Let’s say the story holds and over the next 2 years::: Revenues continue to increase. Pipeline remains strong. Couple more acquisitions. Ok ok bottom line.

Stock languishes.

Should one continue to hold? Would you? What if it is 4 years instead of 2?

PS: Mridul, much as it looks like i am trying to push you, i am trying to push myself. Thanks for engaging in the discussion!

All i will say is - I can stay passive for long if i believe in the stock story. I am still making ~15-16% by positionally trading this 4-5 times while this is range-bound. We need to minimize our opportunity cost while at the same time stay patient with stories where we believe market is mispricing for some reason.

My initial investment here was done sometime around April '17.

Just read entire thread from beginning and its been a great learning experience! Thanks @crazymama@rajpanda@Donald and others for your valuable contribution, its truly amazing to see how constructive this forum can be!!

Coming to TAKE, I came across this stock while screening out companies where promoters have been buyers over last year. Promoter’s stake has increased by about 3% in last quarter.

@crazymama@raj1968@rajpanda I am wondering what are your views on TAKE now that it has been quite some time of EA acquisition and the stock has been seeing some traction lately?

I have been holding this for last 4 years and building more position(s) every two years.

Pain:

Dilution of equity. There was no real need for dilution, as I see it. Reasoning including the one in the recent call was limited.

Price fluctuation does make most sensible analysts wonder.

Tax rate, clearly company is benefiting from lower tax rates and the benefit seems to have abated.

Clinical focus great, but last insight on the same (TV interview) suggested 25% clinical revenue of 70-80% LS… this did not match with my analysis back then (do not have the numbers handy).

Spending on EY’s to help energise team/ make gladiators could point to lack of organic motivators (key for small caps and start ups)

Large focus on Ram Y … what if he resigns, does company management have replacement in place.

Marketing offensive of the stock does not seem to be creating real traction as yet… need proof via FPI or DII or HNI holding increase.

Have not liked debt holding over last 4 years in USD, as it was obvious the Rupee was stable. This along with dilution at wrong times make me wonder of the capability - finance team.

HR Srinivasan held SCM close to his heart, is this one reason he has not been able to sell the business earlier.

MD’s handling on concall has been best among the team, but limited when robustly challenged. At times it is important to give investors confidence not by pointing positives, but accepting honest mistakes and learning from it.

MD on BTV recently was lured again in stating they could sell SCM by H1 of this FY. He had on the concall and all places managed to accept the mistake by not stating deal closure time… this tells me two things… he cannot control his emotions (surely better than mine and many others) … one cannot trust his statements (this is a bigger pain). https://www.youtube.com/watch?v=_GJlOMMMriQ&t=3s

As the business grows there will need to be a change in top management and this I feel can be a sticking point … given promoters strong hold on the firm…

Promoter seems to have strings tightly held for my liking.

Having said all the above I still hold my position(s) and will continue atleast for next 2 years (22-25% y-o-y sales growth). Expecting bottom line to soon perform as well as the top line once SCM is negligible.

Over the last 4 years stock has still given me >25% compounded return. My expectations were more like ~30%…

Trading position: I am not adding at these levels.

Investment position: My fair value 250-260. [Hold].

Short term targets 280-300 (purely momentum driven).

