Looking at last 1 year chart, technically i feel the stock has bottomed out as of now and will rise from here on at least to 3500 or more till November 13, when the results are to be declared.

If the results are good it can rise further, or else one can book profit.

Disc : Took a small position for tracking around 3100 today.

Seniors please comment. This is just a trading idea…

@khushi Results are not Good - Topline is subdued , Net profit Margins have fallen if you compare half yearly and last year . Crude prices yesterday have taken a knock and therefore rubber prices will soften . However it will be more interesting to know if the firm can deliver on the topline growth which seems missing . Only commodity going up , down - markets wont give a higher multiple till they see growth.

Topline , in my book is not so subdued. Its a growth of 9 % which is preety descent. A 9% topline growth can easily incline the profits by 15%-20 % or so under normal circumstances( due operating leverage).

In q2, Its due to stock adjustment that the profits are lower than q2 last year. ( Stock adjustment of 25 cr vs 0.93 cr ).

@csteja

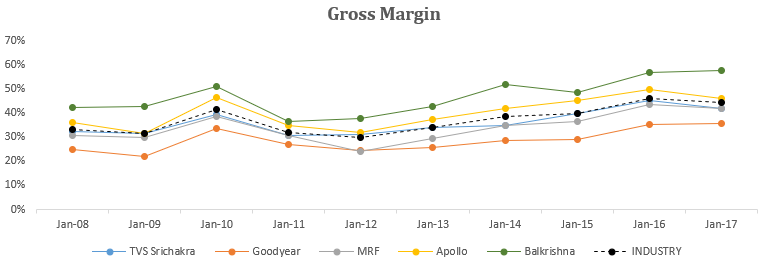

If you see below chart, the gross margin for whole industry has moved between 30% to 46% and also you can see the direction of movement for all companies are more or less same which highlights how much of margins can fluctuate due to raw material prices movement. Usually, it happens in those industry where there is high dependency of profitability on raw material price movement and sector companies do not hold much pricing power. This is typical with tyre companies. FY17 margins were life time highest as rubber prices were at 8 year low. However, nothing goes down forever and nothing goes up forever in commodities. So, one must ensure that in valuation calculation, the PAT margins one is considering is not a cyclic life time high or low margin but an averaged assumption of up and down cycle. In this thread somewhere i have also pasted long term rubber price trend.

So, when i say normalized margins, one must factor out sustainable long term gross margins and then come down to PAT margins and there could be other factors also contributing to better PAT margins like in TVS getting rid of debt has helped in improving bottomline margins apart from falling rubber prices.

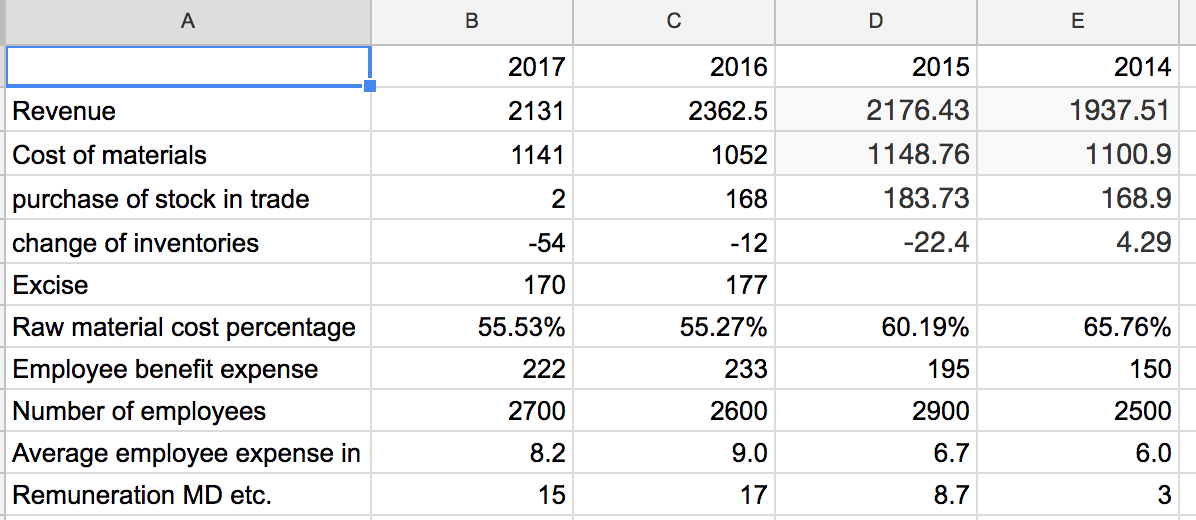

Totally agree. Just a slightly deeper look for TVS Srichakra pasted below; shows raw material cost as fraction of revenue dropped 10% in last couple of years; which should have resulted in a PBT increase of 200 Cr. It wasn’t there because employee costs went up significantly by about 80 Cr (not sure if these are one time payouts or not) including for management. Also there were some other expenses which includes promotions/discounts which might have been passing some of the benefit back to their customers I guess.

