I attended Transpek Industries AGM on August 10 2017. Find enclosed my notes on AGM and other discussion. Please note that Transpek is among my Top 10 holdings and my views may be biased due to my holding. Also, there may some communication error from my side and reader should do his/her own due diligence before taking any decision.

Chainman speech

The company is specialised in Acid chloride which has applications in polymer, Performance materials, Flavour and Fragrance and Agri pesticides. The company is in discussion for long term supply contract with various customers of which one such contract is signed and announced in April 2017. The company would undertake investment in plant and equipment and focus to complete construction for this project by December 2017.

Aggressive marketing, superior quality, wider range of products and compliance with superior environment, safety and health standards by company results unique competitive position for various MNCs companies looking at suitable long term suppliers.

Business condition are stable in domestic market, while US and EU economy is showing improvement in economy growth results in better demand for the products of the company. Superior operating efficiency, sustainable product process, customer satisfaction and increased focus on improving process capabilities would be key growth driver for the company in medium to long term. The company would focus on more value added product and higher products to drive its profitability,

Transpek has subsidiary in Europe which is commercial company fulfilling requirement of REACH regulation stipulated by EU.

Q&A:

New project

The company has taken all safeguard for forex and other market risk factors while executing contract with MNC. Transpek expect additional sales of around Rs 140-160 Cr per annum which is around 60% of total income in FY16. Transpek was in discussion with this MNC for almost 2-3 years for the project. It is also in discussion with other such projects but same is highly uncertain about final outcome.

Acid chloride

Acid chloride is building block which has usage in multiple chemicals. There are around 1200 chemical which require various forms of acid chloride. Transpek manufacture 12-13 products regularly as per market trends. The customer of the company also does not disclose information about enduse due to patent/confidentiality related issues most of the times. Hence, it is very difficult to estimate volume demand and end use for the company products.

Acid chlorides are hazardous chemicals. Customer recongnise consist quality and ability of the company to manage multiple acid chlorides and supply at competitive prices. Hence, Transpek would continue to remain dominant player in Acid chloride.

There is EU based company Kemin Chemical (not sure about spelling). Most of the other competitor operate on lower scale and also have limited integration as compared with Transpek which result in superior competitive position for the company.

Current manufacturing infrastructure and environment approval

The company has large land area of 100 acres of which only 35 acres is currently being utilised. That provide for sufficient area for increasing capacity in future for growth.

The main constraint in setting up new capacity is more from environment approval side. It takes long time for the company to get environment approval for new capacity. The company already have environment approval for new project with MNCs. The company consider the expected time line in getting approval for environment and accordingly proactively moves while planning enhancing capacity. There has been also various regulatory bodies from state pollution board to National Green Tribunal to Supreme court, which at time have conflicting view on environment aspect which also increase complexity.

The group (other companies from Excel group) which various entities which are specialised in certain specific area and have various environment approval in place. At times, the company take advantage of these set up, by entering into an arm length transfer pricing, for a specific product needed by client.

During FY17, the company did enter into tolling arrangement with one of the related parties which have free capacity along with environment approval to take advantage of customer requirement for a particular product which is shown in contingent liability of FY17 annual report.

Client

The company refused to name customers as it is bound by confidentiality and also have high penalty clause on breach of confidentiality.

Capex

Total capex is around Rs 90 Cr for new project. That would be funded by internal accruals and bank borrowing. The company incur around Rs 25 Cr as maintenance capex.

China competition

The company products are specialised and it does face any major competition from China. In fact, in certain products, Chinese players have started importing and using Transpek product due to superior quality as compared with what locally supplied by Chinese companies, specifically when the Chinese companies are expected to export the final chemical to Japan.