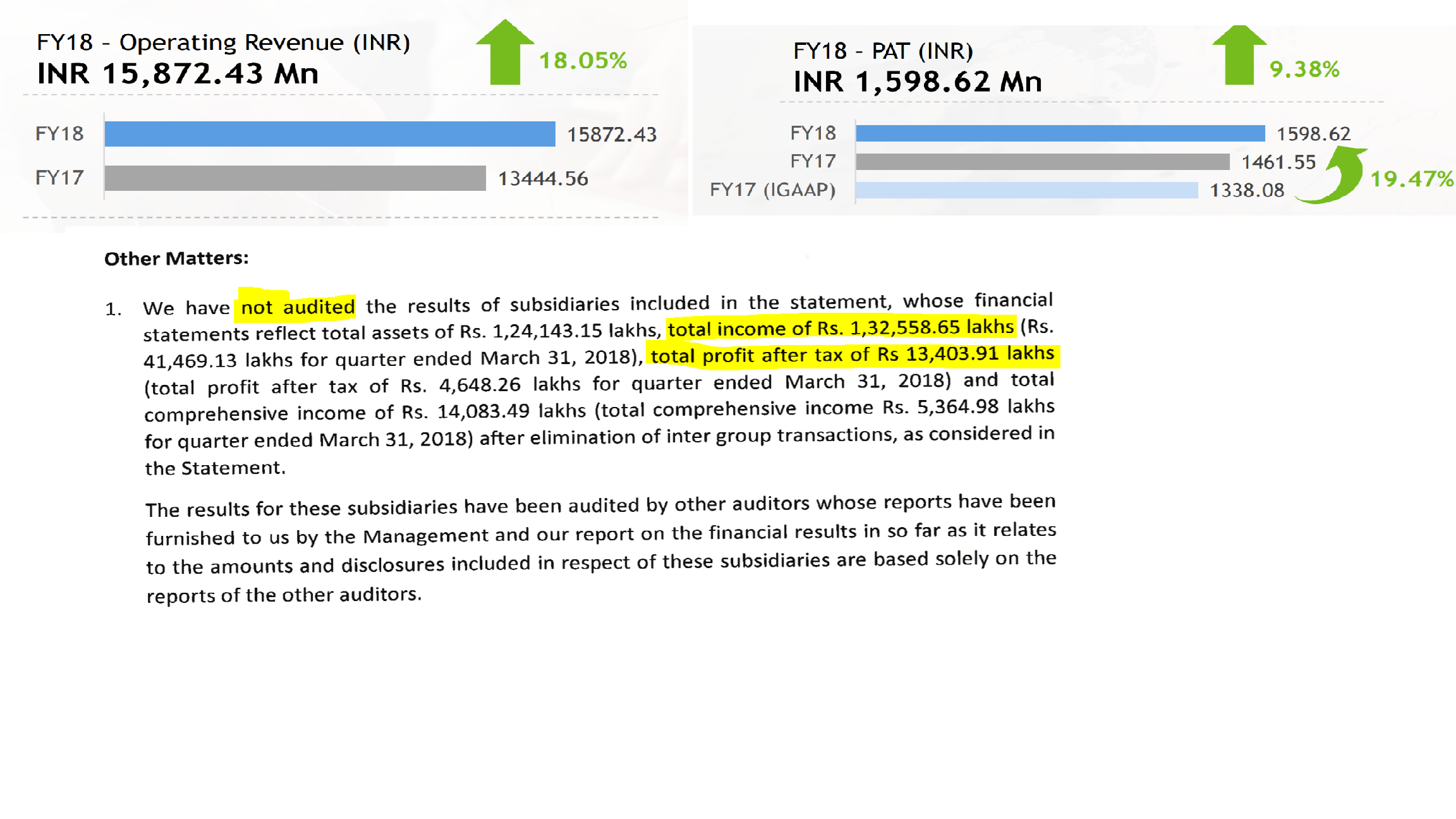

TAKE SOLUTION LTD

Highlights of Q4FY18 and FY18 annual results

Financials

Q4FY18

o Revenue for the quarter stood at Rs 454 Cr

o PAT with minority interest stood at Rs 46 Cr

o Growth rate for the quarter QoQ has been 11.25 % and YOY has been close to 28 %

FY18

o Revenue stood at Rs 1587 Cr which in rupee terms up 18 % YOY and in dollar terms up 22.8% yoy

o It was primarily driven by Life science business. It is showing compounded annual growth of over 30 % over the last three years and 8.37 % from last 12 quarters

o Order book stands at 189.36 million out of which 179.46 million is from life science which has grown 30 % YOY and 26 % YOY.

