Financial results for FY 2017-18:

Corporate Presentation:

Financial results for FY 2017-18:

Corporate Presentation:

I am holding Trident for past 3 years. Company has following going for it:

Reduction in high cost debt reducing interest cost

access to high quality cotton closer to factory, an edge over competitors, particularly foreign

Proven track record in towels

Deloitte is the auditor (hopefully books are not cooked)

Over last few months all textile stocks seem to have corrected including Trident. Its difficult to understand the reason for correction. Cotton prices may be one of the issue though it will affect all the players globally (India being one of the largest cotton producer) so company should be able to pass on the raw material price increase.

company has not been able to ramp up bed sheet capacity to the extent possible which may be biggest overhang. Though personally I do not see it as a major challenge as company has proven capability on towels and bed sheets is a related sector with similar customers.

Other may be trade war leading to reduced access to US market, which can have big impact as company is large exporter though its a business challenge and all Indian exporters will get time to adjust.

It will be good to understand other views on challenges faced by company and future prospects.

Disclosure - I am invested in company and considering adding at current levels.

Production figures for July 2018:

Division Unit of Measurement Quantity

Home Textiles Division

• Bath Linen Metric Tons 3,606

• Bed Linen Million Metres 2.17

• Yarn Metric Tons 9,519

Paper & Chemicals Division

• Paper Metric Tons 13,015

• Chemicals Metric Tons 8,199

It will great help if anyone tracking this company explain - How company doubled it’s profit this quarter 108 crore compared to 51 crore same quarter last year?

Thanx

Better utilization of textile capacities

reduced debt

better USD / INR realizations

continued tailwinds in the paper sector

cotton inventory at old prices

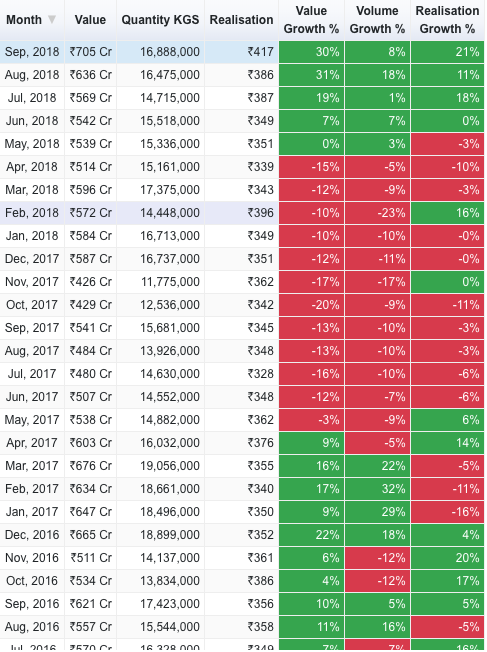

Terry Towels have shown impressive growth in Q2 https://phreakonomics.in/export-import/micro-individual?type=exports&hscode_commodity=5167&startDate=2000-04-01&endDate=2018-12-01¤cy=inr&consolidation=month

There seem to be some tailwind with the realisations as well with 8% increase even in USD terms in Q2. The rupee aided this and made it 17%. I think this is the reason for the good performance in Q2

CARE reaffirmed the Credit Rating of Trident Limited:

Facilities Amount Rating (INR Cr.)

