The recent Dr. Reddy’s warning letter is a grim reminder of how data (integrity & audit etc…) related issues are a major headache for the pharma companies. We can argue that the data doesn’t come into existence from thin air. It’s the actual work of pharma players which in turn manifests in the form of poor data.

But i think somewhere there is a connect between how easy it’s to manipulate data which leads to these bad practices from pharma players.

Please go through the FDA warning letter to take a deeper look at the number of data related issue.

From linkedin searches, looks like Take solutions employees are predominantly work in regulatory filings to various regulators like USFDA, Europe etc. They help in “Cordination, Compilation and publishing the dossier in e-CTD format (e-CTD EXPRESS), for US, & LATAM. Submission of Annual reports, PADERs, CBE, CBE-30, PAS etc.

Archival of the submitted submitted dossiers and related documents in RADARS

TMF upload” by providing the software support to pharma company in the form of SaaS.

In below link, you can find some information on filing eCTD doc and how SaaS company can help pharma company on filing http://apic.cefic.org/pub/eCTDHowtoDo_final%20201407.pdf

A web-based electronic Document Management and eSubmission Solution

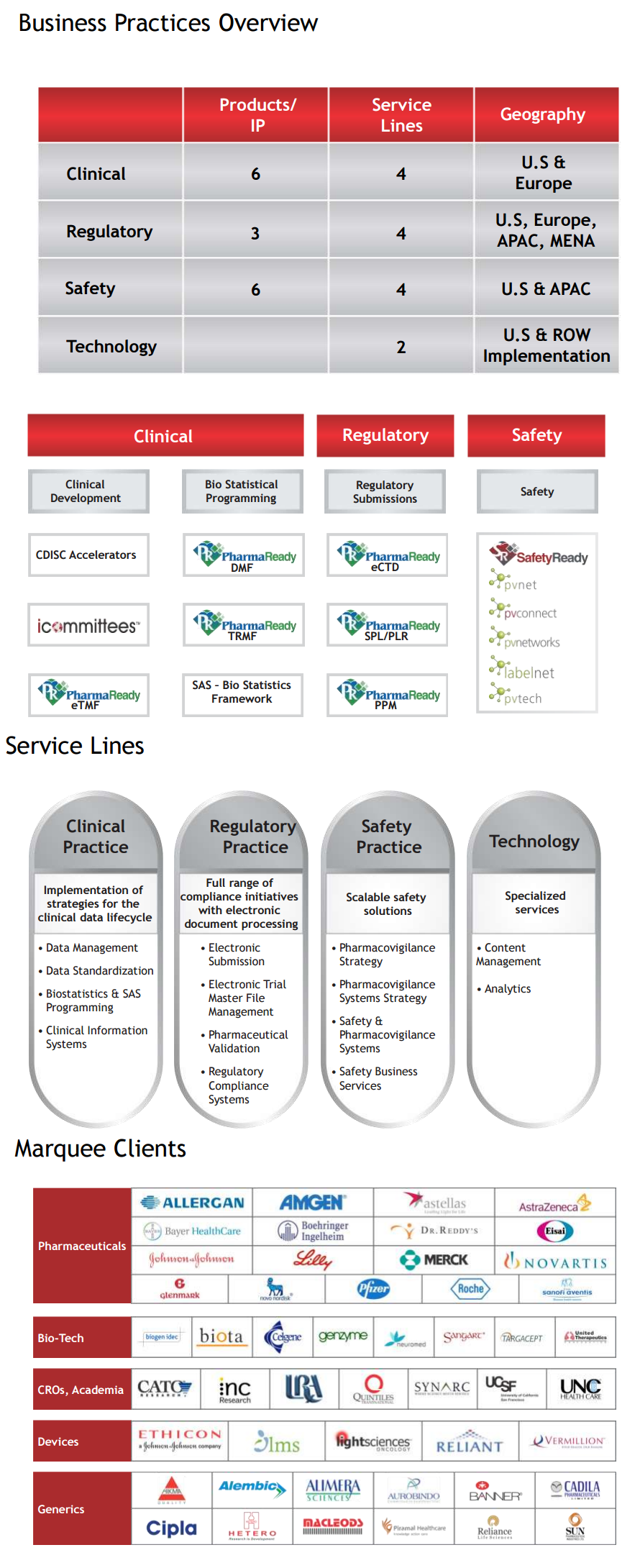

PharmaReady is a web-based electronic Document Management and eSubmission Solution suite specifically designed for both emerging and large Life Science organizations where ease of installation, ease of use, regulatory compliance, and affordability are the primary business drivers. The PharmaReady solution suite is designed specifically for management of SOPs, Work Instructions, Training Records, eCTD Submission Documents, and all other electronic documents. PharmaReady is in full compliance with global regulatory requirements.

PharmaReady Complete Suite is a tightly integrated, cost-effective document and submission management product tailored to the needs of the following small, medium and large life science companies, including start-up ventures:

• Pharmaceutical

• Biologics

• Medical Device Manufacturers

• Generic Drug Manufacturers

• Animal Health Care

• Clinical Research Organization

PharmaReady Suite provides seamless visibility into the entire regulatory document management lifecycle, from document creation all the way to regulatory submissions. PharmaReady Suite is also available à la carte with individual products.

PharmaReady Suite is a comprehensive compliance solution that helps you to define and manage all your quality / regulatory document and submission needs.

PharmaReady Suite is FDA 21 CFR Part 11 compliant and is also compliant with other country-specific regulatory frameworks.

• DMS - Document Management System - Efficiently manage SOPs, Work Instructions, and other documents within regulated business areas.

