Hi All,

This is slightly off the symphony topic, but wanted to discuss my thought if anyone is intrested in this comparison of two investments, I always thought of buying symphony , but remained stuck with Page Industries, as I can own only one of those as I can’t handle more than 10 stocks in my portfolio. Is there an edge that the symphony investment offers over page industries, in terms of possible upside?

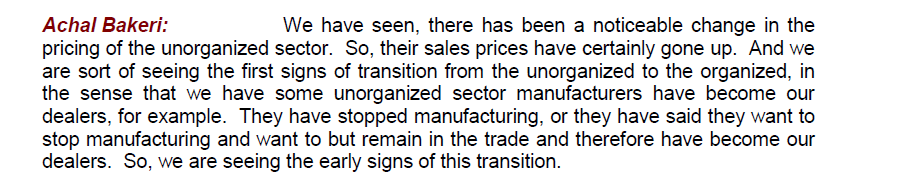

While going through Q3 concall transcript, I came across interesting response from Mr. Bakeri about GST impact on unorganized sector . Please see below -

Since air cooler penetration is very low and as income levels go up, I expect robust growth for companies like Symphony due to product innovations

Yes I agree that, Honey is categorised under FMCG while air coolers under consumer durables.

But the overall human behaviour is very similar, it is just that in Honey it is bought frequently where as in durables it is bought less frequently as the time gap is wide.

When multiple competitors come into the market, the advertisement noise level increases and it sows the seeds of “necessity” in the minds of consumers. From there on if he does a research he will be more oriented towards the market leader than a competitor, because we the human, always want the best. Thus even the advertisement by competitor can lead to some sales him, but can also get more customers to the leader. As the pie expands, more and more people identify who is the leader and even if he has priced it slightly premium, the products will sell. So a competitor who imitates the leader would most probably end up sacrificing his margin but may produce growth but is guaranteed to have poor returns. So an expansion of pie is always welcomed by entrenched leaders who in spite of their efforts were not able to expand the market.

While you may not agree on what I have stated above, if you listen to Rajiv Bajaj who explains it in Marketing terms, you will get the picture. The whole video is valuable, but for the subject under discussion you can watch starting from 15 minutes into the video where he explains it using the soda can strategy.

Also we need to remember how the vendor would act. In the case of air cooler, most of the durable sellers would have pre-paid and bought the product from Symphony because that is how they sell their product. So his money is already locked in and the earlier he encashes it, it is better for him. So his sales guys would be pushing Symphony more than other brand products. Also he will place all the Symphony products at the best eye catching location to influence the consumer. Other brand products would only get a second tier shelf space. And the competitor brands provide their products on credit and in worst situation, the vendor may return the product saying the product is not selling in the market.

Symphony AR FY17 aptly captures this on page 48 & 49.

And the FY18 Q3 transcript reveals the inventory buildup for the competitors the result of aping the leader rather than finding their own niche.

Naveen Trivedi: Since you commented that the competition has largely channel inventories of the last season, so considering that, do you think that the competition can use the discounting tool during this season?

Nrupesh Shah: During the peak season that is April to June, competition was not only granting the credit, but also offering rampant discount. And despite that they are left with huge inventory. So, it is not only the pricing, but the product performance, design, brand and distribution network and service after sales, so combination of all those factors. And ultimately and very importantly, during the off season that is September and December quarter, when trade builds up the inventory with 100% advance, that is also overall reflection of consumer confidence.

Naveen Trivedi: So, when we say the competitors have large inventory, so is it that even the top two, top three players also had a large inventory during the last season?

Achal Bakeri: In the trade, they surely have.

Naveen Trivedi: Okay. So, because the last year the summer was slightly volatile and even some shower has happened during December and I think that has led to the high inventory.

Achal Bakeri: That is right.

Naveen Trivedi: So, considering high channel inventory, but still in the last two-three quarters, if Symphony can grow 20% growth despite the channel also aware about the high competition inventory, it suggests that the acceptance of our all new launches is guiding strong growth in the last two quarters, quarter two and quarter three, is it a fair assumption?

Nrupesh Shah: That is right.

2 Likes

Sir,

To compare human behavior, Honey might not be appropriate, as there is very little innovation or change in the basic product. Honey remains honey after 1000 years (except honey from Himalayas or Nilgiris). Therefore, these products are then benchmarked in terms of quality, which in turn are related to reputation and price(higher the better). The same analogy goes for chyvanprash. The basic product remains the same.

