Sumit Woods Ltd is recently listed Co listed in SME Platforms at NSE Emerge…

Promotors:- Sumit Woods Ltd is leading Developer having projects in Mumbai and Goa, SWL take up mid size Projects. Co Promoted by Mitaram Jangid & Subodh Nemlekar now Second Bhushan Nemlekar (Harvard Graduate) too joined the Business.

SWL successfully running the Business since last 30+ Years and delivered over 5000 units spanning over 52 Projects.

All the Projects delivered with OC

Sector outlook :-

Real Estate Sector in MMR on revival mode, Mumbai will have World Class infra in next few Years that will attract huge demand going forward.

Unsold Inventory is big issue in the Sector but once we analyse the data most of the inventory belongs to large luxury projects and Projects in way far (Locations disadvantage) & Projects stuck due to approvals or Financial reasons. All such inventory having age of over 3 Years hence in normal ongoing projects inventory isn’t that big issue.

Business Model :-

Since the beginning Co working on Joint Development Projects, Redevelopment Projects, now started getting Projects on Development Management Model. Co provides housing to Mid Income Group.

Co adopted Asset Light Business Model since bigining and don’t believe in buying Lands.

SWL believe themselves as a huge beneficiary of RERA, SWL believe that they working according to the RERA norms since beginning.

Pros :-

Strong Asset Light Business Model

Strong and timely execution of Projects

Strong execution lead better Reputation & enjoy better sales outcomes

Inventory levels is almost Nil

Start Projects with all necessary approvals and Financial Closures so risk of being stuck is Negligible

Debt Equity ratio is nearly 0.30

Finance Cost is nearly 12-13% which is phenomenal in the segment.

Strong Project Pipeline, currently around 9-10 project in pipeline and 3-5 Projects may be added in next 2 Qtrs, Got Completion Certificates(OCs) for 3 Projects in past 3-4 Months

Strong inhouse Team to execute the Projects.

Zero litigation from Consumer

Cons :-

Sector is very difficult to understand

Recent liquidity crunch affected the Sector and it may harm further to the entire sector

Policy and Tax issues affect the Industry

Project Execution delay may harm earnings prospects

Regulatory Changes may impact health of the Cos

Every project have different Business Matrixes

Valuations :-

CMP 45

PBV 0.85

EPS (Diluted) 5.00 FY18, 7.00 FY19E

PE Ratio. 6-6.50

MCap 65-67 Crs

RoE & RoCE ~ 17%

Debt Equity 0.30

Expected 3-5 Years CAGR Profit 25-30%

Evaluating on going Projects and expected to commence immediate future I’m Expecting Rs 150-250 Crs Net Cash Earnings (Pre Tax & Amortisation & net of Debt) spanning next 3-5 Years

Disclosure : Invested & willing to add more!