• eCTD - Electronic Common Technical Document-Easily submit in the FDA-recommend XML format while supporting submissions lifecycle management, role-based authoring and intuitive electronic content assembly processes.

• SPL-PLR - Structured Product Labeling - Achieve immediate compliance as well as improve your entire product labeling process.

• TRMS - Training Records Management - Seamlessly manage technical training and maintenance of training records.

• PharmaReady Hosting - PharmaReady On-Demand - Minimize start-up costs with nothing to install on your site. No customer hardware or software is required.

• eTMF - Electronic Trial Master File - Fits perfectly well with DIA’s Reference Model for the TMF (Version 1.0, June 4, 2010)

PharmaReady 6.0 provides seamless visibility into the entire regulatory document management lifecycle. PharmaReady was launched in 2006 and is used by companies in the US, Europe, India and the Middle East by over 80 Life Science organisation.

Foreign Acquisitions/Peers

During April 2010, Oracle acquired Phase Forward, a healthcare and life sciences software provider, for $685 million. Phase Forward’s Integrated Clinical Research Suite manages the drug submission development and safety processes from trial to submission to the Food and Drug Administration and other authorities. In 2009, Phase Forward delivered revenue of $213.3 million and net income was $8 million. This means that Oracle valued Phase forward by 3.2 times in 2009 revenue. Similarly during August 2012, Accenture completed its acquisition of Octagon Research Solutions, Inc., a provider of clinical and regulatory information management solutions and software for the pharmaceutical industry. The detail numbers with respect to valuation and business operations of Octagon are not readily available in public domain.

Another company which can be compared with TSL is Medidata Solutions Inc. Medidata Solutions is an American-based multinational computer technology corporation that specializes in developing and marketing cloud-based solutions to address functions throughout the clinical development process. This company is one step ahead of TSL as it offers cloud based solutions. Its TTM revenue was $320.4 million and PAT was at $1.22 million. Its market cap currently is about $2.38 bn with equity capital of $0.053 bn

Regulatory Publishing/Consulting

The Regulatory Practice offerings include Regulatory Strategy Services, BPO Regulatory Publishing (including Submissions Management and Artwork and Labelling Service Offerings) and Regulatory Information Management. With the deep experience in regulatory submissions operations, TSL has developed its own Regulatory Information Management Analytics tools. TSL’s Regulatory Publishing team has produced over 26,000 submissions for clients in US, EU and India. This experience has also given the company a unique insight into the requirements of Regulatory Information Management Systems.

