Mr. Nrupesh Shah Interview on Q4FY18 results

Has anyone here actually used a Symphony cooler? I was searching on Amazon, and the ratings are quite low. Hardly any product has >3 stars. Some of the user reviews are really bad.

Would be great if someone could talk about their experience. Thanks.

Attached are the reviews for Symphony’s 3 biggest competitors. They are <3 as well. Is the conclusion now then that coolers are bad as a product?

we had bought symphony coolers two year back at a premium to other available products. some lessons

- the dealer recommended other brands in lie.

- The power consumption has considerable risen

- the price difference was almost 20% with the other more home known brands

- we have now replaced the same with a LG ac which cost almost the same as the top end symphony cooler.

takeaways can be assumed.

1 Like

| Best Symphony Air Coolers Models | Rs. |

|---|---|

| Symphony Diet 12T Tower 12L Air Cooler | 5849 |

| Symphony Ice Cube XL 17L Room Air Cooler | 5900 |

| Symphony Window 41 Window 41L Air Cooler | 8099 |

| Symphony Winter Desert 56L Air Cooler | 12220 |

| Symphony Touch 20 20-Litre Air cooler | 6302 |

| Symphony DiET 50i Tower 50L Air Cooler (With Remote) | 8850 |

| Symphony Jumbo Jr. (With Trolley) Room 22L Air Cooler | 8291 |

| Symphony Siesta 70 Desert 70L Air Cooler | 11249 |

| Symphony 15L Cloud Tower Air Cooler | 14448 |

| Symphony Storm 70i Tower 70L Air Cooler | 14799 |

| LG AC Price List (2018) | |

| LG AC Price List | Rs. |

| LG L-Crescent Plus LWA5CP5A 1.5 Ton 5 Star Window AC | Rs. 25,143 |

| LG L-Nova Plus LSA3NP3A 1 Ton 3 Star Split AC | Rs. 28,399 |

| LG L-Nova Plus LSA5NP2A1 1.5 Ton 2 Star Split AC | Rs. 28,990 |

| LG JS-Q18BPXA 1.5 Ton Inverter Split AC | Rs. 29,999 |

| LG JS-Q18NRXA 1.5 Ton Inverter Split AC | Rs. 35,870 |

| LG BSA18BEYD 1.5 Ton Inverter Split AC | Rs. 53,990 |

| LG JS-Q12BPXA 1 Ton Inverter Split AC | Rs. 28,499 |

| LG JS-Q18NPXA 1.5 Ton Inverter Split AC | Rs. 36,470 |

| LG JS-Q12AFXD 1 Ton Inverter Split AC | Rs. 29,990 |

| LG JS-Q18AUXA 1.5 Ton Inverter Split AC | Rs. 44,000 |

1 Like

Hi,

In local market it is not difficult to get a .75 ton AC for ~Rs.14K or even less.

Window AC Price List and Power Consumption Comparison for 0.75 Ton

Company Price (Rs.) Model No. Tonnage Star Rating EER Cooling Capacity Power Consumption Compressor(w/w) (Watts) (Units/hour)

Haier 13,899 HW-09C2 0.75 2 2.66 2500 0.94 Rotary

O’General 18,500 AKGA09AATB 0.75 N.A. 2.63 2498 0.95 Rotary

LG 18,000 LWA2CR1A 0.75 1 2.49 2489 1 Rotary

Voltas 15,290 GOLD 2S (4011021) 0.75 2 2.55 2509 0.984 Rotary

Whirlpool 17,000 WAR09G20DW0 0.8 2 2580 0.95 Rotary

Carrier GWRAC009ER001 / GWRAC009EM001 0.75 3 2928 0.96 Rotary

Godrej 16,990 GWC 10GG 2 WJM 0.75 2 2.52 2505 0.994 Rotary

Bluestar 16,700 2WAE081YB 0.75 2 2.57 2544 0.99 Rotary

1 Like

Symphony making Australian Acquisition

4 Likes

3 Likes

Company has informed FY19Q1 earnings conf call on 24th but has not shared dial-in details. I have emailed management asking for the same.If anyone has dial-in info, please share.

Thanks,

Amit

Any one attending con-call. Will appreciate few highlights he/she can put throwing light on de-growth.

Last quarter they had mentioned weak April and May due to bad weather… i guess that must have continued in June…

But yes someone who has attended the conf call…please share the highlights…

I would have attended, if I had dial-in info. It’s surprising why management doesn’t share dial-in info in it’s con-call announcement. I dropped email to CS couple of days back asking for dial-in info, but no response so far. Does management want only institutional analysts and not individual investors on the call? Very disappointing.