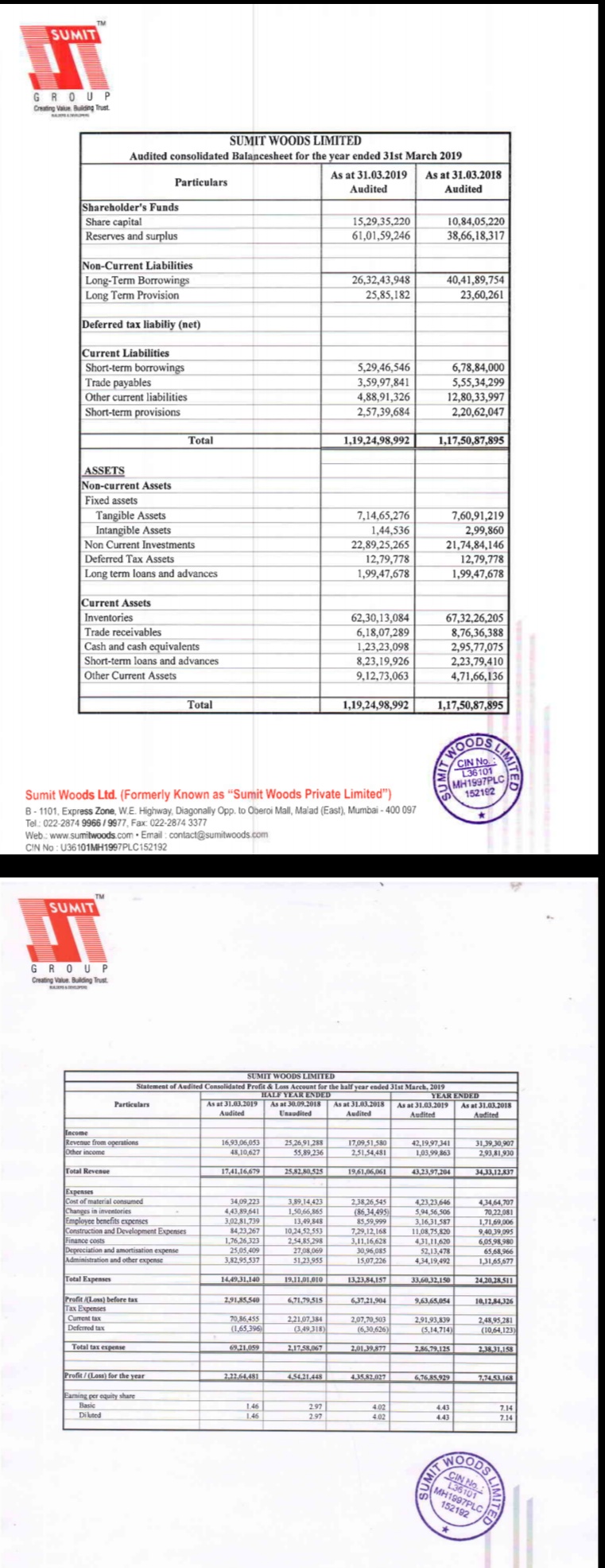

Financial & Cash Flow abstracted from RHP

(upload://xjL8y7TqGLHzPdpMlw8Mo59Dt42.jpeg)

Can you please share details of the projects that the company is undertaking. The area that it is looking to sell and the realisation that the company expects.

Also please share the Debt, profitability status etc.

This will be much more beneficial than giving projected EPS

Ashwini,

That’s true that Real Estate Cos not valued at EPS.

Being Asset Light Business Model SWL don’t buy much Land so valuing it on NAV basis will be very difficult.

Current Debt of the Co is around 25-26 Crs against Shareholders fund of around 75 Crs, so debt equity comes around 0.30-0.35

SWL work on JV Models and Development Management Model so better to value it on expected Cash flow generation.

SWL have 8-9 Project’s running out of these 5-6 are self funded which show financial strength of the Co.

Co maintaining around 30% EBITDA and around 20% PAT Margins.