How did the business begin, and have you grown at a consistent rate for a technology business?

When I explained my business model to Mr. Thyagarajan, he said that it will take you twice the amount of time, and thrice the amount of money you envisage to begin the business. I don’t think he went so much into the technology, but he went more into the perception of what it takes to establish a business, and his own judgment of how long businesses take to establish. So I told him I just want to do this well. This was in the year 2000. He otherwise liked the plan and said it was good. So that’s how it began.

The first business plan was to be a product company in the supply chain space, but restrict ourselves to the supply chain space, and be a product company. The clarity that existed then and continues to exist now and the consistent thought was that we will never be a general IT services company. It was the worst time to start a technology business in 2001 because tech businesses globally had crashed. Well, the Shriram Group didn’t really put seed capital. I have been a supply chain guy. I’m still a great fan of supply chain. I absorb that subject very well. The first product was in supply chain, and it was a very simple warehouse management system, which was sold in Malaysia. It will plug on to an ERP. See those products exist not in our system any longer, because they are commoditized products. See price pressure comes in so unless you stay ahead of the curve, when you are doing something very unique and different, you are not going to be able to command a premium. The first client was won because of my personal credibility, with the Temasek Group, than on the credibility of the company. After a few years we said, okay, it’s not going to be easy in the warehouse space because it was commoditized. From there we went to the production floor because that’s a least – a lesser penetrated area. From there on we said, listen, I think this is not enough. We need to move to developed markets. So we were originally only in Asia-Pacific. Then we said we will have to move to developed markets. That’s how we found the idea of building a product for the pharma industry.

Analytics must be an important business for you? We also do analytics and we do submissions. But we don’t do data capture. The number of people you require in data capture will be about 10 times of what you would require in analytics. So let’s say the way I data capture for a clinical trial in India is different from how it is done in other countries. Now, all the data collected has to get into a common format. So you will have to do manual intervention at different points of time. You will be very surprised that pharma companies are talking about using lot of data analytics. There is also use of the word big data because data from other sources is engineered to make inferences with data from social media. Today pharma companies want to track websites to understand what people are saying about the drugs and it is mostly because of the adverse events created by a social media event. For example, if it is reported on social media that the drug consumed created side-affects, if not already stated, then the lawsuits that can follow are expensive and time consuming. Let’s take – say a company ABC has manufactured a drug – and I take that drug for a particular therapeutic problem. If I continuously have a stomach ache or headaches that become very serious then the propensity to report it on social media today is very high. This is where companies want social media also integrated in the analytics stack.

What makes Take Solutions a serious player in the pharma industry as a technology vendor?

We do the regulatory filings for companies and it is a service. Our product PharmaReady does this for our clients. So what the pharma company sees is the value addition we do in terms of making a regulatory filing easy. We use the data to draw inferences on how a particular clinical trial is going and then you use the data to make regulatory submissions. Cumulatively today we have done more than 200,000 regulatory submissions across 29 countries. … This is typical engagement with a pharma company. It’s not necessary for a pharma company that you must buy and own PharmaReady.

The life science business is not new for Take. But, why this emphasis to rebrand this business as a separate subsidiary, with Navitas, in January? Are you looking at inorganic opportunities?

