i think the rise is due to sector tailwind. Most of the chemical stocks have gone up in last few months.

I guess the MF particularly HDFC MF is buying heavily. They seem to have revised price target from 600 odd to more than 700 recently.

Soumen,

Any idea where one can verify this development or do I have to wait for the next Shareholding report.

I have tried to read the Balance sheet.

First the net sales is down , however the profitability is still up. The main reason for this was a decline in the price of the raw material, (refer to the profit and loss statement. )

The company is constantly buying fixed assets , however the good sign is that it is funding it completely with the cash from operations.

The creditor days is around 12-15 says, however the receivable days are around 60 . So it is clear that the company is giving good credit to its buyers , however not getting the same benefit from its suppliers.

3 Likes

My guess is based on recent two interviews of HDFC MF on news channel. Dipen Seth talked in a very bullish tone about it. His target was around Rs. 630. Parag Thakkar of same MF talked about it in a bullish tone and his target was in excess of Rs. 700.

Vinati reported its 2Q results…overall flat results QoQ…

Important points to note:

- Company has become debt free (Long term borrowings is zero now)

- It has mentioned about the plans to make investments to manufacture IBAP and P-Amino Phenol at Mahad and Butyl Phenols at Lote facility

- Capital WIP has further increased showing capex is on track

Disclosure: Invested

3 Likes

Vinati Saraf came on ET Now for interview today morning. Provided further clarifications about new capex plans.

-

Mahad plant will have capex of 500 Crores and Lote facility will have 150-200 Crores capex

-

Butyl Phenols products are currently imported; Vinati will be first to produce them in India (as per interview these are landmark products); They are getting external technical expertise to make it

-

Capex will be done by FY19

-

She did not mention the source of funding…she also gave revenue guidance from above as 600 Cr and 350 Cr respectively (did not mention if it were annual…but I think it should be annual guidance)

Disclosure: Invested; Please note that these notes might not be 100% accurate but will post the video as soon as I find the link online

My view: This provides comfort that management is working on diversification of product portfolio and this further provides growth visibility for next few years

4 Likes

Haven’t been tracking this business for the last 3+ years.

We did like the Management and their ability to carve out a global niche for themselves - the strong balance sheet, and improving profitability

I did not like a few things like

a) You are completely dependent on Mgmt Commentary about the prospects/visibility on the main product segments like ATBS, etc. It was extremely tough to get any independent corroboration of market, applications, competition updates and the like

b) Inherently a cyclical business - volumes are linked to petro-cycles

(no idea now, guess current product segments would exhibit similar characteristics; its quite possible they might have bolstered existing niche/found better ones)

Decided to pass up on this, given that with other things being equal (BS strength, profitability/returns) we had better visibility into businesses that were growing faster, and easier to track. (Increase Visibility, reduce Hope).

8 Likes

The PAP market seems to be saturated.

The global para-aminophenol (PAP) and paracetamol market has been growing due to the increasing cases of chronic diseases and conditions that need pain management solutions on a regular basis. About 80% of PAP produced worldwide is used for making paracetamol. Thus, the increasing consumption of the latter is directly impacting the growth of PAP market. Additionally, the growing awareness about the pain management solutions offered by paracetamol, which is essentially an effective analgesic, is a key factor boosting paracetamol consumption across the globe. The application of PAP (para-aminophenol) in several other areas such as for making dyes, rubber antioxidants, photo-developing agents, anti-ager, and other chemicals is also propelling the global market.

Transparency Market Research predicts that the opportunity in the global paracetamol market is expected to be worth US$1,049.7 mn by 2022 as against to US$900.2 mn in 2014. Meanwhile, the para-aminophenol (PAP) market, will reach US$709.2 mn by 2022 from US$452.7 mn in 2014. The emergence of India and China as leading chemical producers have also presented a score of opportunities to the overall market as PAP is expected to find increasing application in industries such as agro-chemicals, pharmaceuticals, and dyes amongst others. Players are also expected to tap into supportive infrastructural setup offered by emerging economies of Asia Pacific to increase and diversify their manufacturing capabilities.

North America to Account for 40% of Global Market by Volume by 2022

North America leads the global market, poised to account for 40% of the total market share in terms of volume by 2022. The region’s standing will be the result of a growing number of PAP manufacturers and a strong presence of state-of-art manufacturing units. The persistent efforts made to upgrade from chemical production to specialty chemical production in the region have also boosted the market in the recent past. Additionally, attempts to adhere to environmental regulations pertaining to manufacturing processes are also propelling the PAP market in North America.

Asia Pacific Market Flourishes with Advantage of Reduced Manufacturing Costs

TMR estimates that the Asia Pacific PAP market will exhibit a steady CAGR of 3.9% between 2014 and 2022, while the paracetamol market will rise at a CAGR of 1.9% during the same forecast period. Asia Pacific is expected to present abundant opportunities to the PAP and paracetamol market due to low labor costs, affordable research and development costs, a larger base of manpower, supportive infrastructure, and increasing trade volume due to an exponentially rising consumer base. These are the common denominators driving the consumption and production of PAP and paracetamol in emerging economies of China and India.

