Cash flow from operations looks low… has anyone dug deeper there…

I have a lot of respect for Sucheta and Debashis.But here Debashis has erred by comparing Take with other software companies. How many software companies are in Life sciences in India and in the world or how many life sciences companies are in software

Take solutions has a 208 bed hospital spread over three locations to expedite research and provide solutions where the first to launch gets the moolah. How many software companies have self owned hospitals?

This article has created unwarranted panic in the market!

Good to note that TAKE Solutions has submitted a rejoinder to Money Life, copy of the original article from the exchanges below:

2 Likes

Does anybody have a view on

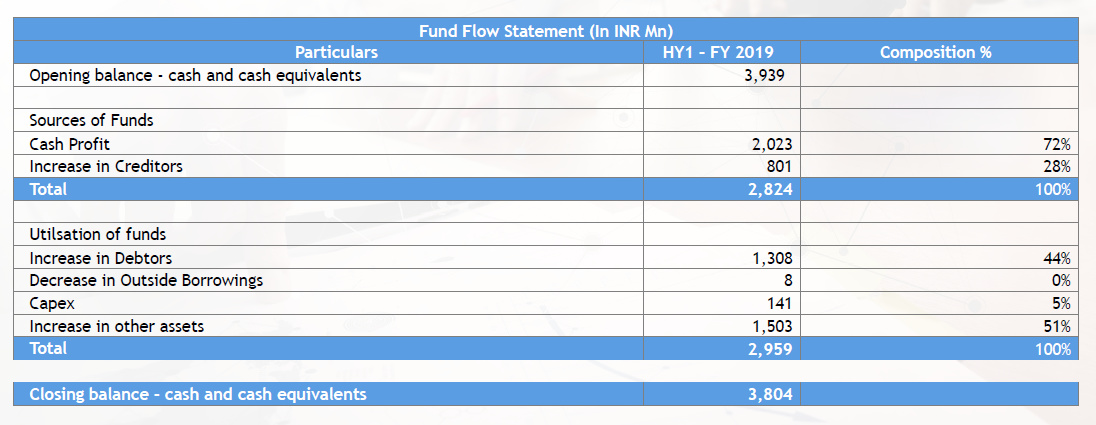

- Zero Cash Generation in Q3

- High increase in Other Current Asset. Seems like it is on account of unbilled revenue

- Payment of Interim Dividend despite no incremental cash generation

Will be worth debating if you can quantify the cash flow.Many make errors while doing the cash flow and hence this request.

Even if it is so, payment of dividend need not be synergistic to cash flows on periodic basis.They may follow different cycles

