TRIDENT

Trident Limited is the flagship company of Trident Group, a USD 1 billion,Indian business conglomerate and a global player. Headquartered in Ludhiana, Punjab.

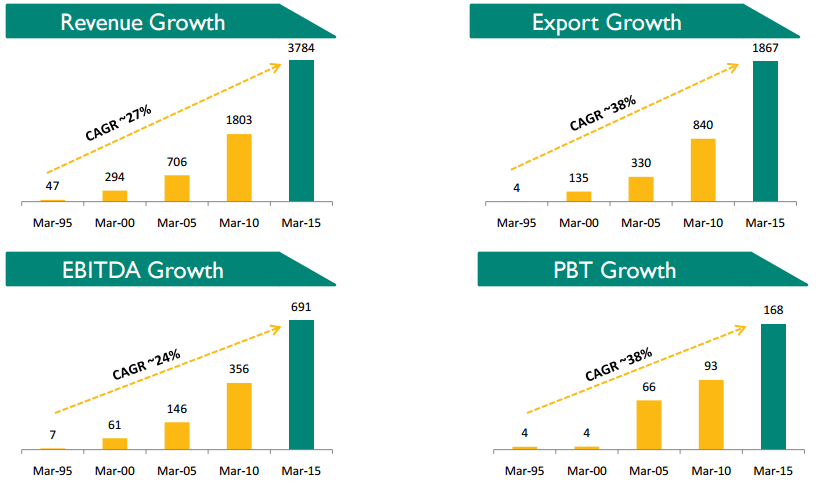

It’s a 25 year old company with CAGR of 30 %

Trident’s customer base spans over more than 100 countries across 6 continents and comprises of global retail brands like Ralph Lauren, Calvin Klein, JC Penney, IKEA, Target, WalMart,Macy’s, Kohl’s, Sears, Sam’s Club, Burlington, etc. With export turnover accounting for about 50% of total sales of the Company.

Trident is the largest terry towel and wheat straw based paper manufacturer in the world.

TEXTILE:

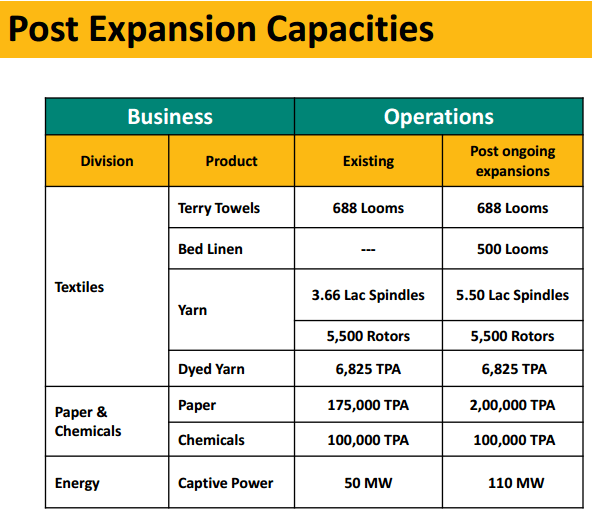

Fully integrated home-textile operations with terry towel capacity of 360 million pieces of towel per annum

Composite Bed Linen Project is under implementation & expected to be commissioned by second half of FY16

Implemented the world’s largest terry towel project at a single facility in Budni (M.P.)

One of the largest cotton yarn spinning capacity in India with 3.66 lac spindles capable of producing 8400 MT/month of cotton and blended yarn

PAPER:

Agro-residue (wheat straw) and ECF pulp used to manufacture paper Customers across 50 countries including India, Middle East, Africa, US, Latin America and UK, among others

KEY POINTS

- Product availability in all major hypermarkets and supermarkets

- Expanding sales through e-commerce in domestic and international

market ,Exclusive brand store on Snapdeal - Successfully entered new markets like UK, Italy, France, Japan,

Australia, South Africa and Canada - Energy-saving operations initiated to reduce power consumption

- Company also issued first interim dividend recently

- TPM Policy has been formulated across the organization to achieve

zero accidents, zero defects and zero breakdowns - Strong management team and strong credit rating (CARE A-)

Risks

- Debt / Equity Ratio stands at 1.77:1, Debt level increased due to expanded capacities

- CMP/BV = 2.29

- Composite Bed Linen Project is under implementation & expected to be commissioned only by second half of FY16

Company website: http://www.tridentindia.com/content/home.aspx

India is the second largest producer of cotton, textiles & garments and is the only major textile exporting country with a net cotton surplus - constitutes ~20% to the total cotton cultivation area.

As textile sector is currently doing well, i believe this stock will perform better and i took small exposure at CMP 46 and will hold it for long term.

If anyone come across any other risk/concern about this company please share, Thanks