Business Highlights

o Company have become the preferred CRO products for two leading biopharmaceutical companies during the quarter.

o Also awarded three studies in the growth areas of biosimilars and stem cell therapy, both these are high growth areas and company continue to capitalize strong position in these

o Other pleasing development was the award of three Phase III studies cutting across Europe and Asia.

o For r pharmacovigilance service given a multi year , multi-geography annuity contract, which is very substantial in value.

o Company also supported d four global pharma companies to comply with the U.S. Drug Supply Chain Security Act and the EU Falsified Medicines Directives

o Company is developing complex molecules and some complex methodologies in area of asthma and diabetes .

o Working on biosimilar opportunities and , these are in the areas of the monoclonal antibodies being used to treat rare indications like rheumatoid arthritis, spot psoriasis and some rare indications of cancer where company pipeline is growing substantially

o Company is looking to expand into the areas of biosimilar/ bio-analytics

o Company offer three core offering

Core service offerings

Set of technical solution

Consulting

o Digital R&D will reshape the world of clinical trials for the future

o Company is also looking to fetching up data from electronic health records and medical records. In this scenario a physician is actually prescribing to a patient, and the symptoms and the prescriptions are being captured in the EHRs and EMRs along with the medical conditions . Company will be investing in one clinical platform.

o Company have capabilities in the areas of servicing to customers in PV services. For example company have added a team of almost 25 post-marketing safety experts. Company will add more customer in service offering.

o In multi products like pharmaREADY, traceREADY, labelREADYand safetyREADY products . Company have continue to invest and grow these platforms. Company have stuck various strategic partnerships with companies like Sparta Systems and a few others like rfxcel and with these partnerships company target is to really integrate company software platform with some of strategic partnerships and over the partner software and company

o In Subject matter experts , company added half a dozen medically trained professionals for performing medical reviews and medical monitoring activities. Company goal is to switch very soon on platform driven set of services, medical monitoring and medical review services, and a whole host of other services and eventual goal is to render annuity services for each of company customers using company own technology platform and preferred partnership methodology is the right way to go forward and adding this preferred partnership over the next couple of years

o In area of supply chain company was able to divest in middle east

Q&A

What is the item in annual report s stands for “Unearned revenue” and in presentation “noncash capex” and explain on tax rate which is much higher in the quarter ?

o First is unbilled revenue not unearned revenue , unbilled revenue means that revenue has still not moved to debtors , it means service is delivered just invoice is pending so it is on a time-effort basis where you estimate and do it, it is a standard practice, but it is not a very large portion of the total revenue. It can be sub to 2 %

o Noncash is the actual depreciation and amortisation which is part of total expense is Rs 104 Cr that has gone to the P&L

o On tax rate company is looking for 15 % or below.

Describe the sales cycle of company ? Describe a bit more on machine learning and competency in artificial intelligence and machine learning ?

o Sales Cycle – Most of sales are repeat almost 90 % are repeat customers . most of it are MSAs that company operate so company have a very sticky outlook. Company had added more then 22-23 customers during the course of the last financial year.

o In functional services and in the Phase I and II trial segment small and mid-pharma seem to be occupy very strong space so there is a slight decline concentration from 31 % to 25 % the top 10.

o In terms of consumption of the order book of $189 million typically it will between 7 and 9 months to consume it.

o The order book is the accumulation of all the SOWs or statement of work that company receive, but actual visibility that into orders is much higher. It is almost about 2.5 times what is stated in the order book, but since the order book is an accounting document company need a customer confirmation in the form of SOW, which is what company cumulate and present as an order book in the public domain but from a management visibility it is 2.5 times so the momentum of growth looks robust.

What steps company is taking toward 5-year 5x growth plan and how important acquisitions are and what segments or areas company is looking at ?

o There are two component in 5-year growth plan.

The organic component is growing at about 24%, 25% CAGR

Second is inorganic component where there is M&A in clinical space in US geography and certain niche technologies that can make an order of magnitude difference to either the time or the cost as far as the pharma R&D process is concerned.

Is the margins from last two quarter is sustainable or it can move up ?

o Margin for the current quarter stood at 19.9 % which is about 0.6 % over the previous quarter. These margins looks to be stable

What is driving the clinical side of business and what is the outlook on that side ?

o On clinical side company is generating growth in the areas where many of the customers who are historically looking at just BA/BE studies or looking at the patient PK studies, which are from a material perspective larger contracts. They are higher revenue generators for the customers. More focused on PF patient studies .

o There has been increase in volume in the innovator companies which are driving a lot more Phase II, Phase III and Phase IV studies. also customers fundamentally sensing the need to do most post-marketed safety or efficacy studies. So overall .there has been an increase in volume of the number of clinical trials being conducted.

