@dd1474 These are part of other comprehensive income possibly resulted out of 1) M2M on their investment of 156650 shares of Excel Industries Limited. 2) M2M on their open forex positions 3) M2M on their 7.87% stake in Transpek Silox Industry Private Limited (but whether M2M is needed for unlisted company I am not sure & you can update).

These Other Incomes doesn’t affect the EPS calculation as this is done without considering those.

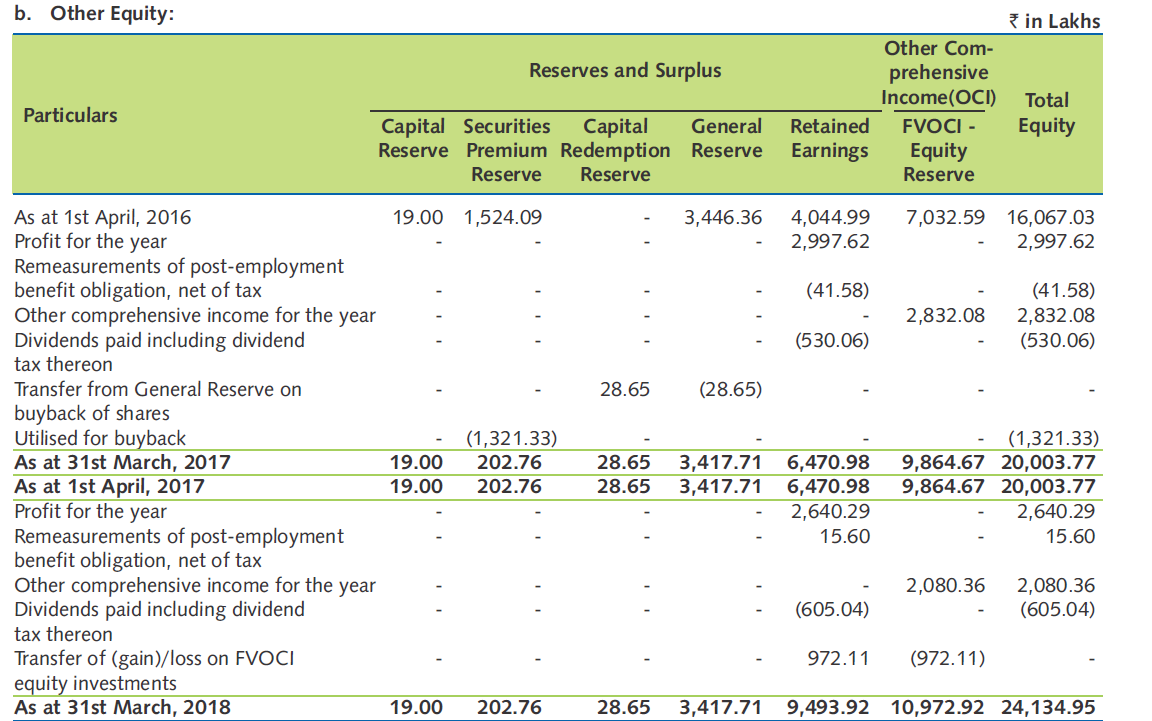

Most importantly, the ROE got depressed due to addition approximately Rs. 100 Cr to reserve and surplus in 2018 as Other Comprehensive Income as you can see from below snapshot of AR 18.

It has made the calculation of true ROE quiet a bit tougher.

I feel number are showing that the company has achieved good operating rate on new project. we are not sure whether current capacity fully utilised or there is further scope for sales growth. Since there is no volume information available, we can read sales value as next best proxy indicator. The Q3 performance justify current price in my opinion. I would continue to hold my position at current level. Not sure whether answer your question but frankly, I do not know beyond what I have wrote.

Fantastic nos indeed. It clearly seems that the scale up has been happening on the MNC contract.

Interestingly as per the Sept 18 balance sheet, there was a CWIP of about 50 Cr hence it seems further expansion might be underway or would have just happened.

am new to the co in terms of doing research on it. are there any one off contracts which got booked in q3 or should we expect the current run rate on the topline to continue going forward. The margins seem to be stable across many quarters.

As per gujarati newspaper gujarat samachar, there was a fire incident in which 5 workers were injured severely and admitted to a private hospital in baroda. Out of these 2 were discharged and 3 are still undergoing treatment.

The authorities have ordered closure of 3 subunits involved in manufacturing some specific product. Whereas fire was there in one unit.

No announcement from the company on exchanges till now.

The plant as per the latest announcement was closed and as per my scuttlebutt, would be up and running once the remedial plan is approved by the authorities. The company manufactures some part of its production from a toll arrangement from a group company at Pilodra.

Numbers wise margins has shown a big jump in q4 fy 19. On a topline of 171 crores, net profit is at 30 crores for q4 fy 19 whereas for q3 fy 19, sales was 171 crores and net profit was 14 crores.