Yes, we started our life sciences business somewhere in 2005. In 2010, we had an excellent overall EBITDA (earnings before interest, taxes, depreciation, and amortization) of 23-24 per cent. However, as parts of our SCM business started getting commoditised our margins suddenly started tapering off. In 2012/13, our EBITDA reduced to 15 per cent. That is when we decided to do a drastic overhaul. During the end of last financial year and during a large part of the current financial year, we walked away from Rs 220 crore worth of business. It was not easy. It upsets shareholders, it upsets the board, it upsets your employees. You keep touching a lot of volume, but if you are basically going off, it’s not a profitable growth. So, we said, let’s go back to profitable growth. We set ourselves a goal, saying that by 2016/17, we will be back at 24 per cent EBITDA. We will be able to do that with the help of the life sciences business, where we have a competitive advantage and an edge in the marketplace. A large part of our investment is going into life sciences and we think it’s a growth opportunity. It’s an industry where outsourcing is just taking off. What most players do today is still largely in-house.

Now on acquisitions. Do we want to bulk up? Yes. But for that, it will not be that easy. These are very specialised areas. We won’t buy a company for revenues. Sometimes, when we examine a company, we may like the company, but we don’t like the (asking) price. If we like the price, there is something in the company that you don’t like at all. If both are okay, then you still have to look at the cultural aspect of whether it’s going to be a fit or not. So, as a small company, we have our own challenges of making acquisitions work. We’ve done a few in the past. The last one we did was in January 2011, more than four years ago. While we are keen on inorganic opportunities, everything has to be right. Organically itself we will grow easily by 18-20 per cent every year. The focus, however, is on profitable growth.

How has the slump in the clinical trial industry affected business? We are not witnessing a slump in the global clinical trials industry. On the contrary, we are seeing a surge. If this question is to specifically address the situation in India, we are currently not participating in the Indian clinical trials market. We are monitoring the developments closely and are well prepared to participate in the Indian market when the situation warrants it. In fact, we are very well branded in the Indian market due to our flagship software portfolio, PharmaReady, that enables regulatory document management, document and submission publishing (electronic and paper), submission registration, tracking, and management as well as other content management solutions. We have also been very busy implementing drug safety systems, CAPA, QMS, and Track & Trace systems for our customers in India and the region. We are well poised in mind and market share to partner with our customers in their clinical trials area when the opportunity resurfaces in India.

Are Indian companies and MNC pharma utilising pharmacovigilance services? Yes, it is mandatory for all companies without exception to be accountable for safety, adverse reactions or any other issue relating or subsequent to the launch of a drug. This accountability is a necessity and not an option.

What technologies do you see as futuristic in the areas that you serve?

We are already working on the next generation of cloud-based regulatory IT tools that will radically change the way regulatory information is managed in the next several years. Technologies that would help support data transparency and collaboration as well as predictive analytics will drive the future. Real world evidence and outcomes based treatments will increasingly become the norm, and there will be a surge in the design of new and novel clinical trials that will produce more effective and safe drugs and procedures aimed at personalised medicine. We are currently engaged in pilot exercises aimed at analysing Drug-ADR (Adverse Drug Reaction) co-occurences for a more effective and timely signal detection and management methodology. Upon scaling across several thousand drugs, this data could also be utilised for drug-drug interaction analysis, off-label usage of drugs, substance misuse, unmet clinical needs and better design of clinical trials and patient recruitment strategies and several more use cases. We are encouraged by the initial findings and hope to scale this platform using the Hadoop infrastructure and launch specific B2B and B2C solutions and services.

What role do you see technology providers such as yours playing in the life sciences industry in the future? What would/ does make you indispensable?

Navitas is not a mere technology company. It is a business enabler that has the ability to view the niche domain it operates in differently, thus delivering better outcomes for the pharma/ biotech industry in the form of lowered costs and faster time to market.

Thanks for sharing. Mr. Srinivasan explains it clearly and patiently.

Prashant and NDTV Team should try to do basic groundwork before they invite any management to their shows. Prashant asks the same stupid questions to every CXO that comes to the show - “What do you guys do? Can you explain to our viewers?” After that, he interrupts most of the time and repeats & writes down what the guest says. Prashant did the same to Mr. Poddar of Mayur Uniquoters sometime back. It’s not the best use of guest and viewers time.

