Concall Highlights (source: capital market)

The company has sold 83175 MT of plastic goods a volume growth of 5% for the Sep 18 quarter on YoY basis.

No inventory gain or loss in Sep 18 quarter

Focus remains to increase sale of value added products and improve ROC of the company.

Expects net sales of around Rs 5700 crore to 5800 crore for FY 19 and volume growth for FY 19 to be at 10% as compared to 7% for H1 FY 19.

Packaging business has seen some plant shut down so volume was down but year end volumes should not be a problem.

In Sep 18 quarter, Company has realised Rs. 80.85 crore from sale of 38718 sq. ft. of the premises.

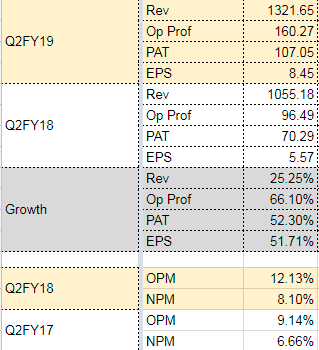

Excluding the construction income, PAT for Sep 18 quarter stood at Rs 72.70 crore as compared to Rs 70.82 crore for Sep 17 quarter.

35% value added product sale in Sep 18 quarter as compared to 37% YoY.

All polymer prices have declined. Expects international polymer prices to remain low and will have a downward bias given the new capacities of polymers coming worldwide.

Average net borrowing as on Sep 18 stood at Rs 259 crore vis a vis Rs 248 crore as on Mar 18. Average net borrowing cost stood at 7.07% vis a vis 7.12% at start of the year.

Demand of plastic products remain positive.

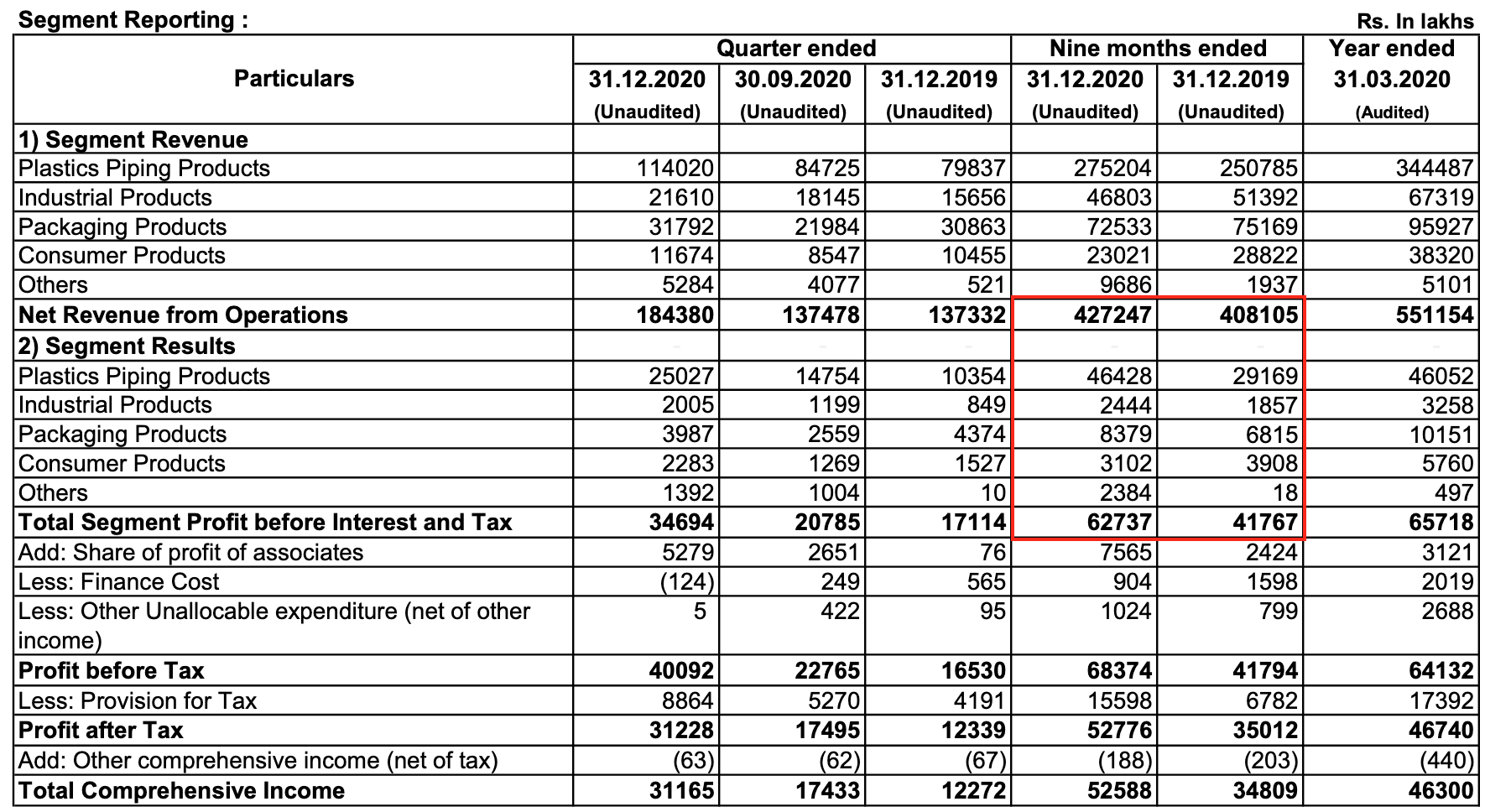

Ebidta margin for plastic piping stood at 13% and the segment grew by 7% in volume terms in Sep 18 quarter. Ebidta margin in Packaging products stood at 15.7% and the segment de-grew by 3% in volumes in Sep 17 quarter.

Industrial products volumes grew by 8% in Sep 17 quarter with Ebidta margin of 11.1%. Consumer products volume was down by 2% and margin stood at 16%.

Capex for FY 19 stood at Rs 280 crore. All the capex plan is progressing well.

Piping demand is strong

The rupee depreciation had seen some forex hedging gain in other income and some MTM forex loss which resulted in some high interest cost Sep 18 quarter.

Expects around 15-15.5% OPM for FY 19.

Company’s business is very much dependent on agri sector, construction activities and other industrial pick up.

Housing demand remains strong and from Nov onwards should be stronger. Big push of affordable housing will also lead to higher demand of construction which is good for the company.