1 Like

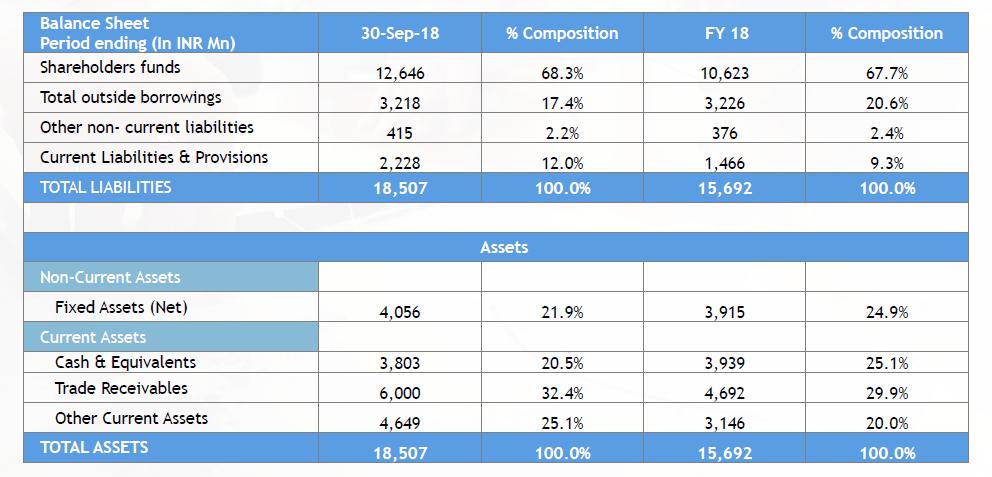

202 crores of cash profit completely utilized in increase in Debtors and Other Current Asset. Other Asset is not detailed but most probably pertains to Unbilled Revenue. Unbilled Revenue increase in too high. closing cash is lower than opening cash despite cash profits. Company will have to pay interim dividend from Opening cash balance which is mostly the capital raised from promoters. The business does not generate cash despite an impressive headline growth of +59% in H1 PAT. Trade receivable is a perfect number of 600 Crs. Seems Strange to have a perfect number.

1 Like

had cash been generated, it could have been used to profit from Financial leverage by reducing borrowing and interest cost.

1 Like

We have had a lot of red flags in this counter be it low cash flows, equity dilution, inorganic growth, etc. I tend to believe all these are already factored in the current stock price.

But my concern is that we have had instances where corporate governance issues were raised. This is also clearly evident from the thread. Apart from the fact that the company has a lot of subsidiaries and has been paying taxes at lower rates, do we see any other issues?

Trying to do a bit of qualitative analysis -

- As per the management, Shriram Group still owns a stake in the company. This does allay my fear significantly.

- Also, you have a profile on Srinivasan H R, who is the vice-chairman of Take Solutions, by IIM Calcutta. Although I am not sure whether IIMC is his alma mater.

Could someone who knows the company or management better please care to address this?

@crazymama Sir, not sure whether you still track this company but your contribution to this thread is awe-inspiring. Would love to know your opinion on this.

Disclosure: Invested

@varadharajanr, As company has replied recently with details to few of your earlier issues based on latest article by moneylife

Would like to hear your views on same.

Disclosure: I had sold of my position in late 2016 due to need for funds. However on restarting the investing pf, my previous convictions did not hold up on introspection.

My take on the situation is that it is a self-inflicted goal. IMHO, the rationale was always driven by a top-down narrative based on management commentary. I have not been able to do the per-unit economic analysis of their numbers nor can we do a comparable analysis with peers like Veeva or IQVIA (Quintiles & IMS Health).

If they wish to avoid these kind of recurring doubts they should be willing to provide more granular numbers to allow for comparison with Veeva or IQVIA. If not, we will continue to depend on mgmt commentary.

On the other hand, they seem to be capitalizing on the Regulatory front (FDA’s eCTD deadline)having taken 2 years to go from 100th to 150th PharmaReady customer base. However this is underwhelming when compared to Veeva over the same period.

Veeva have yet to tap into the Top 20 Pharma companies and are still to launch their Safety (PV) related vault application.

If PharmaReady is an excellent platform, then what is the need for a Knowledge partner (Consultant) to handhold a customer through a submission/filing?

While Take Solutions has put up a few videos explaining what they do, it is nothing new compared to what I had known 2 years back.

Compare it with the amount of info which can be tracked as key monitorables from Veeva

My opinions are from a viewpoint of a recovering diabetic who believes most drugs cause more iatrogenic harm since they try to treat a symptom or a specific pathway that often causes unintended consequences in a complex adaptive system such as a human body.

I would also recommend to read below 2 books to understand the way Pharma companies intentionally avoid publishing failed trials.

Follow the money and incentives.

Above scenario is a risk, CRO’s like Take will have to consider especially when they intend to take on Pharma startups. Onus will be on them to report everything even at the cost of losing a client. Can they do that or would they be entrenched with the status quo?

As a patient, I would prefer if my doctor first suggests me to subtract from my diet to see any benefits before pushing a pill (adding a new variable) to me.

Having said all of the above, Take will continue to make money as long as Big Pharma continue to treat symptoms, emphasize on relative risk rather than absolute risk leading to marginally better drugs.