Disc: no holding

022 62801326 was no you might check if they make recording available.

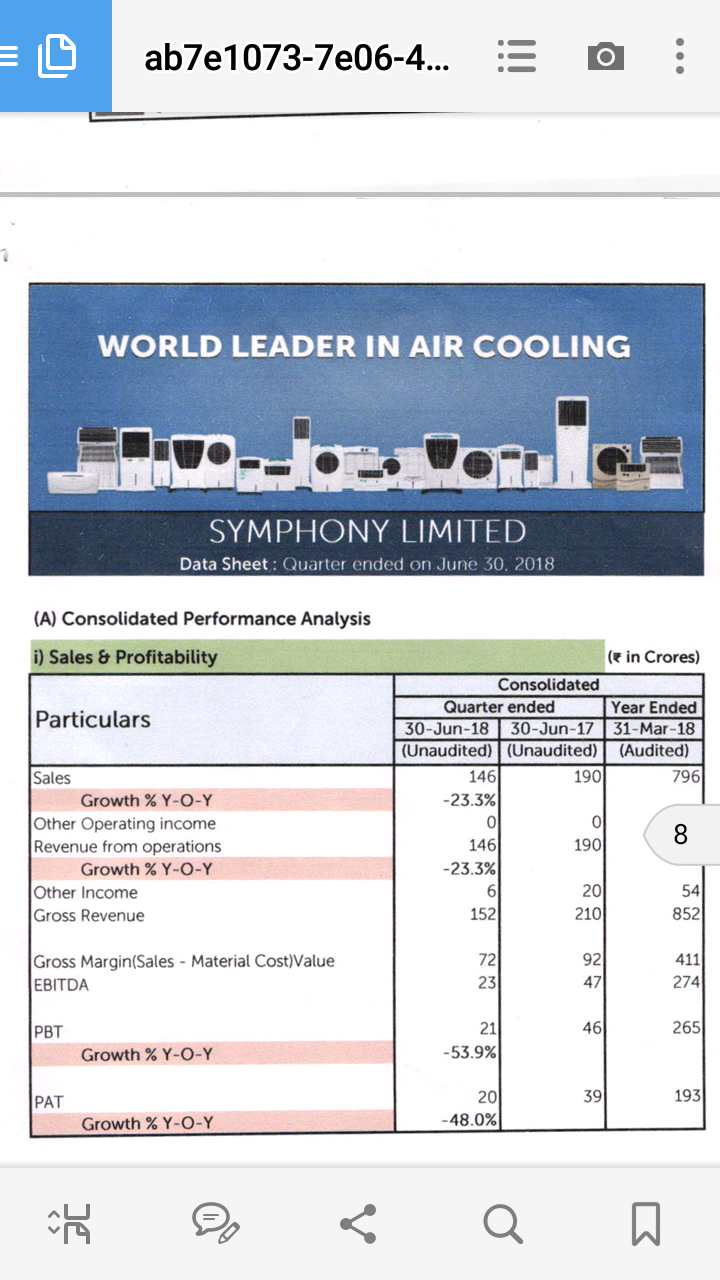

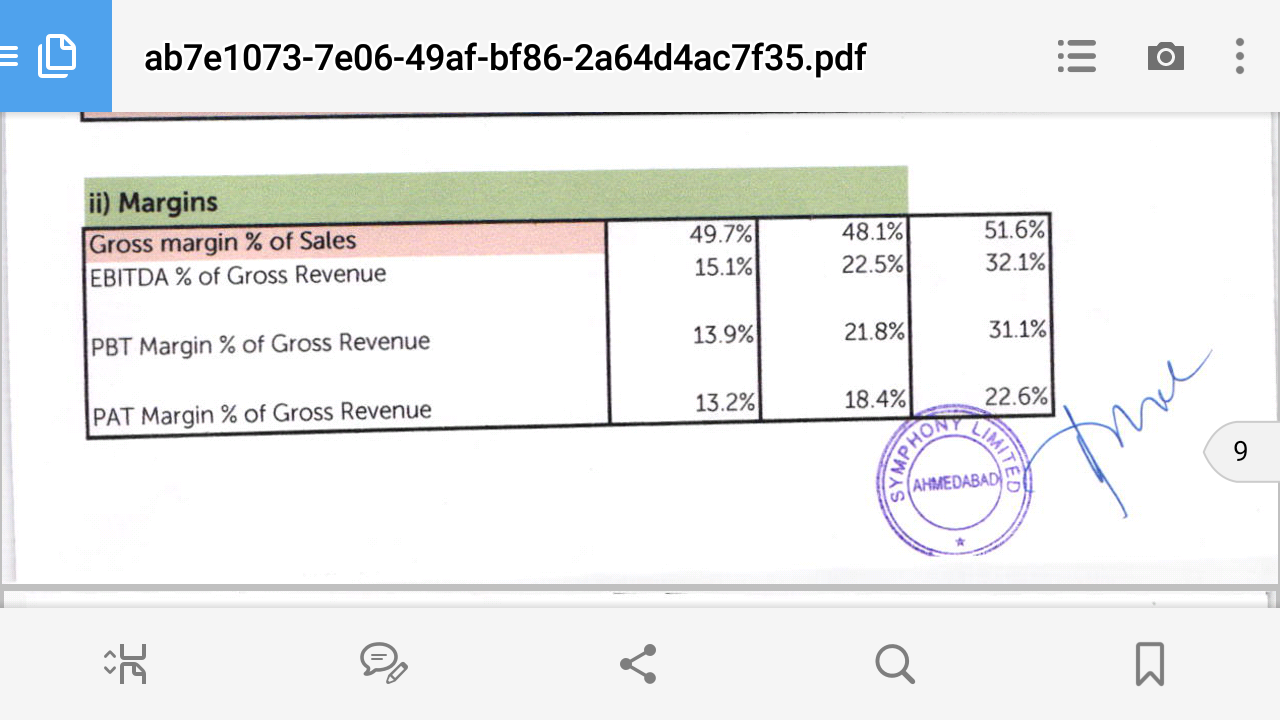

My notes from Q1FY19 con-call (source: researchbytes)

Management speak:

• Management disappointed by the performance in Q1FY19.

• Consolidated: Top-line declined 23%. Down from 190 crs to 146 crs. EBIDTA down from 47 crs to 23 crs (down by almost half). PAT down from 39 crs to 21 crs (down 48%)

• Solace in whole performance was the company maintaining capital employed.

• Geographical performance: ROW is intact. Same as last year. Domestic business severely hampered.

• Treasury now up to 449 crores

• Starting this quarter (Q1FY19) company will report basis on a consolidated basis. After acquiring Climate Technologies almost 40% of the business will be from ROW. Hence the move to report numbers on a consolidated basis.

• Domestic sales: Affected by bad summer. Second consecutive bad summer faced by the company. Impacted mainly because of this. Air conditioning and fans business have also suffered in India due to this and suffered de-growth.

• Company has not offered any discounts to prop up sales viz a viz competitors. Gross margins of the company have remained intact due to this. EBIDTA and PAT margins impacted as other costs, fixed costs etc. remained same.

• Market share intact (or maybe increased) as compared to a decline in the market. Most of the inventory lying with the company to be monetized in the next couple of quarters at most. Very possible the company will go through some pain in the ensuing quarters as well.

• As per their experience when there have been two back to back bad summers it leads to major consolidation in the industry in 2-3 years’ time.

• GSK and IMPCO have had profitable quarter.

• CT acquisition successfully completed. Discussed acquisition cost and other parameters. Not including here as details have been provided by the company earlier.

Analyst / Investor queries answered:

