Any idea why TVS Srichakra was high by 17% with such huge volume ?I am heavily interested in the stock and hence asking .While I dont intend to sale but need to know what has happened in 1 day that valuation up by almost 20% in a single day (there has been lot of buying)

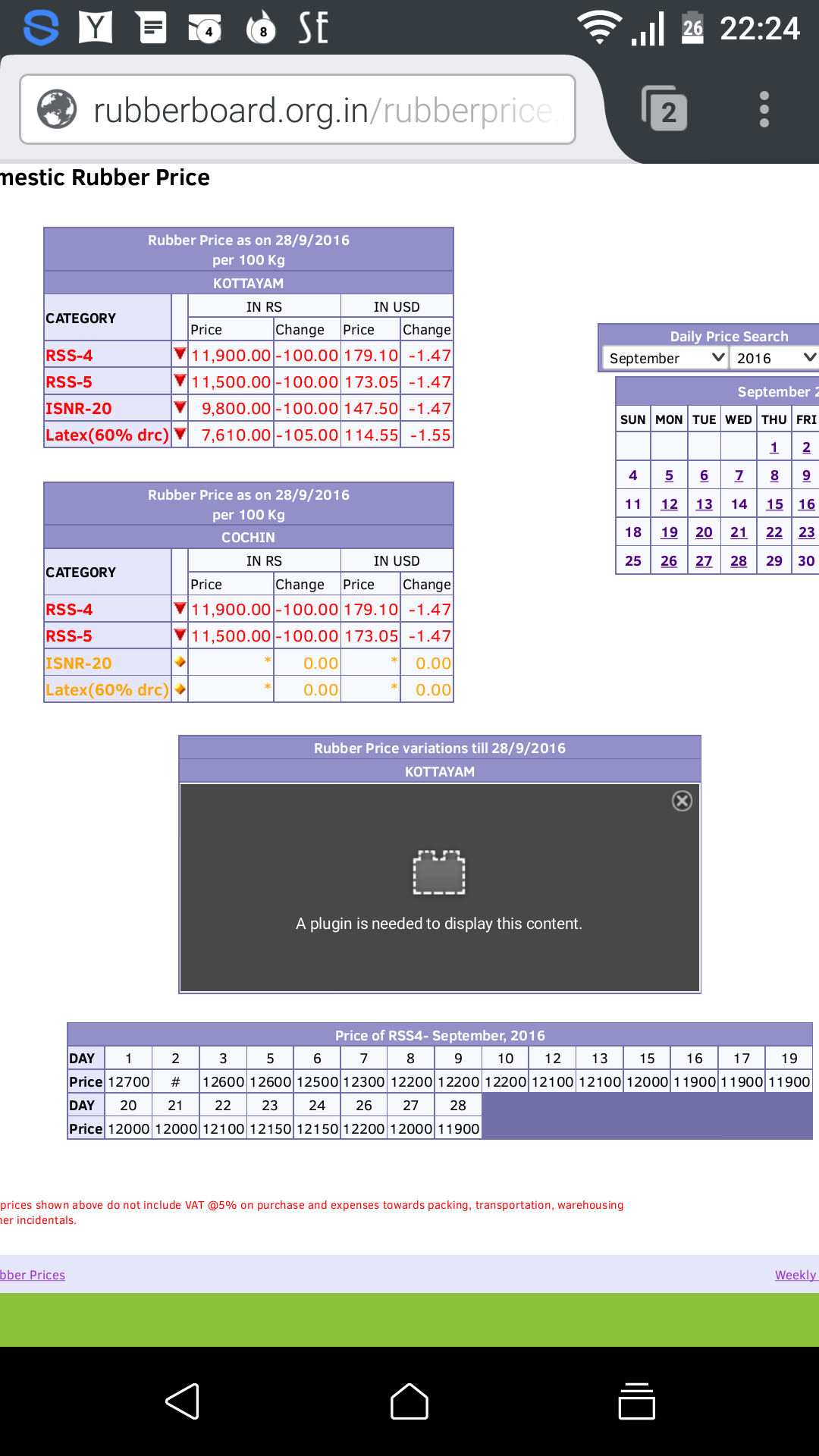

Looks like market is factoring in the fact that rubber prices went down from 12700 on September 1st to 11900 today…it would improve margins and profits of tyre companies…

Disclosure :invested

1 Like

There was very heavy volumes seen today. Would be interesting to see the bulk deals data tomorrow to see Who has bought in big

thanks for the detail update

Hi,

It seems that, Mr. Market has re-rated this stock from PE<10 to PE>15-16 in short span of 3 months.

My analysis suggests that, if I consider 12% EPS growth for next 3 years, then EPS would be around 357.2, since current TTM EPS stands at 254.24, and if we consider more realistic PE at that time (Say, 12), then price could be Rs. 4286. This makes me believe that, next 2-3 years price seems factored into current CMP which was close to Rs. 4200 few days back. I know that, this is simplistic analysis and I have not considered all factors here.

