AR Link: https://linkintime.co.in/website/GoGreen/2019/AGM/Transpek_Industry_Ltd/Annual_Report.pdf

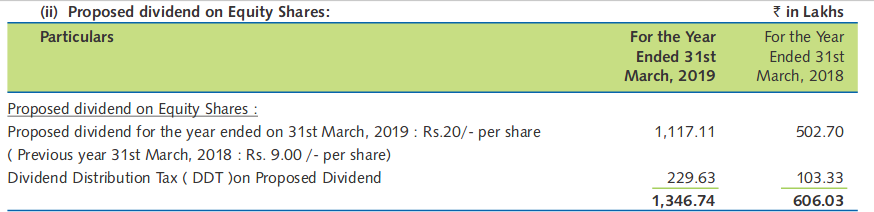

Your Directors have recommended a dividend of Rs.20/- (i.e.200%) per equity share of Rs. 10/- each on the Equity Share Capital of Rs. 558.56 Lakhs for the year ended 31st March, 2019 (previous year: 90%, i.e. Rs. 9.00/- per share).

overall outlook for the Indian Chemical Sector continues to remain positive on the backdrop of increasing global demand and state of Chinese chemical manufacturers remaining unchanged. Global chemical companies are exploring the opportunities of making strategic alliances/partnerships and investments with Indian Chemical companies. The demand for Raw Materials and Intermediates is on the rise.

The constant pressure on Chinese chemical manufacturers continues to provide an excellent growth opportunity for the Indian Chemical sector.

The Company successfully maintains excellent business relations with all its global and domestic customers and supplies large quantities of Acid and Alkyl Chlorides. The Company is poised to capture the growth potential expected at present and in near future.

AGROCHEMICALS: The company continues to maintain steady supply in the agrochemical segment. The overall agrochemical sector has seen an expansion, however, the given segment continues to remain extremely price sensitive. Considering the nature of this segment, the Company has strategically decided to focus more on other business segments.

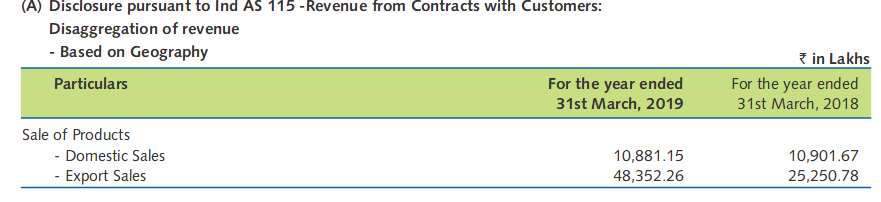

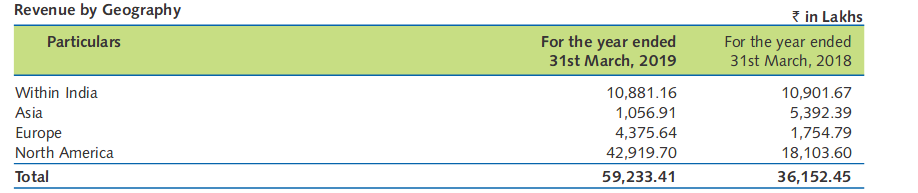

The revenue increase was mainly from exports. Domestic sales are flat and that too from US and Europe.

90% vs 200% divdend and returning 13 crore (inc DDT) to investors.