• Challenges going forward? Any change in pricing stance? Inventory?

o Pricing: No pricing changes going forward. The only challenge: Company experiencing weak trade sentiment. Confidence of trade partners shaken – some even contemplating exiting from the cooler business.

o Inventory: Overhang exists. Even company has significant inventory. Coming 2-3 quarters will not be good as compared to what the company has been doing historically.

o Distributors still have a lot of faith in the company as Symphony’s inventory was still moving as compared to the competitors. This has strengthened the faith of the distributors. In fact, some of competitor’s distributors are switching over to Symphony.

• Growth expectation going forward? New products? Support to trade partners

o FY19 is going to be a challenging year for the company.

o No new products to be launched in FY19 as there is already significant inventory in the market.

o Some support offered to trade partners. Something the company has had to resort for the first time in 30 years. As this is an exceptional situation, such support has been offered.

• Subsidiary performance

o IMPCO: Registered 12 crs profit this quarter. Profit at operating level is up 20% y-o-y

o GSK: Registered 3 crs profit this quarter.

o Same things may not be visible in the coming quarters. As the numbers above have been achieved in summer months.

o Australia (CT) will be having round the year business as compared to other subsidiaries.

• Branded cooler market may have de-grown by 15% this summer. Significant, inventory still lying in the channel, it will take time for it to be sold.

• Chinese market very fragmented. 100s of players in the market. Market potential is huge. No company has any significant market share. Therein lies the opportunity for Symphony. Company’s market share is low at the moment.

• US is also a very large market. Current business is very small. Prospects are solid. CT works with good customers there.