o So one parameter is clearly the growth in volume, a patient PK study by the pure generics; two, the number of Phase II, III and Phase IV studies also going up in volume. The second dimension is across what therapeutic areas or indications and company of 18 different therapeutic areas and some of these are in leading areas where indications like oncology, cardiovascular, ophthalmology, so on and so forth, which are some of the high investment areas that are happened. So company is looking steadily and actually building a robust pipeline as an order book on the back of very strong expertise and running clinical trials for a variety of different companies.

o In Biosimilar , it work in term of regulatory requirements is they need a Phase I study and a Phase III study…

o So company see strong growth in patient PK, number one, number two, the typical Phase II, III and IV from innovator companies and the third bucket is the Phase III for biosimilar. Company is also adding new Logos.

o Even on the innovator side, there is increasing demand for post-approval support, regulatory publishing, whether it is document publishing or submission publishing or labeling and artwork management, track & trace and serialization, so there is a number of these areas that are demanding attention, all because of two factors. One, a demand for regulators for enhanced compliance and adherence to these kinds of regulations that are falling in place. Number two it would be a consolidation and an aggregation of the demand at the customer end and they are fundamentally looking for a vendor partner who understands this business extremely well and can conduct their business of post-approval support on the regulatory & PV side very efficiently. So on the regulatory, two drivers of growth, one is regulatory push, a new regulation in markets like U.S. and Europe, the second is an initiative where they are trying to advocate that demand at their end and looking for a vendor partner that they can potentially outsource to.

Does company is confident to maintain the same level of growth for both clinical and regulatory in FY2019 ?

o Yes

How will be the depreciation and amortization look forward ?

o It is about 6.5 % of revenue and it will be at same level.

What is the outlook on SCM business ?

o It will become 10 % of business from 12 % currently but company is making efforts to sell the remaining portions of the business and hopefully something will be moving there

What could be the growth going forward on full year basis ?

o On higher volume and given the execution capacity it may be closer to 24 % in life science. But company is adjusting for any potential degrowth that may happen on the supply chain side and that is why company hope the weighted average between 22-25 %.

Is there any fallout in terms of some of the deals or there is change in valuation because some of things are not playing out in FY2019 as mentioned so what are the major changes company is seeing ?

o At some time company had seen that e synergy value is not commensurate the monetary value company is paying so company have to revisit the acquisition

o There is nothing in a mature stage and currently company is in discussion with half a dozen of companies. Company is actively looking at acquisition which create value

Why was dilution of equity done in so much rush manner ?

o Company have to be ready for acquisition where currency is required because company have to prove itself for an acquisition so company have to dilute it .

Does CAPEX investment will be done behind CRO ?

o Yes and it also include physical expansions that have taken place in about five offices: in Frankfurt, in Berlin, in Princeton, in Bogota in Colombia. There has been a Chennai facility. There has been a Bangalore expansion. So now company will expand the facility and add clinical facilities and also adding equipment. There are lab equipment and LCMS/MS machines, ICP-MS machines, and these are all expensive machines that come in for analysing samples.

o Capex will be in context of growth rate overall

o In non-cash it will be 6-6.5 % of revenue . In hard infrastructure it would be 3-3.5 % of revenue. And that would largely be addition to facilities, addition to lab equipment and addition to some of these certifications, which go along with the lab equipment and the audited facilities, the audited data centers.

Are there any one off expenses going ahead or other expenses that keeps growing QOQ ?

o There are no one of expense . Company is anticipating a lot of addition to the management band with a few more people joining at senior level in US and Europe and continue to expand business. SO there may be capacity build of people ahead of demand. If it doesn’t happen then EBITDA will improve

Why has debt grown up in spite of equity infusion ?

o There was a debt program initiated at the beginning of year and that are all long term debt with a 5-year circle . So the equity, which was infused for a specific end user of acquisition and definitely is not going towards working capital of the existing business.

o The debt are at coupon of about 5 %. They are overseas loan not rupee debt and they cannot be paid off by issuing equity.

At what senior level does company is going to add people in US ?

o At Clinical head or Global QA head and company has hired both

o Company has also hired a new global head of marketing who is already onboarded . Company have taken expert positions like regulatory information management specialists. Company have been looking at a PD thought leader.

o As US geography is growing so fast so company may add a North America sales head for which again discussion are going on.