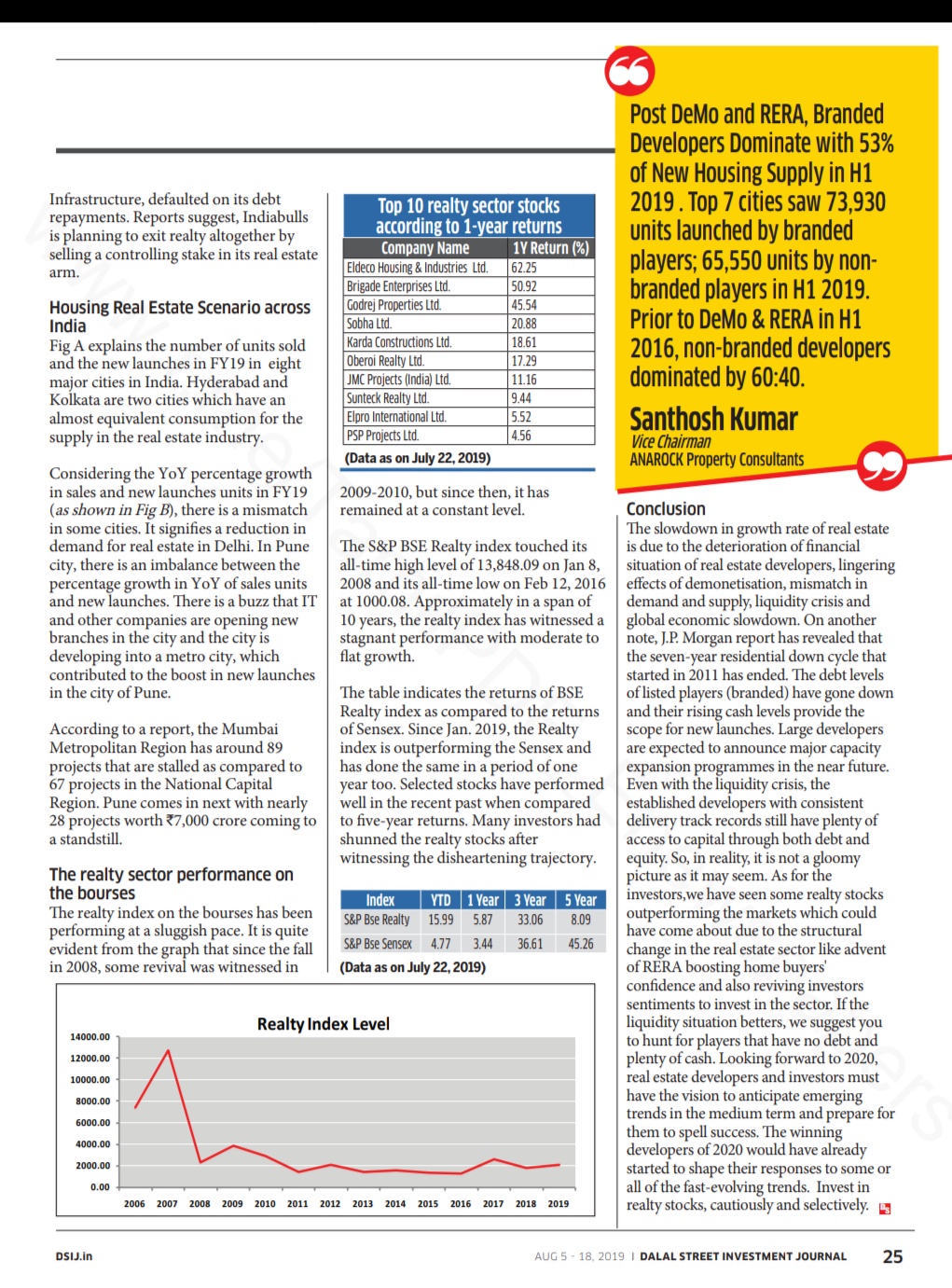

“Top 10 listed entities, including Ashiana Housing, Brigade Enterprises, DLF, Godrej Properties, Mahindra Lifespace Developers, Oberoi Realty, Prestige Estates Projects, Puravankara, Peninsula Land and Sobha sold nearly 32.19 million sqft, registering a robust 44 per cent growth over the previous year, rating agency Icra said.”

“Home-buyers are increasingly leaning towards developers with an established track record of on-time and quality project completion. Pricing also remains a key driver of purchase decisions. Thus, focused execution, resulting in timely deliveries, and developer emphasis on increasing affordability of residential projects, has supported sales levels for the larger listed players,”

Organised & Well Established Players will have edge being Strong Executioners, Brand and Strong Balance Sheet

After a long time and waiting now State Govt announced the relaxation in some norms.

Industry sources says Mumbai have more than 30000 Buildings for redevelopment but city don’t have required competent developers.

Competent players have ample opportunities now and for future

(1) The additional development cess for infrastructure purposes, which was payable over the additional FSI component has been withdrawn.

(2) The CM-led urban development department has lowered the premium payable on the FSI, which is granted to all projects in Mumbai on payment of a premium, from 50 per cent to 40 per cent.

(3) Premiums payable for compensatory fungible FSI in residential and commercial projects have been brought down to 35 per cent and 40 per cent of the ready reckoner (RR) values respectively.

(4) To push the development of information technology parks and similar specialised commercial projects, premiums for the incentive FSI has also been lowered to 40 per cent.

(5) For fast tracking redevelopment of dilapidated buildings in Mhada-owned colonies, the government has meanwhile proposed a 50 per cent reduction in the premiums payable on the incentive FSI component in such redevelopment projects in the economically weaker and low income segments and a 25 per cent reduction in the middle and high income segments.

(6) To promote development of multi-storied public parking lots on private land, the premiums payable on the incentive FSI component of such projects has also been lowered from 60 per cent to 50 per cent. The government has said that the concessions offered will be valid for a period of two years.