5 Likes

Silent boarded here but a part of the industry having tracked this for a couple of years closely

I refuted all the Moneylife allegations in the comments section of the article twice (and so did another boarder). They were deleted twice by Moneylife. My mistake is I didn’t take a screenshot (I didn’t expect the crooks there to delete it twice). The Moneylife article is copy paste from allegations raised on this thread and was frankly nonsensical. Probably written to make money from owning a naked short on the stock by the writers

I think the way to think about it is as a CRO, which has 140 days debtors (industry has 100-120 days) and where the Lifescience IT business is also now cross sold with the clinical trials piece so also has similar debtor days as a result. If you want to look at peers, look at Parexel’s gross and net debtors from their last published AR in mid-2016. Gross debtor days are 145 and net ~120 days. Margins are 10-15%

These businesses are cross sold so a combined margin profile of ~15-16% is more realistic. You have to remove the amortization below EBITDA from the opex and also remove it from cash flow from investment outgo. They nearly match up. This is a mostly BA/BE Clinical trials company with some biosimilar phase 1-4 trials as well because of Ecron legacy in Europe. Very different from Syngene which only has a small clinical trials business but a larger pre-clinical trials business (testing on mice, contract research etc.) which is higher ROE in India. In India clinical trials is a hard business because you have to own your own hospital to run the trials well unlike in the West. Take has apparently acquired a 100 bed hospital in Chennai for this which is running at some 20-25% utilization. There is huge demand from China now requiring drugs to have trials on Asian populations from scratch for approvals now and not allowing trials on Westerners done 15-20 years ago for approval. So they’re riding this tailwind

What they should do is change the auditor to give some comfort (auditor apparently audits 90% of revs but doesn’t consolidate subsidiary audits) - why not pay more and get a big-4

Promoters can’t buy much more - they already own 68%. They probably don’t have money to delist - that’d need 1000cr or so to do I guess. If the stock stays here for 6-12 months my guess is they might decide to sell out. Some strategic guy might buy this at 8-10x clean EBITDA. That’s around 250 a share

2 Likes

Just interested to know,if you are in any way associated or were associated with this company. Do you see any redflags on the Management integrity. Are you comfortable with the reported numbers.

Not associated with company but own shares and have done checks with IQVIA, Novartis, GVK Bio, Freyr, Kinapse and other analysts whose funds own.

Hard to doubt integrity as they’re ex-Shriram guys. Would hope this is the jolt needed to be more transparent and move to a big-4 auditor as there is a lot of discretion in CRO company reporting. You can check with SYNEOS - CROs have been moved to a new accounting standard in the US as a result where there is less discretion. This company should probably just be taken private and listed in the US where this industry is better understood with many peers

I’ve also come to this thread after ~1 year - to post about my Moneylife responses being deleted. Medidata was one of the companies I’d looked as a peer a long time back as well but they’re like apples and oranges now. Medidata just sells a software product to CROs to help manage clinical trials. Take also partly used to do that, but realized that clinical trials companies were developing this in house / acquiring peers and would not go to them in the future for business. So they decided to get into the CRO business through Ecron

1 Like

Ok. Thanks for taking time out for your reply.

The thing that concerns is the quality of the numbers. Huge and growing requirement of working capital and lack of visibility of free cash flow. The Company growth appears impressive. The Size of opportunity looks impressive as well.

Most Indian company’s growing at this pace would be doubted about quality and integrity. There have been many instances - (also recently as well) where investors have got burnt due to cooking of numbers by the management. Difficult to get conviction unless numbers (free cash flow) aligns with management commentary and interactions. Appointing a Big 3 (PWC cannot audit listed companies. They have been debarred due to Satyam scam ) gives assurance on the sanctity of the number (Not that local Indian auditors do not. But there is a perception issue here as well). But at the end numbers need to speak for itself.