If I understood the business correctly, big companies like Accenture , Cognizant, Parexel, Genpact competing in the same area(be it on the clinical development side or post drug approval side) how is TAKE solutions differentiating?

Though I agree that Prashant should be prepared better, I feel he is able to get the basics of business out from the guests very well. It is done in such a manner that even a layman(me included) can build his understanding.

I haven’t found any other series where businesses are better explained.

Biggies have their disadvantages too. They lose their agility over a period of time and here comes the advantages of smaller players like Take. Also big companies are seldom interested in projects of smaller size and duration. This gives the entry place for smaller vendors and once you have proven yourself well, opens up door for bigger contracts as well.

What I liked about “Take” is the special focus on domain where I have seen most of companies struggling. Plain vanilla IT services companies don’t have domain experience/expertise most of the times although they will claim to have so.

With the acquisition “Take” has strengthened and expanded it’s domain capability. Now we have to see how this flows to their topline and bottomeline.

Disc: Recently bought and is more than 5% of my portfolio.

Approved by CDISC or closely working with them. See the file attached and the names.

Accent , Oracle and Medi ( US based) - I dont see any other big IT names in this segment. Need to confirm.

Navitas - to bring in focussed approach and some big names are here.

Associated with top 10 pharma companies and one can correlate here Syngene ( CRO, read the latest AR 2015 and DRHP) to see the potential of the segment where Navitas is going to operate.

Now some anomalies which we dont find in a software company and we need to find answers.

Debt for working Capital. The Company has been in existence for so many years and still they have debts even for working capital. Long Term taken but paid off - not an issue. Why there is no sufficient cash built up ?

2.DSO 120 days - this explains the working capital loan but a negative for SW company. Any debt ST or LT is dangerous for a SW company.

Complicated Structure in place - cross holding, 4 subs for NAVITAS and others 12. It is better to be a simple structure like Infosys or TCS,etc.

Srinivasan does not hold shares and draws salary from sub. These things casts doubt as a simple investor find out reasoning behind all these complicated stuff.

We dont have much details as to whether acquisitions have paid off . Recent one WCI consulting taken for Rs190 crore and latest Ecron (Rs.115 cr)

5 Auditor is a small time auditor from Chennai and not a big 4.

Forex earned is shown as Rs 7.78mn. Am I making a mistake. Again complicated stuff due to structure.

Software Product cost are capitalised. Is it okay? What some of the product companies like Oracle, Polaris are doing?

During the year, a subsidiary APA Engineering Private Limited, India increased its holdings in RPC Power India Private Limited, India from 25% to 100%. Is there any Shriram Group angle to this. What Take has to do with a power company.

Dont know whether a single 1 mln. client is there as the info is not disclosed. One mln. clients are prestigious for a software company.

My analysis says they are not making money in the Supply Chain ( 50% of the business) as it is a very competitive and crowded vertical and they are moving into Life Sciences to compensate for the loss. SCM revenue de-growth of -35%, very high for a software company.

This is an interesting company going through tough times. While in the process of reading about it, I remembered that it was researched by an independent research site (masters of equity) who had recommended it in April 2009. They later closed the call. While I cannot attach the report, I will present a summary of their analysis which would help in getting a perspective about the company’s history. All the data is as of April 2009. In my next post I will summarise their reason for closing the call in June 2014.

Background:

Headquartered in Chennai

Presence in 9 countries and caters to more than 150 customers.

Incorporated in 2000,

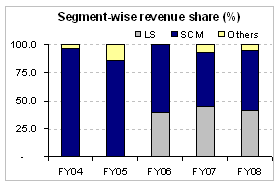

Two verticals – Supply Chain Management (SCM) and Life Sciences (LS).

In 2008 54% business was from SCM and 41% from LS.

16 active products in the SCM, which are housed under the OneSCM suite,

6 products in LS under the OneClinical suite.