Thanks. Lifescience strategy seems to be heading in the right direction. And luckily for people invested, market finally seems to be recognizing it

The addition of new client logos is a good positive. Given the slight ‘product’ oriented nature of the business, I would have expected margins to go up more than what’s being indicated

I did some basic digging around take as a fun exercise and found some concerns which warrant digging further.

not able to reconcile employee productivity with the usual industry metrices.

i also checked statutory payments - esp EPF and it makes no sense given the number of employees. A good thumb rule I have is about 1500-18000 employees on linked in for every 1000 cr. of revenue (average productivity is about Rs. 30-45 lakhs for best in class - usually 25-30 on median). When I add up all the employees of take it comes to only about 1200-1300 employees. Also, i am not able to see many on the sales/pre-sales side. I try and use some of these checks to triangulate it with comparable sized competitors. since this is IT services, about 70-80% of employees are usually are on LL, I also use glassdoor, # of jobs advertised etc. to triangulate this.

tax rates are much lower than 15 %

the indian entity is continuously being stripped of value. if all this cash was raised in the indian entity, it makese no sense that revenues and profits plummet in it. it beats the offshoring paradigm itself.I find this extremely strange

-company keeps diluting - qip in 2016, pref in 2017, for an IT services company why do they need so much cash in ? and hows the promoter who is a first generation entrepreneur bringing in cash from overseas ?

does anyone have a view on how many employees they have across entities ? i could not find it from AR. my concerns are around the org structure making no sense (# of employees, # of emplyees in USA/sales/pre-sales), high receivables, indian entity being squeezed out, repeated dilution and stretched cash flows.

Fair enough. Couldn’t find the latest annual report, or the employee count. As i have noted before, i have yet failed to understand how much revenues come in from “products” vis-a-vis “services”. A higher component from specialized products would justify higher $ realization per employee.

I would also be wary of comparing Take to any other IT services firm. Professionally, i have been involved very very briefly in executing a project with a clinical pharma team, and i can definitely say it needs specialized knowledge just to understand what your client wants!

While trying to find the annual report,

i came across the auditor statement and it’s quite weird that they DON’T audit around 80% of the company

The q4 earnings call transcript is quite interesting. Link: http://www.takesolutions.com/images/financial/take-sebi-qtr_4_transcript-2017-18.pdf

2.1) CFO wasn’t able to answer some questions around capex convincingly, and it looks like Srinivasan is the one calling the shots on capital allocation.

2.2) Management is confident of having tax rates around 15%

2.3) I am guessing the presence in sales/pre-sales will increase after they get the senior hire ‘Head of Marketing’

My investment reasons continue to hold:: (i) niche in their work, validated by growing life science revenue, and healthy order book). (ii) good opportunity size, enhanced by acquisitions that help them move across the value chain. Based on these two, I see Take being a steady compounder for at around 5-yrs.

That said, i suck at financial analysis. Thanks for bringing these points up and giving a diff perspective.

This company is transforming itself from an IT products/services company to a company offering niche services in the space of Regulatory, Phamcovigilance, Clinical services to Life sciences industry using Digital Technology. It also offers access to Life sciences company to the Digital Technology for their inhouse needs. Outsourcing today has moved beyond cost savings to a Strategic choice for many companies and this company is trying to create a space in this area. The company belongs to the Shri Ram group

You should re read the Annual Reports to figure out if you still want to look at this company as an IT company or a company that is transforming itself in to a Outsourced service provider in Niche Life Sciences space using Digital Transformation technology.

My view is that readng and re-reading AR’s is one part of investing. A part that is often ignored and underestimated to see if the data points that flow from AR triangulate with those in the real world. I am not able to see a connect on number of employees and revenues. Given the shrinking revenues india, repeated dilution.low cash flows and multiple subsidiaries that are not audited by the indian auditor, I see plenty to think about. Does not mean its wrong or right, it just requires some more thinking through.

Well noted.

It would be worth checking with the firm (investor relations) how its subsidiaries are audited. There is a need for audit in the US and EU markets for subsidiaries.

Or one could use database like ORBIS to check for their submissions. British Library could give you free access to some of these databases.