However, a fair comparison could be Mobile phones or TVs. If a high quality product with better features could be produced by anyone, they could beat the competition. We got numerous examples, staeting from a question as to who remember Blackberry these days. What did Xiomi do to competition in mobiles (especially in the niche eastern markets). The next domination of Xiomi is in TVs . Look at the quality offered and the price (4K TVs 55inch at INR 35K, if you haven’t, kindly check flipkart). My hands too twitch to get one the soonest. Who cares to find the market leader, with those features and the price point.

To sum up, with no entry barriers; product innovation and pricing holds the key. The moment someone comes out with another innovation (technology, price or both), the wind will go milder on the sails of this company.

Disc.:No investment, only academic interest in the ongoing discussion. This company is in my radar, however not at these valuations.

1 Like

If i understand correctly, these are the only things precisely SYMPHONY do, and offload all other work to third party.

Symphony has been an outlier for sure. But how long it can remain so is the question. To my knowledge, at least 3 companies with brand power have entered air coolers business in last 2-3 years (Voltas, Blue Star, Havells). As the competition grows, can Symphony maintain 50% market share and 25%+ net margin? If we take example of air conditioner industry, the market share for the leader is around 20% for Voltas. And, all AC companies have very low margin due to competition.

The idea is not about who sells the maximum, it is about how long a company is on its toes and maintains its niche. The moment market smells it lost its superiority, price will crash.

We have seen BPLs and Onidas disappearing with no trace. And it can happen to Xiomi as well or it may become the next Samsung who knows.

But as a owner of a company, I am concerned about the inherent strength of the company and the niche it has and how it maintains it year after year with rigour. The ultimate kicker would be growth on top of a tightly run ship. I see that both in Symphony.

Competition even now it exists. That is why Symphony’s market share is not 90+ but 50+ only. Usha, Bajaj, Kenstar are already well known brands and they are in market. A few more if they join, they may grab the market share and Symphony may command a market share of 40% or 30% or 20%. So be it. Because of competition the pie will grow and the margins will shrink. It is not that they don’t sell their air coolers on credit. They do.

But if they maintain the margin leadership, continue to be ahead of others, that is what matters. Do not forget they are selling their products in 60+ countries.

Like Rajiv Bajaj repeats there is not much technology difference in any of the bike manufacturer. But it is in the consumer’s mind. As long as the consumer perceives it as premium, the company will milk him. The same applies for Symphony.

1 Like

I am looking in investor’s point of view. At current price, I don’t see value as earnings growth may slow down due market share loss and margin contraction.

SYMPHONY is the best company in Air Cooler Business and have stamina to remain on top as management is far ahead than competitors in product innovation, distribution network, product quality and after sales services. It is a company like Page, HDFC bank, Eicher wherein people think it is costly but it remain costly always and miss to ride the growth !

Unless all-round market crash due to external factors, we never get such company cheaper!

1 Like

This should hold the company in good stead this year. Hopeful of seeing some robust sales this year.

2 Likes

Looks company is finding it difficult to keep sales from declining.

totally agree. long term growth of 15-20% is realistic… eventually all companies will fall into this band over long term…that is the precise reason PE ratio of 15 to 20 are long term historically sustainable

Good result only problem is that company was not able to show growth when compared to previous qtrs

Looking fwd to the new acquisition which the company has highlighted in an another report to exchange

GST has not given great incentive to organised players. Local ones are able to manage this. Cheap import of air-conditioners from China is another issue. PE is high. It is going to be really long term to see 15-20% growth in profits. Frankly, I do not see this soon.

Disclosure - 5% of Portfolio.

Not that good a year compared to the valuations it trades at…But given the execution capability of the management…have to wait and trust them to bring it back to good growth levels…

GST effect might take longer to benefit the organized playeers…

But i would think it will be back on track to decent growth figures next year…

Just to give perspective…

Q4 and Q1 is a major revenue season for this industry. Today’s Times of India Kolkata edition carries article that ACs sales are down by about 10% due to frequent, unseasonal rain especially in North but also almost across the country.

Last week in Havells con call also they said same. It is more of external negative issues for industry n not headwind to specific company.

Growth should be seen with this perspective on relative basis.

2 Likes

But for the full year also, revenue growth is only 5%.