I am assuming that, rubber prices may not fall much and margins may not improve much hence assuming EPS growth which is moderate.

I am new to this forum and would like opinion of other investors whether in this analysis, have I missed any important trigger for further re-rating in this stock? Any views are welcome.

Thanks.

Disc: Invested at lower levels.

Fully agree. I also have done some calculation. Market is overestimating its earning potential

Is current market price makes stock undervalued? Is it right time to enter for long-term now (3 to 4 years)?

Current market price does not look attractive.

One good thing that TVS is doing is , they are very religiously clearing off debt.

Debt / equity is close to 0.2 down fom 2.1 [ 5 yrs back].

1 Like

Hi All,

I am trying to identify the reasons behind the decline in revenues and profits for the company in the current year, but I am not able to find any investor presentations or analyst reports regarding the same.

If anyone can please throw some light on the factors or share the relevant links then it will be really helpful.

Thanks very much

Some observations on the company:

Volumes were up 10% during the year (FY17) but Raw Material costs were down 6.34%. Despite selling 10% more tyres, revenues were down 10% and PBT was down 26% from Rs.284 crore in FY16 to Rs.211 crore in FY17. Realizations are under pressure, and the market is becoming fiercely competitive. Commission & discounts had already gone up 35% from Rs.100 crores in FY15 to Rs.135 crores in FY16 pointing to the same. The figure for FY17 is not disclosed in Annual Report but likely to be quite high.

There is a flurry of new players entering the 2/3 wheeler tyre market, and existing ones are increasing capacity. CEAT commissioned a greenfield facility at Nagpur. It will reach full capacity this year and more expansion is planned. Apollo Tyres launched two wheeler tyres last year and claims to have crossed 1 million units this year. It has announced a new plant costing Rs.500 crores in Andhra Pradesh dedicated to 2/3 wheeler tyres. JK Tyres acquired a loss making plant from the Birlas and claim to have turned it around this year. The plant produces 10 million tyres per annum. Others like Balkrishna and Bridgestone have also announced their entry in the 2/3 wheeler tyre segment recently. There seems to be a supply glut and so pricing pressure is likely to continue.

To its credit, at TVS Srichakra a lot of capex has gone on stream last couple of years. Around Rs.160 crore is reported to have gone into enhancing capacity by 200,000 tyres per month. Financial details of the Michelin tie-up are not known, but must have cost close to Rs.200 crores for a reportedly 3.6 million tyres per annum facility. Hopefully, this should drive volume growth, though how much of that will flow to the bottom line is anybody’s guess. Margins on the Michelin arrangement are not known. Advertising & Promotions have also increased in recent times, from around Rs.10-15 crore per year few years back to Rs.40-50 crore per year in the last two years. We have seen high profile ad campaigns on TV and Sports sponsorships.

Meanwhile, Long Term Debt on books continues to be more than Rs.100 crore and total indebtedness has increased, largely due to bank borrowings of more than Rs.250 crores to fund inventories. DSO has increased from 27 days to 35 and inventories have doubled. But amidst all this, company invested Rs.40 crore in Preference Shares of a group company last year and continues to hold the same. It also carries “investment property” worth Rs.25 crore on the Balance Sheet. Promoter drawing high salary & commission is another thing I don’t like. Overall, the Annual Report reveals very little and is quite a disappointment.

CRISIL estimates 7-9% growth in the OEM segment and 9% growth in the after-market segment for 2/3 wheeler tyres. ICRA estimates 6-8% CAGR for the two wheeler tyre industry upto 2019. But supply seems rising faster, so tough times will likely continue. The only saving grace is that rubber prices are expected to be benign, though here too competition will eat into any margin gains.

If anybody is attending the AGM later this month, please post your report.

(Note: Invested. Data collated from various sources in public domain & in some cases my own calculations. Do your own research before investing)

4 Likes

Hi,

I didn’t see TVS Sri conference calls to discuss quarterly earnings or any presentations shared with the investor community.

Can someone please confirm if TVS Sri conducts quarterly earnings conf calls?

Thanks.

No. They do not conduct any concalls as such. Thanks.

Can anybody help with understanding why stock going down?

“In the short term the market is a voting machine. In the long run it is a weighing machine.” There is usually no way to “understand” why price is moving in a particular direction in the short term unless you want to kid yourself. IMO better to focus on business prospects, management quality, strength of balance sheet and current valuations rather than price movements.

4 Likes

Thank you . I tried to get some answers myself. I have not seen any specific reason related to TVS Sri.other than many players are setting up huge capacity and China dumping.

RM - rubber prices are up, margins r down, profit is down, hence stock is going down

Hi Ram,

I don’t track TVS Srichakra, however I have been actively tracking CEAT and MRF for the last one year. So I have slight knowledge about the sector.

The recent not so exciting movement pattern among the stocks in the tyre sector is largely due to the negative sentiments in the market due to steadily rising prices of crude oil and natural rubber in the international market, since tyre is a raw material is a very raw material intensive product.