• Market share of CT in Aus 35%. IMPCO in Mexico has market share in excess of 40%.

My thoughts and observations:

• FY19 is going to be a weak year for Symphony as far as domestic sales go due to consecutive poor summers (first time in 30 years as per the management, apparently!)

• Performance of foreign subsidiaries may fill up the gap to a certain degree (esp. CT)

• Mr. Achal Bakeri didn’t sound happiest on the call today. And some poor and at times unnecessary probing by the analysts did seem to irritate him.

Disc: Invested

6 Likes

I think Symphony is one of the best companies when it comes to keeping both investors and analysts updated on how the business is shaping up each quarter.

Good quarter or bad - they speak up and mention things they way they are. They are top notch when it comes to corporate governance and communicating to shareholders / analysts imho.

Also, I have heard individual shareholders on quite a few Symphony calls.

Anyways, in case you wish to listen to the con-call for any company (including Symphony), you can do so on Researchbytes. I believe they do a great job of compiling conference calls across companies each quarter. Cheers.

3 Likes

Thank you @amangoklani for putting together con-call summary!

Let me first clarify that I’ve tremendous respect for Mr. Bakeri and I completely agree that management is top-notch. What Mr. Bakeri has done is close to a miracle! But at the same time I am also frustrated and disappointed with not being able to attend the con-call and not getting an opportunity to ask my questions to understand Symphony better. I had couple of very specific questions that I was hoping to ask Mr. Bakeri about his Version 3.0 strategy and better understand CT’s business model and their products that are sold in the US. Both questions had intention to better understand Symphony’s long-term strategy/prospects.

I went through con-call recording on researchbytes. Unfortunately, given dismal Q1FY19 numbers and given our Dalal Street analyst’s typical short-term view, most of them barring few were trying to understand how softer could coming off-season quarters get so that they can predict Q2, Q3 and Q4 EPS. Anyways, I will drop an email with my questions and let’s see if I get any response. Off-season is heading their way, so hopefully they should get enough free time to reply back.![]()

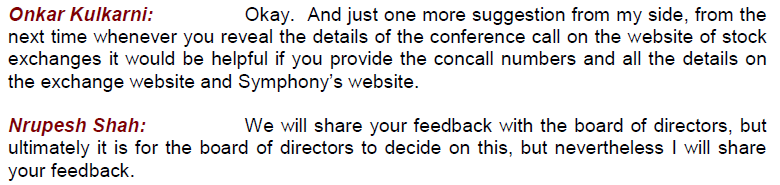

BTW - very curious as to how the individual investors are able to dial-in for conf calls since management doesn’t share call-in info. Below is screenshot of transcript from Q1FY18 call where Onkar Kulkarni, an individual investor was suggesting Mr. Shah to share concall numbers and details so that individual investors can also participate. All I am looking for is a rationale from management for not sharing call-in details with individual investors.

Researchbytes is a savior for many of us. Have been using it for last many years. Thanks for the recommendation.

Cheers!

2 Likes

Yes, I understand there is nothing better than speaking to the management directly and hearing things straight from the horses mouth.

If you haven’t written to the management already, may I ask you slide in another question?

The management keeps saying China is a huge opportunity - though they have never mentioned the total size of the market there (not to my knowledge). They’ve only mentioned it is fragmented and there is great potential for someone to gain a decent market share in the fragmented market.

Whereas for all other markets / business lines they’ve disclosed the market size -

- India residential cooler market = ~Rs. 3500 - 4000 crores (Overall market growing at 12% y-o-y. Organized market growing at 18% yo-y) (source: https://www.youtube.com/watch?v=LqrybOSi1t0)

- India industrial / centralized cooler market = ~ Rs. 4000 crores + (picked from Symphony’s corp presentation)

- US Market = ~ Rs.1700 - 2000 crores

- AUS Market = ~ Rs. 388 crores (derived) (CT sales = Rs. 274 crores. Rs. 247 cr sales from Aus (90%) 55% top line from ducted cooling in Aus = Rs.136 crores. 35% market share in coolers = 388 * 35% = ~ 136)

- China Market = ?

Symphony’s consolidated sales last year were Rs.798 crores and they are sitting on an opportunity to capture ~9,000 - 11,000 crores of the growing cooler market worldwide (sans China). I like that!

The other question that I was surprised no analyst asked was about reduced GST. Wouldn’t that make the prices of branded coolers more competitive viz a viz coolers from the unorganized market? I would certainly think so.

Hahaha, yes you are right. They will have a lot of time to answer now!

Symphony is now going to go through a sustained phase of dropping share prices and consolidation. Over time this will surely open a window of opportunity to load shares of this stellar company at least at fair prices.

3 Likes