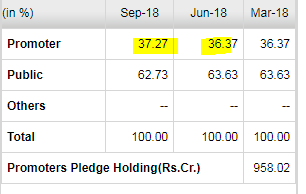

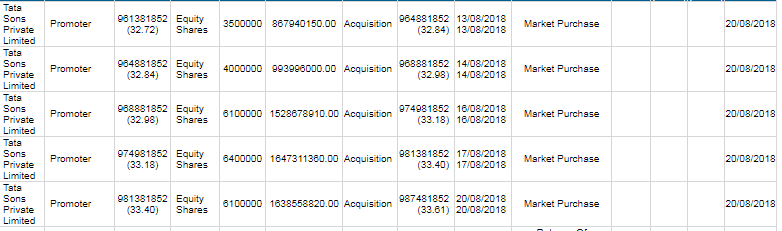

Tata sons bought 2.61 crore shares and not 98 crore shares. They’ve increased their shareholding by 0.89% from 32.72% to 33.61% (including DVR shares).

1 Like

Thanks for clarifying. The moneycontrol article was a bit misleading.

Promoters checks into the battered down stock!!

The new 2019 Jaguar Ipace v/s Tesla. No doubt its an ad but you’ve got a competitive product here. Seriously considering TaMo looking at the reviews.

3 Likes

I-pace is arguably the best electric car till date. Way ahead of Tesla in all departments. Only questions is can it make significant impact to the top and bottomline of JLR in the medium term since the production volume would be relatively small.

1 Like

While it’s a well established fact that iPace is a great vehicle & it should give good sales numbers for a few quarters (as long as production catches up with the demand), does anyone have any idea about the margin for the product? I am concerned about this because in past Tata motors had admitted that they were losing money for each car produced

I think that were before Nexon and Tigor s arrival … Please check recent PV sales for past 6 months Tigor,Nexon and Tiago sales were good. There are 3 to 5 models in pipeline in PV segment. If that clicks then Tamo would get consideralble amt of revenue frm them. Also TAMO shud list JLR and rest of the arm separately to unlock the full potential of turnaround story. JLR weak sales hurts the TAMO s solid Domestic performance…

1 Like

This is a year old link, it is pretty well known they were losing money in passenger cars. However if you see the latest investor presentation/ concall, they are close to breakeven at EBITDA in PV segment - more specifically from 20% negative EBITDA they are 1% negative EBITDA YoY, which is a huge delta. YoY revenue is up 63% (though on a low base and probable GST impact last year), nevertheless there is a real turnaround here…

I personally believe at EBITDA should be breakeven by next quarter or the one after, net level not so sure.

2 Likes

The company seems to be meeting with a LOT of funds and analysts. Signal of increasing institutional interest?

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=daf8e598-e259-4b84-9005-04cafa1eb29d

TAMO PV sales in August… https://m.economictimes.com/industry/auto/auto-news/tata-motors-domestic-sales-up-27-pc-at-58262-units-in-august/amp_articleshow/65635329.cms

1 Like

3 Likes

Agree with this author. Although Tata Motors has been a value destroyer - valuations have become very attractive now. They are taking the right steps to lower diesel vehicles and increase EV vehicles into their portfolio.

Very long term story is unclear as the competition is very high and all major OEMs are burning cash.

1 Like

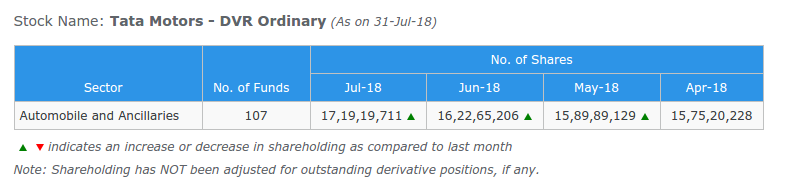

Mutual Fund holdings of Tata Motors - DVR has been constantly increasing from the last 3 months ( i.e. July’18 , Jun’18 , May’18)

Source : https://www.rupeevest.com/Mutual-Fund-Holdings/217889

1 Like

It’s trading at six-tenths of its book value. These valuations for a company that owns jaguar are too tempting to stay away. On visits to the UK, I see JLR is quite popular and believe it will remain so in the near future irrespective of how the Brexit story plays out.

Disc: Invested. Took more than a nibble today.

3 Likes

CRISIL revised the outlook on the long term rating of TML from ‘Positive’ to ‘Stable’. Some key points of report is as follow

Strengths

- Robust product portfolio and strong brand in the global luxury automotive segment

- Strong market position in CVs; weak but improving performance in PVs

- Strong financial risk profile

Weakness

- Weak operating performance at JLR owing to challenging market conditions and increased business risks

- Large capex at JLR to result in negative free operating cash flows over the medium term

Upside Scenario

- Healthy and diversified growth in JLR volumes along with improvement in profitability

- Sustained strong financial profile with improved operating leverage and lower capex intensity

Downside Scenario

- Further weakening of operating profitability with slower growth

- Larger debt-funded capex, leading to moderation in its financial risk profile

1 Like

Pick-up in iPace sales. The demand seems to be there, will be interesting to see if JLR is able to ramp up production - https://insideevs.com/jaguar-sold-710-i-pace-september/

Tata Motors promoter holdings has increased by approx 1% in Sep quarter. Tata Sons bought shares worth 650-700 crores in Aug from market at approx 265-270 rs.

2 Likes

https://seekingalpha.com/article/4212162-jaguar-pace-outsells-tesla-s-x-combined-40-percent-norway

The ipace has been doing pretty well in the Norway market. Outselling Tesla S and Tesla X combined. Norway is considered an indicator for how things might be in other developing EV markets. I think these are good signs moving forward.

3 Likes

JLR began construction of a new manufacturing facility in Slovakia during Sep 2016 (#1). They were expecting the production of vehicles at the new facility to be started during late 2018 & the project was estimated to cost about UK £ 1 billion. This type of large projects usually take a lot more time & money than estimation however Tata motors achieved it within estimated timeline & budget (#2). This tells a lot about the direction in which the company is heading. While domestic business is turning around, JLR continues to show extremely professional performance (despite losses in previous quarter).

#1: https://www.tatamotors.com/jlr-press-release/jaguar-land-rover-begins-construction-of-slovakian-plant/

#2: https://media.jaguarlandrover.com/news/2018/10/jaguar-land-rover-opens-manufacturing-plant-slovakia

Disc: Invested, views might be biased.

1 Like

Decent volume growth continues. I expect Diwali falling in November this year should imply November to also show robust sales.

36937035-3010-4a14-bc02-3c40121f6f5a.pdf (484.7 KB)