Full year sales was 595 crores and net profit is 70 crores giving eps of 118 per share.

Looking at the balance sheet, Property plant and equipment has gone up from 178 to 236 crores and there is still capital work in progress shown as 33 crores.

Total debt has reduced from 180 crores to 120 crores. Revenues has gone up from 364 to 594 crores whereas trade receivables has remained same at 93 crores while inventories has gone up from 46 to 56 crores an increase of only 10 crores after a revenue growth of 230 crores. Seems balance sheet is gettting stronger.

Dividend of Rs 20 per share declared . (as compared to rs 9 per share for previous year).

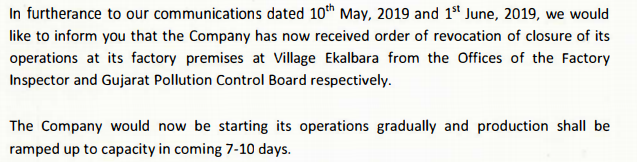

Next key monitorable is when the plant starts. The next AGM should provide some answers to the kind of trajectory the company is targettting.

Sir, any quantitative analysis of loss (/impact) in production bcoz of this shutdown?

Lot of chemical companies have loopholes in safety. I would say transpek will sail through inspection smoothly and plant will resume as usual. In my opinion , mgmt who are shareholders friendly tend to be more generous about well being of their employees including safety aspects at work.

It’s surprising that even after reporting of shutdown, share price didn’t go down. This shows stock is in strong hands.

Disc- liking this group (the shroffs) . Invested in Excel Ind. May enter in transpek too.

been tracking this co for the past few months…can you detail what is the reason for such spike in margins…raw material cost going down led to the growth in profits…are there any one offs in terms of temporary spike in margin or can it sustain at these levels

Transpek management has good reputation in the local geography and are well known for their philanthropic work through the Shroff foundation.

Coming to the fire incident, 5 workers were injured due to the incident, and there were no casualties. The management was quite proactive in taking these employees to private hospitals for treatment.

A local newspaper reporter had started doing a string of articles related to some old episode many years back relating to some issues of employee compensation which as far as I know was settled at that particular time. And as these things were going on as luck would have it, the fire incident happened. Because of this there was a lot of media coverage given to this episode and in view of impending elections I guess the authorities had no choice but to take stringent action.

@vivekchoraria, Business wise transpek remains a black box with very little details available in the public domain. Even the management doesn’t communicate much in the annual report or during AGM. They do take questions at the AGM but give answers only on a need to know basis and hence too much details about the business segments or their margins are not available.

Whether these margins are sustainable or not only time will tell. My rough back of the envelope estimates for fy 19 and FY 20 were EPS figures of 90 and 120 respectively. So this eps figure of 118 for FY 19 comes as a pleasant surprise. Lets see how things pan out.

so you are saying the investors relations team might not be open to discuss the prospects. Any particular reason you think why this quarter saw such a big spike in margins…and any idea of what market share do they have in their product profile.

Regarding margins and market share and rest of the lot your guess is as good as mine. As stated before in my post most of the business of the company is a black box with few details available. So anything I try to answer would be mere guess work.

Only thing which is well known is that the company has a multi year contract with an MNC for supply of a speciality chemical which seems to have started contributing meaningfully from q3 fy 19. Some scuttlebutt provides the insight that the new MD Bimal Mehta is more aggressive for growth as compared to his predecessors. If the company because of the Chinese disruption or because of its own expertise in its own niche chemistry can get more such contracts, it can be in a different orbit altogether. And with the kind of results it has posted, the downside in the immediate term seems limited.

Its heartening to know that atleast some manufacturing is going on at other tolling locations. I knew about one location keeping production alive at Pilodra but with 3 places being alternative production sites should limit production damage.

Other thing to monitor would be insurance claim. If it includes loss due to loss of production, they might recover some money out of insurance too but that is a question that management needs to be asked and even if asked as of now they wont have much idea how much insurance claim would be approved if any.

The other key monitorable is how soon production is allowed to resume from the Ekalbara unit.