An influx of investments in chemicals and pharmaceuticals industry has built the perfect framework for the consumption of PAP in various agro-chemicals and dyes along with a range of pharmaceutical compositions. All of these aspects have resulted in reduced costs of final products in comparison to products manufactured in North America and other European regions. Thus, consumers are preferring Asian products over others, while manufacturers are shifting bases to indulge in cost-benefits offered by countries in Asia Pacific. Citing these reasons, analysts predict that Asia Pacific will emerge as a significant regional segment during the forecast period.

Some of the leading players operating in the global PAP and paracetamol market are Mallinckrodt plc, Granules India, Angene International Limited, Haihang Industry Co., Ltd., Jinan Haohua Industry Co., Ltd., Parchem Fine & Specialty Chemicals, and Kemcolour International. Companies will strengthen their distribution channels to reach out to a wider audience to maintain their leadership in the overall market.

6 Likes

Ambit has published a detailed report on Vinati Organics. Will share the link if available in public domain.

Vinati Saraf interview telecast on CNBC today:

Here is the initiating coverage report on Vinati Organics by Ambit released today:

Disclosure: Invested

5 Likes

The report is good. New products being developed and capacities being built to manufacture these are the primary reasons to invest in this company. Vinati has 2/3 well developed products with very high market share that will provide required free cash for these future initiatives over the next 2-5 years.

Strategy of the company is to develop a product with well established market by collaborating with a leading research laboratory in India or abroad and manufacturing it at the lowest cost. It has worked 3 times in the past and it likely to work in the future as well as long as Mr. Saraf is actively involved in development of the product/process. He was the key driver behind the past successes. However, he is pushing 66 and is unlikely to continue to work for a long. Ms Vinati is handling everything except the core R&D and is doing that well. But her job is relatively simple as low cost commodity product is easy to sell as there are just a few bulk buyers of these products which does not require much marketing/distribution efforts.

At current valuation, next wave of growth is already priced in.

Disc: Invested.

3 Likes

First things first Thank you @vivek_mashrani ji for sharing the AMBIT report with the community.

I am attaching an excel file which contains a few notes I have made from different sources freely available online. I hope these notes will be helpful to anyone researching the company.

Going through the excel, you will find the first sheet contains the past two years export data on ATBS & Na-ATBS. I have calculated the average realizations of two years and average yearly realizations also. Volume and total value data is also available. However, the total value figure will not match the segmented sales data for ATBS provided in annual reports as the export data is missing a few months of data which is not available online currently.

The second, third, and fourth sheet contains the past 2 year import data on Butylated Phenols, a market that Vinati Organics is targeting in the coming years. The data is in the same format as the first export data sheet and I have calculated the average yearly realizations and total volumes imported. The import data contains all four types of Butylated Phenols targeted by Vinati Organics namely, Para Tertiary BP (PTBP), Ortho Tertiary BP (OTBP), 2,4 Di Tertiary BP (2.4 DTBP), 2,6 Di Tertiary BP (2,6 DTBP). The domestic market for Butylated Phenols seems to be around 15000 TPA and valued at 150 cr annually.

Vinati Organics is setting up a 39000 TPA capacity of BPs by FY19, currently India imports 20500 TPA of BPs which is a 300 cr market as per Ambit. The import data is from Zauba, the mismatch between Ambit and my estimates maybe due to some chemicals imports missing in the data and also due to some by products of the BP manufacturing process that I have not considered yet.

The fifth sheet contains the past two year import data on Para Amino Phenol (PAP). Again the format and calculations are similar to previous sheets. The import data shows that the domestic PAP market is around 22000+ TPA and valued at 300+ cr. This seems to be in line with the figures that Ambit has provided in their report. However, this is only half the story for PAP as the other half of the market is in exports for which Ambit has provided some estimates. I am unable to confirm the global market size for PAP from my current research but I will keep looking and will share when I find something. If anyone else has experience in assessing this global data from direct sources not reports your help will be appreciated.

Caveat: All the market figures given above are based on import prices and Zauba does not mention whether these import prices are inclusive or exclusive of customs import duties which in case of these chemicals is 25.85%. A big portion of this custom duty is the 12% CVD which is Countervailing Duties. CVDs are charged on imports at the discretion of the destination country based on self assessments of the subsidies provided by the source country. CVDs are fair in the eyes of WTO provided some particular guidelines are followed by the destination country. I will be researching this further to check the legitimacy (according to WTO norms) of India’s CVDs on these chemicals and will post my findings soon. Both PAP and BPs are protected by CVDs.

On the sixth sheet are some calculations to check the economics of PAP. The assumptions are the usual logical figures. I take 20% cheaper unit realizations for Vinati’s PAP compared to current import prices. I have also done some calculations for the global market value excluding India. The assumption is Vinati Organics will gain 40% market share globally. The global market value figures are based on the assumptions of the Ambit report and have not been corroborated by me yet.

The seventh sheet contains my notes taken from the Ambit report shared by Vivek ji.