In terms of rupee term company grow by 3 % and in dollar term short by 0.7 %.

Company has converted 37 % of Order book as revenues

Company expect 22-23 % of organic growth during the year.

EBITDA margin stands at 20 % compare to 18 % last year same quarter and it is sustainable going forward.

Revenue grew by 37 % YOY.

EBITDA margin YOY grew by 41 %. In rupee terms

PAT grew by 54 % YOY at 54.2 Cr or 8.1 Mn dollars.

Key Highlights

Company is now looking at expanding in Clinical and Generic vertical . Also trying to gain footfall into the US market.

Company is in talk with many companies and confident to start dealing with one of them in near future.

Company has expanded its facility both in Trinston and Bangalore.

Company also had an inspection from FDA recently and there has been no observation left.

Company has close to an order book of 200 Mn.

BAB Generic pharma has become full service offering for the company and does include now data standardization for US FDA requirement.

Company is in the process of going digital and currently it is in stage of inspectional studies and entire focus is on digitalization and automation.

Company is focusing to become Global forum and for that company is meeting its existing customer as well as new customer. Company is also in talk with number of companies for cross selling. Company is expecting lot of orders on BVC technology and upgrades.

In Pharma company is getting big customers. Going forward company will gain more market share. Company is also developing mathematical models.

Company is also expanding in fingerprint.

Adding process on the clinical trial vertical. Company quest is to digitally transform own business and company is also developing strategically partnership.

Forum in Mumbai is continuing to get attraction. Company is also inaugurating 2 new forums.

Several Domain experts have been added to company global team. Company marketing , production and all other teams are strengthened in existing capabilities. Company is also adding scientific capability in Europe and company is getting the value for this recognition.

Q&A

Kindly give quantify outlook for next 3 years ?

In M&A company had done a raise capital and company is now very bullish on this and there could be a transaction in the next few months and that would add to the Inorganic Growth. Comparing the order book and FY17 Q1 results the revenue conversion was about 45% plus of the order book and in Q1 FY18 the revenue conversion was about 39 % in march and now it is 37 %. So this show the strength of multi year deal that company have been growing. So the order book is growing and revenue conversion rate is coming down yet the revenue is growing. It means that the multi year deal is strengthening in the overall pipeline order book.

The capability in Clinical trial is complex and not predictable so company is very much comfortable with 22-23 % of organic growth rate. It could be higher but that would depend on when company convert the order book. From current order book and longevity company believe 22-23 % is a good number.

Kindly explain the GAP concept in US and M&A explanation of acquisition ?

In M&A company focus is on EPS lucrative and therefore company will take time and do sufficient diligence and company approach is not going to change in any manner.

GAP is created in the mid-market space and now the small pharma company are been under serve because they don’t have that much capability to do business with the large one is missing and company is happy to absorb all the capacity so company is on the right kind . Company is going to leverage centralized clinical area to cut down the cost.

Kindly split the order book in segment ?

Life sciences is 190.21 Cr and SGM is 9.53 Cr.

Does company see increase in order size ?

Company conversion rate to order book has come down from 46-47 % in FY17 to 37 % now that reflect that company is getting larger and multiyear deal with clinical function included in that. So clinical deal will be in 8-10 million and technology deal in half million. The range would be 500K-10Mn . The 190 Mn of order book is SOW and visibility will be 3X of current order size.

Did the 10Mn range is part of current order book or visibility ?

That will be visibility.

Kindly give brief on the profitability on the Clinical versus regularity and PV segment ?

Overall Clinical EBITDA margin would be lower than the Regularity and PV. But it has attract the higher spend. So the clinical EBITDA margins would be in mid deal where the regularity and AMT margin will be upward in range of 23 %. So that is how to interpret.

Does the clinical segment will grow faster than other segment ? And does it will create pressure to move margins to 20-21 % ?

Yes

On weighted average yes the margin can see a pressure but look at the context of the market that for every dollar spends 70 cents is spend on the clinical and if one not remain relevant in the clinical so push out of it to drag and safety. If one need long multiyear tenure deal than clinical have to be part of it.

Can clinical margins go up as company scale go up in this segment ?

Margins will definitely go up it all depend on the use of technology not only scale. So company is reducing the person and moving toward automation. So margins will get push up with usage of lot of technology. As company moves and gain volume this margin will gain to 20 % range.