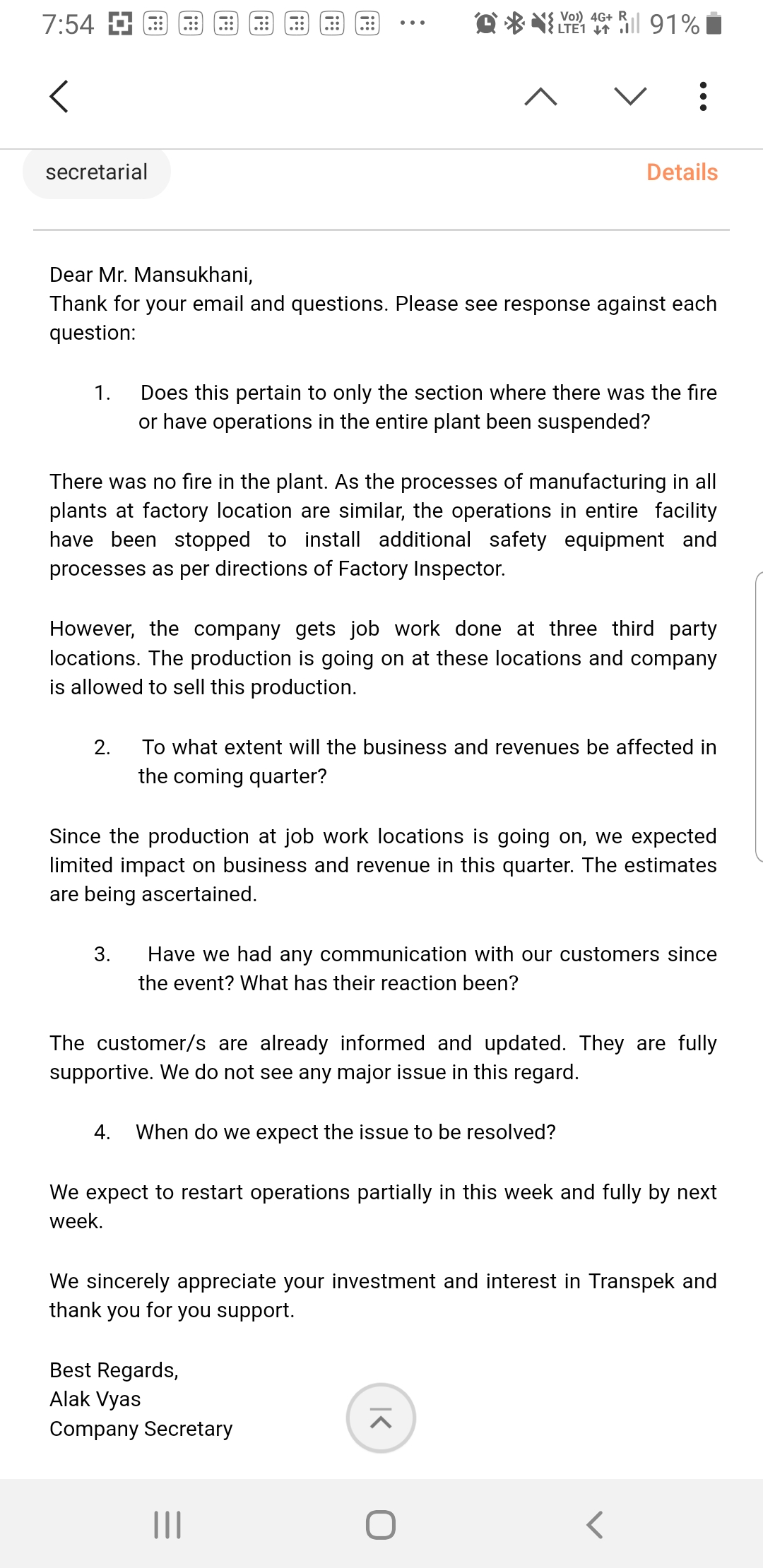

Its good to see that a company that is very reticent in giving information is responding to emails in a detailed pointwise manner.

How would you look at the jump in ebitda margin from q3 to q4? I am guessing doubling of margin percentage will not be sustainable. What would you say are the monitorables here…i recently sent a mail to th the co and got the following response…

1- What was the total capacity in tonnage that was on stream after the expansion and what is our capacity utilisation as on q4 fy19.

Our capacity utilization was full for most of the products in Q4, 2019. The total capacity in tonnage has been disclosed on BSE on 27 May

This has already been done.

2- There is still some CWIP reflected on the balance sheet. What will be the total capacity available after that is commissioned.

Some additional installations in supplementary equipment and utilities are being done besides significant replacement in one plant. This

is not going to result in any additional capacity.

3- Do we have a multi year contract with the mnc and has the expanded capacity been set up only to cater to that customer or will it be used to service all clients.

All our plants are set up to cater to multiple clients. However, due to quantities involved in long term contract, three plants are used for catering to the demand under contract.

4- There is a big spike in operating margins in q4. were there any one off’s in terms of prices of raw materials coming down or are these margins sustainable? Historically we have done about 15-17 per ebitda margin but this quarter we almost see to have doubled it. What has led to this and what are the sustainable margin levels on the expanded capacity if you can give some broad range.

The nature of raw material pricing and our product pricing in relation to it, product mix, target quality of our product etc. are multiple

variables that affect the profitability from quarter to quarter. To get a better idea, it is recommended to look at annual profitability

considering nature of the business and variables involved.

5- Do we have any plans to list the company on the national stock exchange to enhance liquidity.