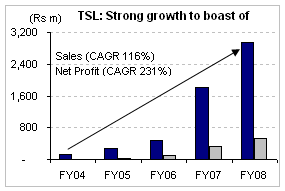

From FY04 to FY08, company grew sales and profits at average annual rates of around 116% and 230% respectively.

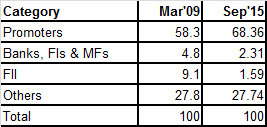

Shareholding:

No. of shares remain the same at 122.4 million, no dilution.

Employees:

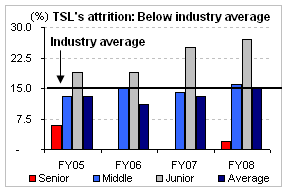

21% of the company’s total employee strength is domain experts - PhDs, doctors and supply chain industry experts.

The average attrition rate for the company during last four year has been 13% which is lower that the industry average of 15%. The company has been able to retain 20 key management people who have been there since inception.

Key management

Mr. Ram Yeleswarapu (President and CEO) - experience of over 15 years in both startup ventures and fortune 100 businesses. He is a co-founder of clinMetrics. Engineer from IIT Chennai.

Mr. S. Sridharan (Managing Director) has 15 years of experience in the IT industry. In 1990 he started company named Megatrend and established it as a leading IT infrastructure company, in 1996 he started Surf India a Web Solution company. In 2000 he launched iStartWeb, an intellectual property oriented software. Engineer from PSG College of Technology, Coimbatore.

Mr. Devaki Venkataraman Ravi (Chief Financial Officer) is a co-founder of TSL. 19 years of work experience in the IT industry. Post graduate in management from the Institute of Rural Management, Anand.

Business:

In SCM (54% of sales), the company has marquee customers like Xerox, Sun Microsystems, Siemens, Alcoa, Allergen, Biogen Idec, CavinCare, Parle, and ITC.

In LS (41% of sales), TSL provides software products and services which help in time and cost reduction in the drug development process. The LS space is highly regulated by the USFDA and is subject to various laws and regulations from state and local laws. The company is catering to these needs by providing product suites that comprehensively addresses regulatory issues in document management system (DMS), records management system (TRMS), structured product labeling (SPL), and the web version of the common technical document (eCTD).

Recently, various regulatory authorities, pharmaceutical companies and IT firms have formed a consortium known as Clinical Data Interchange Standards Consortium (CDISC). TSL is the only Indian IT firm to be a part of this consortium, which has developed platform-independent data standards that will enable information system interoperability to improve medical research and health care industry. Given that the submission of documents will be made in a particular format, the need for products and solution provider will be huge going forward.

History of acquisitions – to fill domain gaps:

2002 - Millennium Infocomm, a Microsoft partner that was developing software solutions in the logistics as well as financial services domain. 2003- company acquired divisions of iStart WebLimited and Metalogic Systems (India) Private Limited (again SCM domain). 2004 - TSL forayed into LS vertical and acquired the US-based clinMetrics. This company was assisting life science companies on decision making process in drug development through data inputs. TSL cross-sold its TAKE RTE (real time enterprise enabler) solution to clinMetrics’ clients in the pharmaceutical industry. 2006 - 100% stake in Onsphere Corporation (regulatory application software in the LS vertical), 51% stake in Applied Clinical Intelligence LLC (clinical data management) and 58% in Autopartsasia Private Limited in India.

All acquired companies have been profitable, and TSL has paid on an average not more than 1 times sales for any of these acquisitions.

Industry Prospects

Supply Chain Management: As per ARC Advisory Group, the SCM market is expected to grow at a CAGR of 9.9% to touch US$ 7.4 bn by 2011. Not giving details here as it is being exited.

Life Sciences: The global bio-pharmaceutical R&D spending is estimated to be US$ 172 bn, growing at a compounded annual rate of 18%. Out of this, outsourced work amounts to US$ 30 bn per year, while the clinical and regulatory spends are around US$ 7 bn.

