I think the decision to stick or exit is purely personal decision. I generally sell only when there is new variable which I have not thought of initially or there is serious impairment in quality of earnings or any corporate governance issues with management.

In case of Vinati, yes, FDA ban of ibuprofen is a potential challenge for growth of IBB. But we need to understand that IBB is used in many other pharma products + perfume industry + as specialty solvent (Source: Annual report 2015; Pg. 17).

So we need to first analyze how much of total % of IBB produced is exported to US (and which is used specifically for ibuprofen) and see its overall impact on earnings and is this factored into price or not.

Also, there might be such challenges in terms of ban or environmental issues etc going forward as well since this is the nature of industry. But I think Vinati has been able to adapt to the requirements and diversified into new products, green production capabilities etc.

So the point is while selecting the company we should see its adaptability to changes since change is constant. For example, Infosys was writing codes in COBOL initially but with advent of Java and C++ it had evolved and now it is evolving in terms of areas like analytics, digital and social media.

Hope these little insights were useful. In my opinion we should constantly monitor results to see signs of any business impairment which I haven’t seen till now.

You are right but one has to also consider the capacity expansion as well in light of slowing demand…many times management increases capacity by extrapolating fast growth…ATBS was growing fast initially due to low global share which is now 45%…IB is used for captive demand as well as agrochemicals which are again both showing slowdown and yet the management has increased capacity…IBB has its inherent risks which we are all aware of…regarding the success of new products-your guess is as good as mine.

I like the management and their approach…I like the business model too…my only overhang is the valuation…given risks in the business I believe the stock is over valued and hence would wait for a good correction (if any) to enter

widout a single penny from past year export benefits…PBT for Q4 is similar to tht of previous year…this gives an indication tht ATBS volumes are increasing…IB volumes expected to pick up in line with growth in agro chemical demand…plus some of the capacity additions will come online…

even though robust volume growth expected in fy17, eps is expected to be more or less flat…because last 32cr of export benifits were sitting in the PBT…which will not be available this year…

Capex to cost 200 Cr. funded entirely through internal accruals

Above initiatives+growth in existing products is expected to contribute incremental sales in excess of 100 Cr. in FY17

Indian chemical industry expected to grow at 11-15% pa for next year

We are the only Indian manufacturer of ATBS; the largest producer of IB in India; the largest producer of IBB &ATBS in the world; and retain market leadership in all the 4 key products of our product profile.

ATBS Capacity 26,000 TPA;Exporting to more than 25 coutries

IBB Capacity 16,000 TPA; Largest producer in the world with market share >65%

AGM on 6 August 2016; 1Q results in 4th week of July 2016

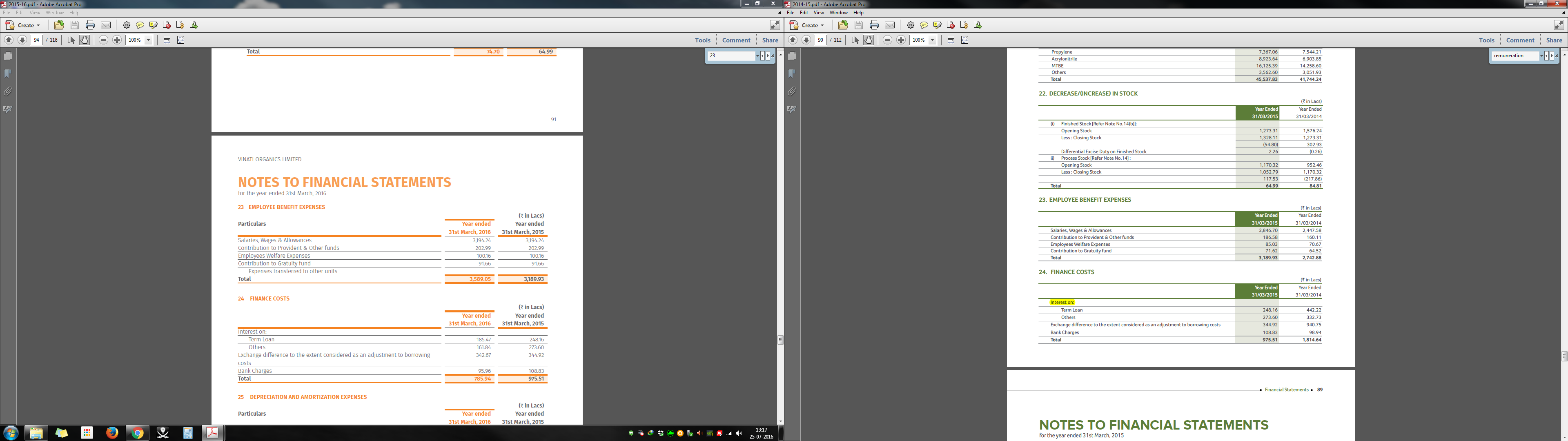

“Schedule 23 of the annual report for FY15-16 consisting of employee benefit expenses has the same figures for FY14-15 and FY15-16 for each of the four individual heads. For instance, the figure for ‘salaries, wages & allowances’ is the same for both the years at Rs3,194.24 lakh. However, the figures in the ‘total’ column for both the years are different. The auditors have certified these financial statements and these have been submitted to the Exchanges”

But for 15-16, individual break up has to be incorrect(which is the error pointed out by Moneylife). It might have been a printing mistake(although these have been submitted to exchanges). Moneylife is pointing at certificates by auditors here and ideally such errors or practices should be avoided by companies.

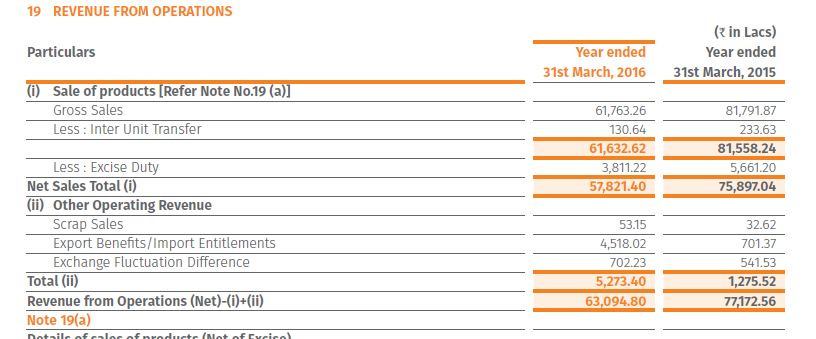

Company came out with its 1Q’16 results, overall very good result with decent revenue growth and good growth on PBT. Net profit growth slightly lower QoQ due to higher tax payments which typically is the case in first quarter.

The revenue from new products seems to be adding to the top-line and bottom-line.

This is general practice of many companies to inflate sales and earnings by other income like selling scrap, waste, capitalisation of waste land, etc. Surprise thing is that this will happen in bull run of stock market ( some time company sell scrap at higher price though real price in market down!)

Stock has moved up quite significantly in last few sessions without any further new. It is up almost 5% today as well with heavy volumes.

Based on knowledge of technical analysis, there may be something on the cards which is driving price-volume action. Ofcourse promoters had started buying, but I think they have almost bought more than 8 lakh shares (out of target 9 lakh shares), hence the price-volume action is more surprising now.

@vivek_mashrani L ooking at the industry PE of good performing companies, it seems the average is around 30 and at yesterdays closing price it was at around 21 pe.So at the current year EPS the price is undervalued. I guess that could be one reason of the stock price going up. Also the promoters are increasing their stake and hold close to 70% ,which is a big positive.