TVS Srichakra Ltd FY18 Annual Report Notes

The undertone of the management commentary in AR was positive on the back of expected double digit growth in Two-Wheeler segment. Management remained cautious of the competition in the Tyre industry as all the companies are earning good cash and there is expectation of Rs. 25000 cr investment in the sector in next 5 years. High growth in Two-Wheeler vehicles augers well for the company’s After Market segment in which TVS is the leader. Following are the notes from AR 2018.

Plant Location: Madurai (TN) and Rudrapur (Uttarakhand).

During the financial year under review your company registered net sales of ₹ 2218.03 Crores (including other income) as against ₹ 2140.65 crores during the previous financial year. Profit before Finance Cost and Depreciation stood at ₹ 267.16 crores as against ₹ 292.51 crores during the previous financial year. The net profit after tax for the current financial year stood at ₹ 117.61 crores compared to ₹ 155.33 crores during the previous financial year.

Company’s wholly owned subsidiary TVS Srichakra Investments Limited (TSIL) recorded a net loss of ₹ 26.82 lakhs (PY ₹ 576 lakhs).

During the year, ZF Electronics TVS (India) Pvt. Limited (ZFTVS), an associate Company, recorded a total revenue of ₹ 49.07 Crores (PY ₹ 46.43 Crores), ZFTVS made an EBITDA of ₹ 1.12 Crores (PY ₹ (0.35) Crores) and incured a net loss of ₹ 2.45 Crores (PY ₹ 3.82 Crores), mainly due to increase in cost of raw materials. Subsequently, ZFTVS has become a wholly owned subsidiary of TSIL with effect from 4th June, 2018 and the name was changed to TVS Sensing Solutions Private Limited (TSSPL) on 5th July, 2018.

Overall volume growth for the last year was 7% owing to increased pull in the OEM segment.

Company’s growth in the OEM segment was in line with the industry growth, thereby maintaining its market share and holding on to its leadership position.

GST had a negative impact on after market growth, your Company managed to maintain its market share. After Market (AM) segment faced significant pricing pressures and the Company had to churn out various new schemes/initiatives to remain competitive.

Expenditure on R&D of Rs. 29.59 cr at 1.33% of sales.

Advertisement & sales promotion exp of Rs. 43 cr ( 42.83 in FY17) at 1.99% of sales.

Total managerial remuneration of Rs. 14.31 cr (Rs. 16.31 cr in FY17).

Capex of Rs. 120 cr during the year.

The following certifications were obtained during the current year:

Madurai plant: ISO 14001:2004, IATF 16949:2016

UKD plant: ISO 9001:2008 & TS 16949.

As of 31st March 2018, there are more than 2,860 employees (both direct and indirect) on the rolls of your Company

Two-wheeler sales have been continuously & consistently growing in India leading to increased vehicle parc (i.e. number of vehicles on road). Consequently, there has been a sizeable increase in aftermarket opportunity which too augurs well. This provides a huge opportunity for your company to grow in this segment.

Government’s focus on electric vehicles offers yet another exciting opportunity to grow the segment.

Two-wheeler industry, which ended last year on a high note with a 16 per cent growth rate, is expected to grow not as fast as last year but at a respectable double-digit growth rate.

Raw Material scenario during FY18

While the first quarter of FY18 saw a softening of raw material prices due to subdued demand arising out of the transition from BS III to BS IV and GST, there was a turnaround soon after.

The raw material prices rose sharply since then, with a surge in demand resulting in increased consumption as well as global shortages of raw materials arising from Chinese manufacturers shutting down production due to environmental issues.

This period also saw an increase in the Oil Prices (Brent Crude) to $66/barrel in March ’18 from its low of around $47/barrel in June ’17. In addition, some structural changes in the duty structures of truck/bus radial tyre imports and import of nylon fabric also triggered these increases.

However, the only relief to the industry was the decline in natural rubber price during the year. The international rubber prices also softened due to a marginal drop in consumption and an increased global rubber output by about 6%.