Life sciences companies survive on innovation and launching new and effective forms of medicines wihc involves constant research and development and regulatory compliance. The drug discovery process is very tedious, time consuming and complex. An average successful drug takes over 15 years and costs nearly about US$ 900 m to bring to the market.

Therefore IT plays a role in bringing efficiencies in drug discovery and development. IT is used for drug tracking and monitoring regulations, stimulating the new drug pipeline flow, clinical trials, and document management.

Financials:

Sales have grown at CAGR of 116% over the past four years and profits at 231%. Average operating margins are 23% and average return on invested capital during last four years is 30%.

TSL’s P/E on its earnings of the past four quarters currently stands at around 5 times.

It would not be right on my part to share any projections that they had made or their targets. But I can say that the company fell short on revenues front by a little bit, and on profits by a large margin.

In April 2009 the stock price was Rs 27. Over the next 5 years it went nowhere reaching only Rs 35 (28% point to point return).

The company’s financial performance in last 5 years was disappointing. While the company’s topline growth was decent, intense competition in its main business segment SCM impacted margins and net profits. Global giants in the FMCG and Retail industries revamped their supply chain networks post the recession of 2009. Take Solutions was unable to meet the need for new software solutions required by the revamped SCM networks. The clients were unwilling to renew their contracts under the old software. Over last four years, the company had to write down 140 crores of investments made in the software products that it had developed for the SCM space. Also, the ramp up in the LS vertical was not progressing as planned with muted growth of only 6% YoY in FY14. The management expects the tough times to continue for the next 1-2 years.

Believing that the present situation would not improve soon because the company had not completed the winding down of its legacy SCM business and the LS vertical was not poised for any spectacular growth, plus also due to valuation concerns, declining short term profitability combined with an uncertain long term future, they announced to sell at current levels.

The bet is on the life sciences business where company has started focusing on. SCM is getting smaller by every passing quarter.

While reading their AR for FY2015, one interesting thing I found that they got several awards in 2015 for best employment practices. I feel they are getting their acts together and got their niche. However, we still need to watch carefully on how things pan out for them. http://www.employerbrandingawards.com/award-winner-2015.html#

The business appears attractive – its in a Peter Lynch kind of mould. Focus on the backend of a sector that will always be in demand, is recession proof and keep growing (Pharma). Make a niche for yourself, make your services indispensable for your customer, and keep milking him. I think all would agree on this.

Therefore let me do what is very easy, that is, question. Lets add to the negatives already mentioned above. There are the following key points according to me:

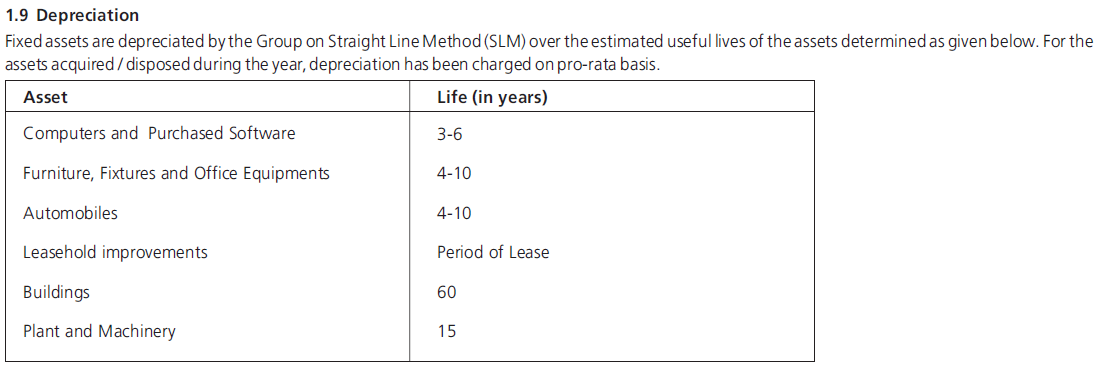

Consolidation of accounts – there are many subsidiaries and step-down subsidiaries in the consolidated financials. This gives rise to scope for aggressive accounting (not saying this is happening). Are the current auditors adept at handling such complicated accounting, and if required, putting their foot down with the management? Just an eg where the building is being depreciated over 60 years, which is too long. The figure may not be material, but the principle is.