I think the way to think about it mathematically is that it is a 15% ROE company, growing at 30-35%. So it will not generate cash as long as growth > ROE. So that is worth keeping in mind. I am certain based on references the business is for real, the question is what level of 5-10% subjectivity on booking certain revs the current auditor has allowed vs. what a big-3 would allow.

I think their auditor is aGD Apte and is one of the 15 shortlisted for forensic audit in India.

I am sure they will not the change the auditor unless there are issues.SGurumurthy happens to be a friend and advisor and he thinks the big 4 is just a hype.

2 years back Ambit came up with a proposal to list it in the USA where they advised that it will get a mkt cap of 4 times what it has in India.The proposal has been kept in abeyance till other issues are resolved.

The company is focussing on increasing it’s US revenues before getting a US listing.Towards acheiving that the recent issue of warrants to promoters.

2-3 years down the line there is a strong possibility of the US subsidiary listing there.

The immediate news flow could be one or two acquisitions coming through.

Can you elaborate, What are the other issues that are to be resolved?

Getting listed in the US without having one of the Global auditors would anyways dilute the credibility. They will have to change them if the ambition is to get listed in the US.

The valuation and Market Cap is influenced by global/ Institutional informed investors. If the business model is understood and appreciated well by these investors, valuation and market cap would get ultimately reflected. It would be a challenge to attract large informed investors without a global audit firm in place.

Vaibhav Global recently changed its auditors to KPMG as they were facing similar challenges.

The street is finding it difficult to believe the results being churned out by the company, all the commentary made by the CEO is being treated with skepticism.

As is said P&L is an opinion, Cashflow is reality. TAKE’s business model revolves around technology platform as well as Services. This kind of model should generate significant free cashflows. If it does, the company can get high valuations in Indian markets as well.

I saw the operating cash flows which is a measure of the company’s performance, positive over the last 3 years and this half year.The group has been a favourite of PE funds even without the big four as a auditor in SCUF/STFC and that will continue till the push comes to a shove.They already have a auditor for their US subsidiary under US laws.

The hesitation with institutional investors is the absence of a competing company to compare.The whole business model is not easy to understand as it is neither a pharma company nor a software company.

The “other issues” I was referring is what I gather from sources is a Mckinsey report for US business given the uncertainty relating to visas and politics,Two years back they kept the Ambit report in abeyance till they double their US turnover.The other task undertaken is to increase the global footprint by setting up a European subsidiary.The latter has been successfully done and the former is being done.

Recently in their group(not exactly a group co but having the same mentor) co STFC there was an issue on a guarantee to a group co which was referred to NCLT.and the consequent fall in STFC.The ex chairman has repeatedly stated that the ethics of business are always important and declared that there will be no devolvement of this guarantee on STFC.This is to just illustrate how he believes that ethics are important and hence there can be no question of suspecting their results/figs.

Fear and greed are part of equity investment and skepticism and euphoria are part of this phenomenon

Auditors in the US are a lot more worried about going to jail than in India. I think you have your Enron examples with Arthur Andersen but by and large even smaller ones are considered more reliable than the CA shops in India

Apte has audited Shriram group companies; they’ve had marquee PE and FII investors who’ve never had a problem with them. Yes, they are pig headed about not changing the guy but it might change soon if they realize this kind of hard to understand, more subjective business needs a top notch auditor, esp at this scale

If this was listed in the US, it would get a 10-12x EBITDA multiple. The thing to remember is that it makes sense to grow fast and hard here to get to a certain scale because revenues are super sticky, a lot more than those of IT services. Once growth sort of levels off to 10-15% 3-4-5 years from now, cash flows will look a lot better. Operating cash flows ex-growth working capital are the right metric to look at - take your operating cash flows and subtract 140/365*(delta in sales YoY) and subtract maintenance capex. I agree that they could a much much job explaining this to the market

1 Like

I believe the Part-2 of the Moneylife article is out.

Could someone please point out if there’s anything material this time?