The last sheet contains my notes from a 2014 Environment Clearance report by Vinati Organics to MOEF. I found this interesting as the report details all their expansion plans which were completed in 2015. The report contains detailed ROIs for each individual project and their target markets. This document is very informative and should be read. I will be attaching the report at the end.

Based on the above line of thought I continued to search for more up to date Environmental Clearance permissions for its newer projects but I have not found anything yet. I will continue to search for similar permission reports as they are bound to come up sooner than later.

I have however, found the pre-feasibility report for their PAP and BP projects online but I am yet to read them. I am sharing them here for your benefit. When I make proper notes from them I will share them too.

IChemicals Import Export Data.xlsx (294.3 KB)

Approval for Expansion.pdf (1.1 MB)

22_Apr_2016_1300126804PGR1HW6VOLBriefSummary.pdf (466.7 KB)

22_Apr_2016_155939733UHIOJRKWVOLPFRfinal.pdf (1.5 MB)

26_Aug_2016_1314412405UHJ3O6KVOLLotePFR.pdf (1.5 MB)

Disclosure: Invested

13 Likes

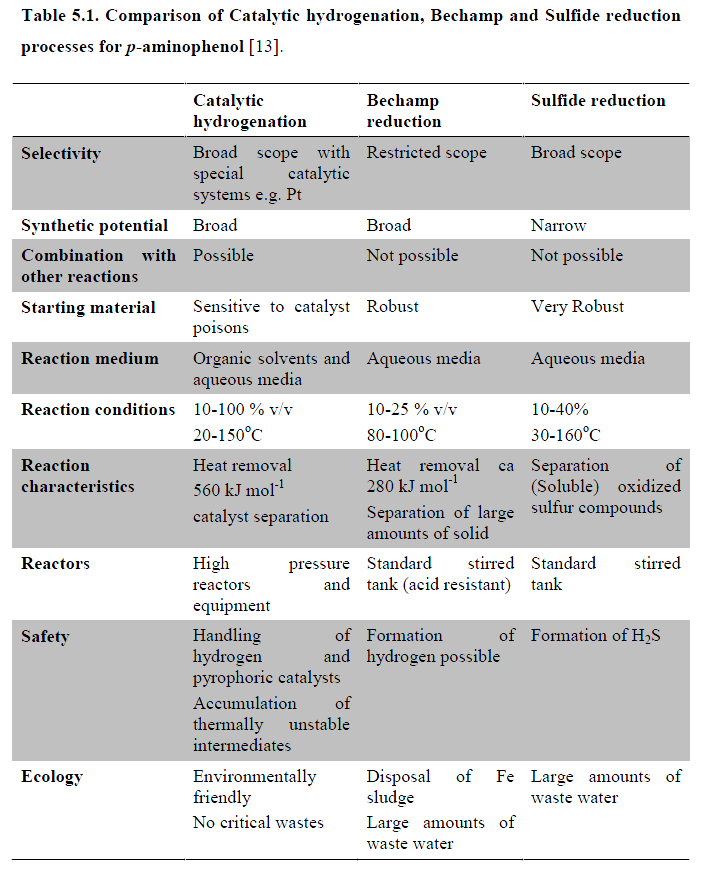

I forgot to share this with my previous post. I have some studies which explain the process of Catalytic Hydrogenation of PAP. The method was invented by a scientist in NCL, Pune named C. V. Rode, I found patents in his name for the same process dated 2000. It has taken Vinati a long time and trial and error to commercialize this technology.

As you will notice in the table below the CH of PAP has lower temperature requirements, is a single step process with lower wastes. This in comparison to the Bechamp process currently in use in China which results in toxic iron sludge. You can read the rest of the report below.

Catalytic Hydogenation PAP.doc (71.5 KB)

4 Likes

Thanks for sharing this.

The Zauba data is taken from shipping documents such as Bill of Lading and therefore does not include Import Duty or CVD.

A recent query by a fellow ValuePickr towards the timeline of PAP lead me to search for evidence of how the project is progressing. I think I have found something but do not know what it means. If anyone knows what this means please do share, for now I am only going to speculate to its meaning.

I found an entry for VOL’s application for the manufacture of PAP with DIPP in their daily list of IEMs filed.

Here is the link: http://dipp.nic.in/English/policy/iem09122016.htm

Now I can only speculate that this is an application for the license to manufacture PAP. Filing would mean that VOL is ready to commercialize PAP.

In the past VOL has applied for IEMs for various products:

http://dipp.nic.in/English/policy/iem02122011.htm - For DI IsoButylene

http://dipp.nic.in/English/policy/iem24022012.htm - For HP-MTBE

http://www.dipp.gov.in/English/policy/iem01042016.htm - For P-Tert Butyl Toluene

http://dipp.gov.in/English/policy/iem30082013.htm - For ATBS

Here is the link to a sample IEM form: http://dipp.nic.in/English/Investor/Forms/iem_Form.pdf

I am not 100% sure about this, I am hoping that someone with more knowledge of the DIPP IEM application will share their views here for the benefit of all.

3 Likes