Goodwill accounting – As on Sep’15, goodwill forms 31.5% of the networth. Goodwill is 188cr, networth is 597cr and H1-FY16 PAT is 65cr. Is the accounting treatment fair? Is it being amortised at prudent rates? Are impairments being recognized early? A large impairment could have detrimental impact on the profits. I have been bitten by the Opto Circuits bug in the past and hence am a bit wary of acquisitive companies. Which is why I gave a pass to Motherson Sumi as well, albeit, much to my chagrin. But this could very well be a personal bias.

Receivables turnover has been dropping since 2011 to 2015 being 5.9, 5.3, 4.3, 3.6, 3.1. It marginally improved to 3.53 as of Sep’15 (annualized). Are receivables so high in this business or is the company giving higher credit period in return for charging higher and improving profit margins? Which is their stated aim – focus on profitability.

EBIDTA margins for LS for H1-FY16 are 24.1% as per company’s press release. The management had earlier stated that EBIDTA in this line was 25-26%. Going by this, there does not seem to be much scope for improvement here. Yes, what can happen is that the company acquires another company with lower EBIDTA margin, which bumps sales growth, and then works on improving its margins all over again. The recent acquisition seems to be of this nature.

Lastly on valuation - The company has stated that they would be able to grow at 20% organically. A 20% grower, with close to peak margins is trading at 23-24x TTM PE, which appears fair.

I am also trying to find answers to the above, subject to which I find this a very interesting investment idea for the moment.

The business of LS ( not SCM) definitely is attractive but the key here how the Company is going to be successful in extracting the outsourcing from the top pharma majors. Some more points

On the strength of the considerable intelligence gathered, TAKE made the strategic decision of limiting its SCM activities to profitable segments while capitalizing on the growth potential of the LS industry and its USD 1.23 trillion Pharma & USD 289 billion Biotech markets.

SCM from Rs 166 cr in 2009 to Rs 212 cr in 212 ( CAGR 5%) and LS from Rs 156 cr to Rs 475 cr in 2015 ( CAGR 20%). 20% is a very god sign.

Life Sciences R&D spending is projected to grow 2.4 % per year from 2013 to 2020, reaching $162 billion.

TAKE Solutions’ Clinical Accelerators to reduce the time taken to standardize clinical trial data by over 50% (when compared to standardization without the accelerators), thus reducing time to market.

Experts joining LS vertical.

Source : Company AR

Depreciation is 30 yrs as Schedule II but I dont know the logic behind for 60 years. This is first time I am seeing a dep rate exceeding a rate as per Schedule II.

Ashish Dawan ( > 5% shareholder)has take an exit . he is from Chrysalis capital.

Working Capital requirement is huge and is consuming most of the operating CF. Further, CF is negative if you consider FA, Product Development and Goodwill.

They have intangible assets of Rs 100 cr and Rs 187 cr as Goodwill. Anyway, this can be ignored as it is accounting only. But on cashflow basis point no 3 is important.

Future potential is good provided we get improvement on 1) Cross Holdings 2) DSO 3) how they are going to tackle unattractive SCM 4) CF improvement from WC and Product development. FA and Goodwill, I am ignoring for the time being. 5)More details on how they are doing on acquisitions.

Software product cos. have habit of acquiring research at inflated prices and Take Soln. is no different. Capital allocation has been poor in the past. They took debt to acquire assets which did not yield good enough results and hence debt never really came down. Someone compared FY11 and FY15 profits and it appears that they have stagnated. In reality, EBITDA has grown in line with sales but accelerating depreciation (and amortisation?) has kept PAT in check. I haven’t done study on why its recent acquisition should work.