To mitigate increasing raw material prices and availability, the Company took some actions such as long-term contracts with major suppliers, new and alternative sources. The Company also maintained additional inventories of certain raw materials that were in short supply for usage during crisis situations.

Tyre Industry trends in India

Last year(FY’18), domestic tyre industry grew at 7-8 per cent resulting in production of 18.05 crore tyres. This was despite the weak sales observed in the first and part of second quarter FY ’18 owing to Goods and Service Tax (GST) rollout. In tonnage terms, tyre volumes grew by 7 per cent during FY’18 on the back of Truck & Bus replacement demand which incidentally had seen sluggish growth in the preceding two years.

In FY’19, Unit and Tonnage growth are pegged at 8-8.5 per cent and 6.5-7 per cent respectively.

On exports front, while business grew by 10% in FY’18, it is expected to grow by 8-10 per cent over the next three years led by stable demand and increased acceptance of Indian tyres’ quality & price in overseas markets.

Capex infusion & related capacity addition is expected to continue for another five years given the favourable demand, strong accruals & large cash reserves. Fresh infusion of Rs.25000 crores is likely to happen during this period.

Improving road infrastructure across the country, increasing working women population and low penetration levels of two-wheelers in rural areas are still the main drivers.

TVS has emerged as the largest supplier to all established domestic automobile OEMs including Bajaj Auto Ltd , Hero MotoCorp Ltd, Honda Motorcycle & Scooter India Ltd, Suzuki Motorcycles India Ltd, TVS Motor Co. Ltd and Yamaha Motor.

3rd largest player in two wheeler after market segment in India.

Company also has a contract manufacturing agreement with French tyre major, Michelin, to make two-wheeler bias tyres under the Michelin brand, for the aftermarket.

TVS Srichakra will undertake capital expenditure (capex) of about Rs.150-200 crore annually, over the next three years, to augment capacity and enhance level of automation at its facilities.

Operating profitability moderated to about 12.5% in fiscal 2018, due to increase in prices of crude based raw materials (while rubber prices also remained high in first half of fiscal 2018) as well as reduced exposure to after market segment.

Prof Bakshi (vq moat fund) seems to have exited TVS Srichakra completely… as per latest BSE shareholding pattern of Q1FY2019… or am I missing something? any thoughts?

You are not missing anything. A big investor exiting a stock does not change anything about the company fundamentally. Unless Prof. Bakshi comes out specially with an explanation of why he exited the stock, there’s nothing to discuss.

Focus on your own conviction and stories, because Prof. Bakshi will be doing exactly that.

Prof Bakshi hinted about TVS Srichakra (He did not take the name of company but said ‘a tyre company in his portfolio’) in his recent talk at Moneylife seminar.

As per him, he overestimated the moat of the company, and if he would analyse this company again, he will not assign it his earlier valuations. One of the major concerns he flagged was inability of the company to hold on to OEM prices. He said," All the hard work of company management and employees is being enjoyed by it’s OEM customers due to weak pricing power of the company and hence he (Prof Bakshi), made a mistake in calculating the moat while buying the stock.

Bang On. @ashprit this was the explanation i was looking for on this forum. Will certainly help in re-analyzing/recaliberating original thesis. I had heard his class lecture about “Investing in Niches” .The stock has came off from the highs of 3700 to 2200 odd levels since then…still looks expensive though

Disclaimer: Tracking…

Correct. The lack of pricing power originates from this - see para 2 of this post:

Often, investors overrate the demand factor and underrate the supply factor in an industry. At least, that is one of the most important learning I have personally had in the last 3-4 years.

(Disc.: Exited a few weeks after the above post, no current exposure).

TVS Srichakra has historically been focused on the OE segment, with a limited presence in the after-market segment compared to the other publicly-traded Indian tire-makers. My understanding is that a significant part of TVS Srichakra’s margin compression over recent years has been driven by the company’s deliberate strategy of ceding margins to distributors in order to gain inroads in the after-market/ replacement segment. This seems to be working, at least to some extent, as seen from the recent acceleration in top-line growth.

Rubber price has been in the doldrums for a few years now. With many cultivators moving away from rubber cultivation, supply shortage is predicted from 2021 onwards. This may not bode well for the tyre companies going ahead

Michelin announces revolutionary new “airless” tyres, will go into production in 2024:

Why this is important for the tyre industry is that two-third of all tyre sales today come from after-market, which could be under threat if a technology breakthrough like this comes about.