What does the equity raise of funds pertain to ?

That is just an enabling provision. For a company with high growth and it is just an enabling provision it doesn’t mean that company will act on it. This resolution is taken from last 10 AGM.

What could be the ball park range of acquisition amount ?

Company is not at that stage that company can reflect the numbers. All of them are not in the same type of business. One could be in services , technology platform, and they all operate with different numbers. The current revenue range company is looking is anywhere between 25-30 Mn in revenue terms. That is where the target range is currently.

Would the fresh 250 Cr of raise of funds will be sufficient to fund the acquisition ?

Company current cash balance and if require any than currently company is very underleverage so even is any additional is needed in terms of growth capital than Company will go for leverage and not to raise equity.

On depreciation 33 Cr per quarter is sustainable going forward ? Kindly bifurcate between tangible and intangible assets ?

Company have plan for this much only and company do expect not more than last year. Depreciation consist of 50 % tangible asset and 50 % intangible assets ?

What does it mean by consolidation going on in M&A ?

It is an industry picture in which larger company is looking to consolidate from size and they are also trying to get technology capabilities because only size base consolidation is not helping them in case of margin improvement .

There are lot of technology companies which are adding CRO capacity to them. Also IT companies is trying to get capabilities which will be in the life sciences case. So it is actually at intersection of the life cycle companies such as company own technology company and there is a good mix of activity. Therefore the current valuation are little aggressive. Company need to be EPS lucrative as far as company can do the transaction. This is what happening in the technology , CRO side.

Is there is a separate schedule for Tangible and Intangible assets ?

Yes

The Indian pharma Companies are bottoming out so how does company itself in pharma segment ? How can the acquisition be deal out ?

On acquisition company cannot give time line and one has to look on valuations and discussion , look at the appropriateness of asset or look at the strength that company have to grow at the asset, look at the possibility of Integration for business and the ability to create revenue synergies. Acquisition for cost synergy does not help company have to create revenue synergy. This is slightly a complex strategy. And today company is looking for bunch of assets that look promising from revenue synergies.

In Generic pharma the competition is getting stiffer and stiffer and there is pressure on margin. Now Indian pharma companies are investing in Bio similar. So these are higher revenue opportunities for the pharma. Now large pharma companies have integrated strategies with Generic and Biosimilar equivalence to Biologic and mono stromal anti body for cancer treatment. So Indian pharma is evolving and company is working with number of pharma companies and that will probably grow.

Indian Pharma companies are seeing pricing pressure so how they will resolve it ?

They will solve it from technology and automation and reducing of labor . For that investments have also start happening.

What is the receivable days for the current quarter ?

Last quarter it was 99 days and now 110 days. So the Industry receivable days are between 90-120 days. But company want to more closer to 90 days.

What were the valuation that happen in the M&A in the recent past ?

On EBITDA basis transaction is 8 times to EBITDA to 18 times EBITDA. There has been transaction from 1 time sales to 4 times sales. Median cannot be defined as the types of buyers has been different. If the deal has been in with large companies than the valuation has been on high basis. If the deal has been in with smaller companied than the valuation has been on conservative side.

What will be the CAPEX this year and where it will be focused on ?

It will be more toward equipment and technology and not more than 110 Cr CAPEX.

Kindly brief the Other Income ?

It is from the investments both in term of back interest and dividends from Mutual Funds.

For the full year can ETR be expected in range of 16 % ?

Hi,

I have gone through the article in detail and find it erroneous in its conclusions.This company is being compared in the wrong sector of IT and ITES which it is not. I follow the company closely and I am aware of the services and clients that the company caters to. This company is sound to my knowledge and administers excellent governance policies.

They are basically comparing them with plain vanilla mid tier IT companies and saying figures(revenue per employee, salary per employee) are out of sync. Ideally Take should be compared with Life Sciences division of other companies doing similar work.

One good thing Moneylife team has done is after every point they have put management perspective as well.

Anybody who has followed the company knows all the points raised.

They have compared revenue per employee, cost per employee, receivables etc with IT companies which may not be ideal comparison. They have mentioned that they will be coming up with qualitative analysis of the company soon.