Even though recently anti dumping duty was imposed on tyre (bus and truck radials) imports from China, but the event was factored into the price ever since the speculation broke out a month ago the actual event, so the market did not witness any massive surge when the event actually happened. As they say you know ‘Buy the rumor and sell the news’.

Also there has been the effect of GST and the corresponding destocking which is likely to continue have it’s effect for the next couple of quarters.

So all of these are inhibiting the bull to run of late in these stocks.

2 Likes

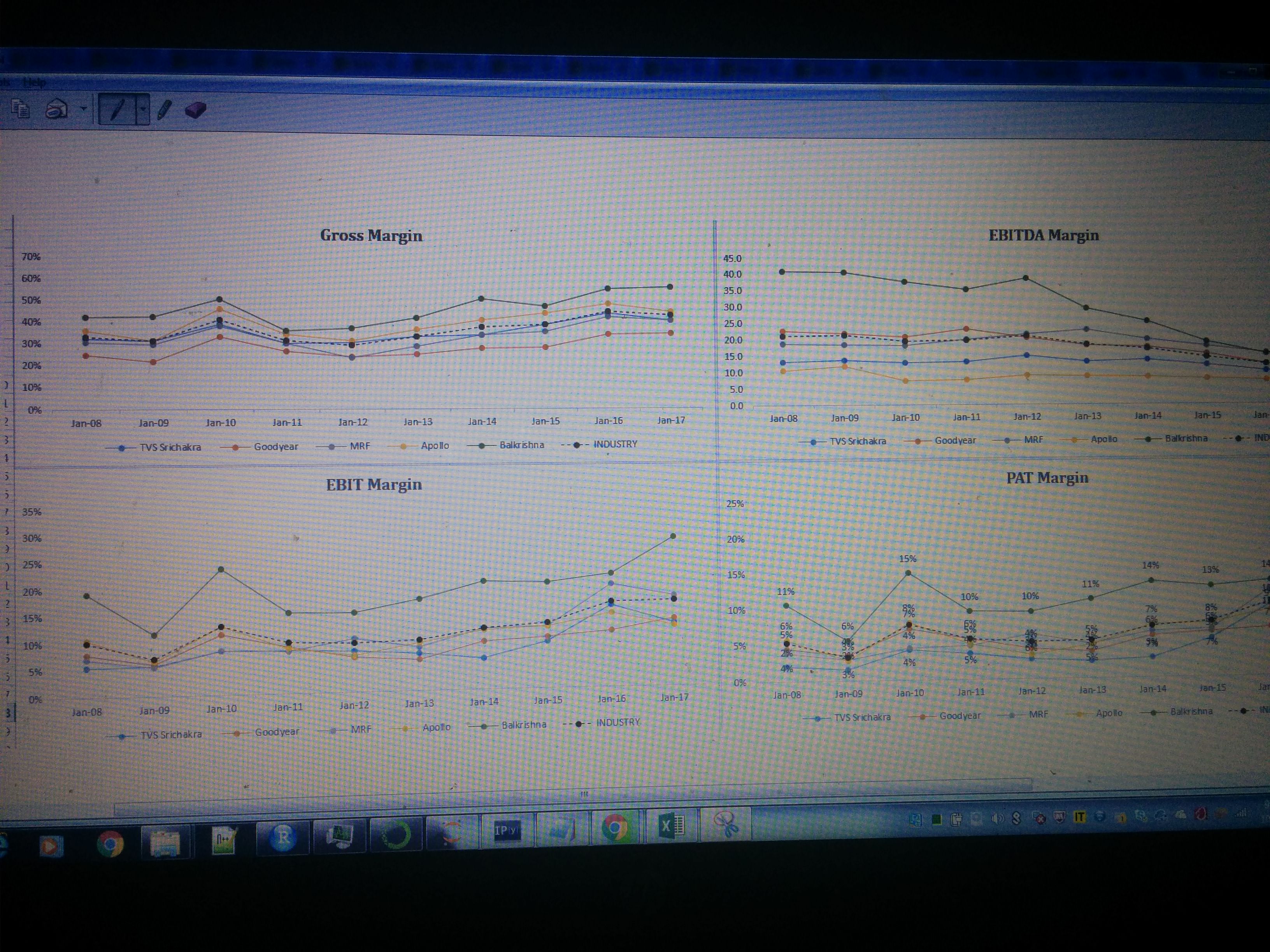

Historically , tyre industry has been a cyclic industry due to 1. Rubber price as raw material fluctuation 2. Insbility to pass price increase to end consumer. If you study 2008-2017 margin n correlate with Rubber prices you will see, margins are almost double (varies company to company ) at bottom of rubber prices . So, anyone buying must factor normalized margins rather than considering current margins in any kind of valuation estimate calculation. These are reasons why studying historical performance is equally important though share prices is all about future because history sometimes gives a view of future unless this time it’s different due to unique non cyclic phenomenons

5 Likes

To highlight the same I am providing below a simple profitability margin chart for last 8-9 years for 5 companies

2 Likes

Hi Andre,

Thank you very much for providing information.