Long term Bank 1,564.63 CARE AA-; Stable

Long term /Short 1,500.00 CAREAA-; Stable I CAREA1+

term Bank Facilities

Short term Bank 200.00 CARE A1+

Total Facilities 3,264.63

Good Q3 results-

Revenue up by 18%,

EBIDTA up by 21.3% (EBIDTA Margin-19%),

PAT up by 53.4%, (PAT margin- 9%),

Textile rev grown by 18.6% ,

Paper & chm rev grown by 15.6%,

(Textile contribution in rev 80% and paper & chm-20%),

Textile PBT margin - 10%,

Paper & chm PBT margin- 38%

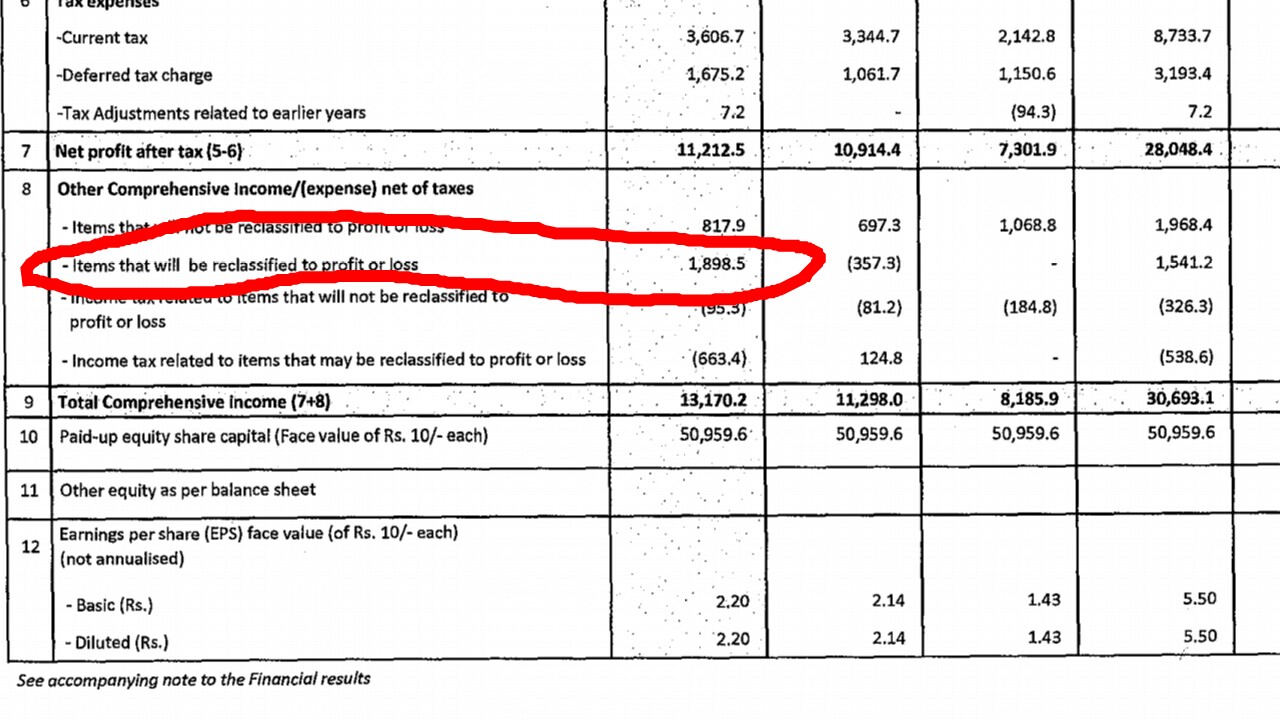

Can someone please help to understand what is this for. Nothing mentioned in note section. This added quite a good amount in overall profit.

Investor presentation post Q3FY19 results. Better results, Debt reduction, Promoter stake increase.

Improving capacity utilisation in Bed and Bath linen is key for future growth.

Press release.

Management is running extra mile to provide forward looking info on Industry outlook and Trident perfromance.

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=68f44f7e-ed21-42b8-8826-0882a6438516

Trident has been granted a patent for “Environment Friendly Fabric and its method of Manufacturing” by United States Patent & Trademark Office.

The present invention enables Trident to manufacture fabric for bed & bath products without the use of chemically harmful fibers and at the same time allowing the fabric to be absorbent , easy to dry and highly breathable.

Consumers across the globe prefer such bed and bath products. The grant of this patent provides further recognition to the focus on quality of the innovation that is always being carried out by the Trident team.

Any comments on longevity of the company and how much top and bottom growth can we expect in next three years? I found that there is double digit increase in profit, however sales are increasing in single digit only. Just analysing the company as new learner.

One thing to note is trident holds 1,785,714 shares in IOLCP which has gained traction because of IBP prices (BASF incident).

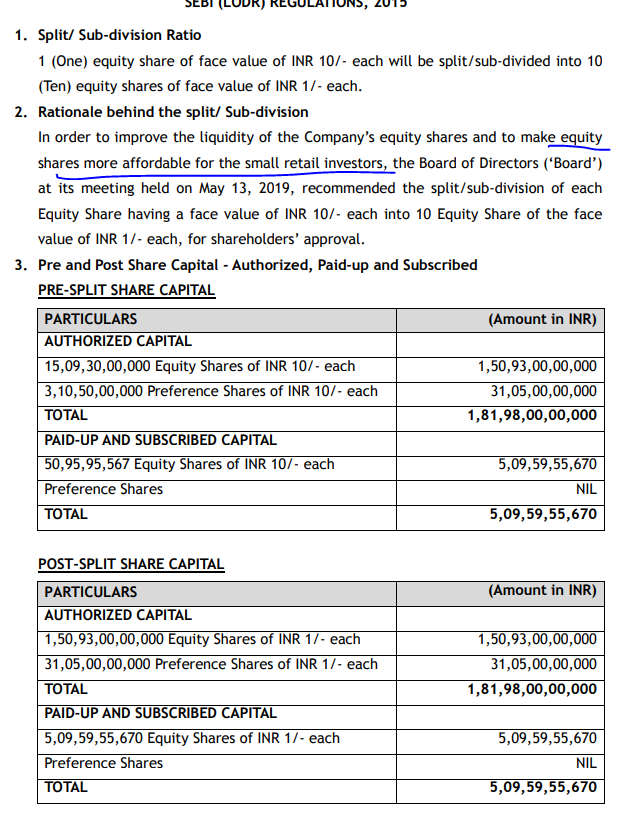

Trident’s reasoning for splitting the shares so that it can make it affordable for the retail investors in not in line with good corporate governance practise. The company’s D/E is at a reasonable 0.9 and the cash flows healthy. The company has pointed that it wants to make the share cheaper for the retail investor. The company is currently valued around ₹60. Splitting it further will only allow for more speculation in the share price and will create too much volatility. The company is not acting in the interest of share holders.

Disc: Holding trident for the last 5 years.

I agree. Seems weird going for a 10:1 split when the stock price is currently only in 2 digits.

Seems to me it will be a good case to study what happens to stock price when managements do this to attract small investors  . I will watch this one closely to see if such opportunities offer 30-50 percent upside for future use.

. I will watch this one closely to see if such opportunities offer 30-50 percent upside for future use.

Not taking away from the morality of the issue, just wondering what these shenanigans yield the promoters and shareholders.

planning to enter right now or waiting to enter post split? Actually I am tracking this company and was planning to enter. But suddenly got this news. Little confused as what will be the impact of this news. Thanks

I am not going to put any money. Will just watch as a case study