odd. Converting once laggards into outperformers within your portfolio always helps.

what else do u have in your PF? any recent buys n sells?

1 Like

Kenneth Andarde complely avoids Consumption and FInance stocks…reason cited very high valuations causing bubble…do you agree?

1 Like

You can refer the thread on this company…I was also suggested this name by @dumboinvestor

Bought some Gruh averaging on upside post Bandhan results as its cheaper by 9 to 10% via this route.

Credit access cud be another intersting bet on MFI sector . Good mnc mgmt low Npa n good sourcing of liabilities

6 Likes