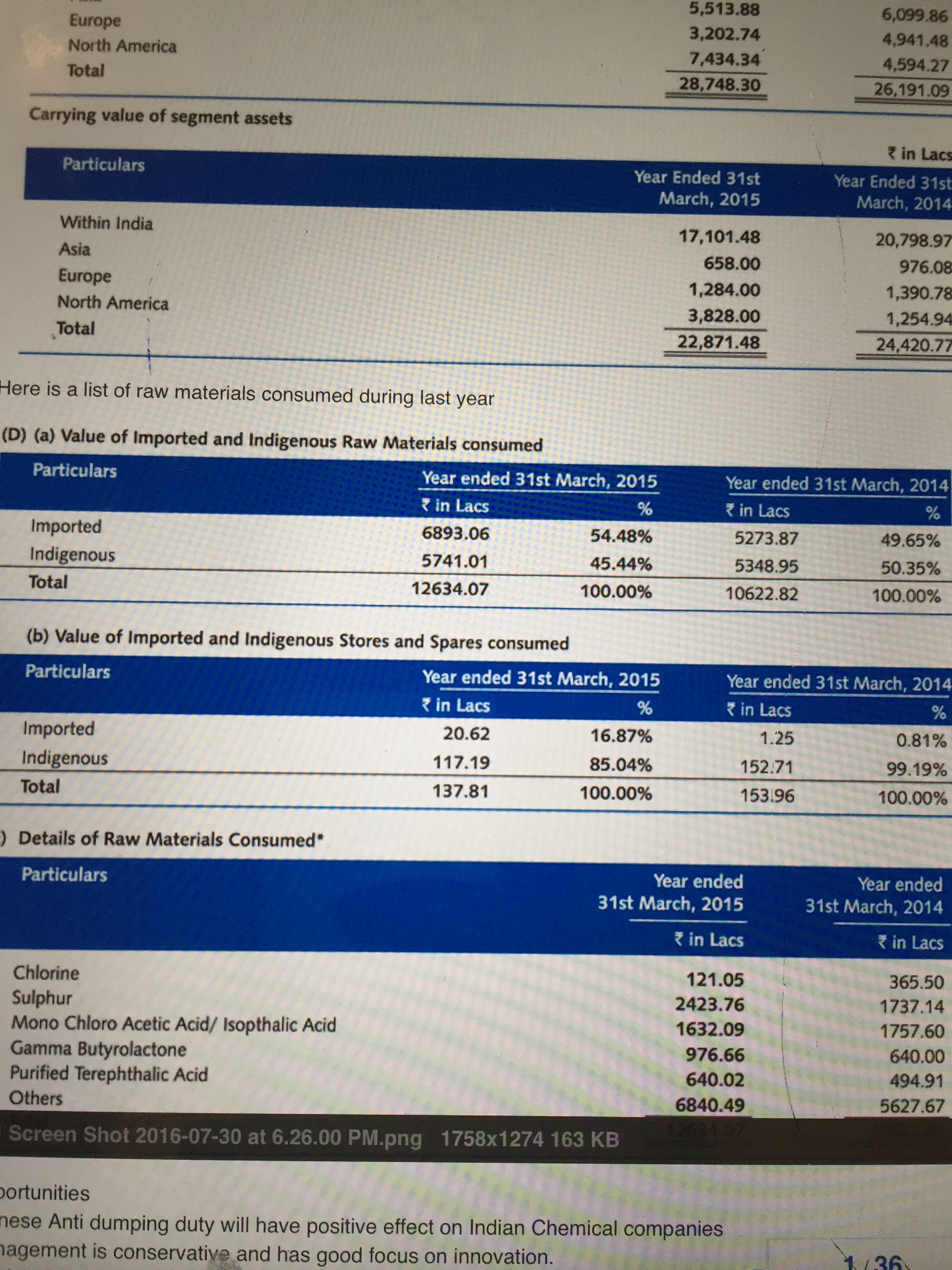

Regionwises sales

Over the period, the company’s sales to EU has been declining while to US is increasing. The slow down in EU economy growth and higher demand for polymer enduse were the main factor behind increased share of US in export for Transpek.

Q1FY18 results

The company performance was adversely affected by rupee appreciation and lower dividend income (around Rs 1.5-2 Cr decline). There was spurt on one of the chemical input, price of which went up by almost 6-7X during Q1FY18. The price of same started declining from July and company is also in discussion with the customer for revision in price of that particular product. The company would continue to face such market volatility in future as well. However, over a period of time, the company ensure that it improve its margin and achieve sales growth.

Other points

The company would consider Transpek Silox as strategic investment and would not like to liquidate same to fund the capex requirement.

My view

Acid Chloride chemistry+ Sustainable development+ Good management were the key highlights of Transpek AGM. However, management is relatively mature (expect Mr. Ravi Shroff) and hence moves steadily rather than aggressively which has its own limitation, especially when we are looking at high growth environment in medium term in my opinion.

I would request other VP members to add/edit my notes to reflect true discussion.