As per mgmt, at full utilization of the upcoming alloy wheel and CV wheel plants, an additional 800cr topline can be expected. Ideally we should see this by fy 18-19. The margins for alloy wheels will be higher. The mcap is around 1350cr however they do have a debt of 800cr which will weigh down on the bottomline till full capacity is achieved. A lot will depend on timely execution. There was a small amt of promoter buying yesterday.

Disc: invested.

1 Like

Just to note, the CV demand is huge. They run close to full utilization as soon as plants become operational.

If alloy wheel demand picks up, that would be great. This will start testing in Jan’18 and probably start production from Q1 FY19. With higher margins, this would really take SSWL to much higher levels.

On debt, they have mix of Indian and Foreign debts which keeps the interest cost under check. On an average, there debt is about 7.5% and if you eliminate the tax savings, it would come to around 5% which is actually good.

In my opinion, this company has excellent quality which keeps the orders coming, good expansion plans and debt commitments under check. Patience will be needed to see the results.

1 Like

Promoter is buying shares from open market through DHG Marketing Pvt. Ltd. Mr. Manohar Lal Jain, ED of SSWL is also a Director of DHG Marketing. The purchase on 22/11/17 was 5137 shares only. Substantial quantity- 1,29,957 shares was purchased next day (disclosed to exchanges on 24/11/17).

Promoter Group Companies DHG bought shares on 22 Nov, 2017. Further the company bought 1,29,957 shares on 23 Nov, 2017 sold by GS Global Corporation (look at GS description below).

Three days later subsequent to this acquisition, the promoters are releasing the news of bagging miniscule back to back export orders Nov 27 (one-time order of barely 2,500 wheels to be supplied in Dec’17) and Nov 30 (6,000 wheels to be supplied over 12 months). And the stock is rallying.

Looks like people blindly buying promoter instigated stories. Isn’t it surprising that promoters are buying shares just before releasing the export order news which will have no material impact on the books.

GS Global Corp, is engaged in steel trading business based out of Korea who sold their holding which was bought by Promoter. Not sure why Korean based steel trading company is engage in buying Indian company which is into wheel manufacturing.

Many fishy things are emerging out of this pack. Trade cautiously and carefully.

GS Global Corp. is a Korea-based trading company specialized in the export, import and triangular trade activities. The Company operates its business mainly through steel and metal segment, and resource and commodities segment. Its steel and metal segment imports, exports and trades steel and metal products sourced from the domestic and overseas manufacturers. Its resource and commodities segment imports, exports and trades petroleum products, petrochemicals, cement, coal, engines and other machines and industrial plants. It also provides inspection, storage and maintenance services for imported cars. In addition, through its subsidiaries, it engages in the manufacture of industrial equipment, including chemical equipment, such as heat exchangers, pressure vessels, columns, towers, reactors and others, and energy equipment, such as heat recovery steam generators, steam drums, condensers and others.

Just wanted to clarify one thing here - Steel Strips has a practice of regularly updating the orders it receive to the respective exchanges. You can verify its disclosure history. I consider this as a sign of transparency and good corporate governance which would help investors make better informed decisions.

Investment/ trading in any financial instrument is subject to understanding, discretion and risk appetite of the individual.

Disclosure: Invested in Steel Strips.

Hi,

Anyone have info on when their alloy wheel plant start commercial production, I hope next leg of rally start once this plant start production.

Regards,

Sathish

As per the announcement in BSE today - February topline has witnessed a growth of 53% YoY primarily aided by significant improvement in tractor and truck segments.

Sales growth for April 2018:

Sswl result looks very good even raw material prices up they are able to increase ebitda margin

5fc7a63c-f008-465b-943d-f98dd9f66b12.PDF (1.5 MB)

In the Q4 result, the comparable net revenues were 431cr in Q4 FY18 vs. 380cr in Q4 FY17

However, if I add monthly figures (Net revenue) that gets reported every month, there is a significant difference-

| Revenues | 2018 | 2017 |

|---|---|---|

| Mar | 169 | 127 |

| Feb | 150 | 109 |

| Jan | 127 | 108 |

| Total | 446 | 344 |

Can anyone please explain the difference?

A small difference can be because of export orders. But, in case of Q4 2017, it is huge.

Is it something related to the tax rate (GST) ?

I have taken net revenues everywhere to be comparable.

Increase in stake by management, SAST disclosure:

Hi,

Very good sales value and volume for may month . Now 2 consecutive month of more than 225cr sales . This rate they can clock easily 650cr for this quarter

d9d7d3e1-e873-4ef7-ae44-041c38458b3a.PDF (424.4 KB)

I am not sure but this my be due to exclusion of excise duty in Q4 2017 sales to make it comparable

Order win from US:

Found Some updates on SSWL Alloy wheel segments.

-

I think Alloy Wheels segment and has established a capacity of 1.5 million wheels which ran at 30% capacity in FY17-18, and management targeting 75% utilization for FY18-19.

-

Greenfield alloy wheel plant in Mehsana, Gujarat to drive growth: With its Gujarat foray, SSWL is breaking ground in alloy wheel production for the first time with an initial capacity of 1.5 million wheels; which has been has commenced production in Q4FY18. The technical collaboration with Kalink Korea, will see SSWL acquire the knowhow for design and production of alloy wheels. SSWL has started alloy wheel exports to Kalink in Q4FY18. It is expected to ship 30-35k wheels per month to Kalink under the buyback agreement. With this, SSWL is expected to garner ~Rs 10 Cr. export revenue per month from Kalink.

-

There are a number of other alloy wheel manufacturers and most of them are struggling with quality issues leading to higher rejection rates. SSWL believes that they have superior technology, (KALINK from Korea is their technical collaborator) and have Diamond cut alloy wheels which are superior to most other alloy wheels manufactured in the country.

-

Have been able to reduce the rejection rates in alloy wheels from 13% initially to around 7‐8% now and expect to reduce the same to 5% by the time commercial production starts and targets to settle at somewhere around 3.3% once it stabilizes.

-

Good response from domestic OEMs could lead to faster ramp-up: Peak turnover which can be attained with this initial capacity is Rs 450 Cr. We expect SSWL to have a capacity utilization of over 50% by FY19E. SSWL has already signed agreements with some major OEMs to supply alloy wheels for their models and is in discussion with several other OEMs. It has received orders from Hyundai, Tata Motors, Ford, Mahindra, Nissan etc. Seeing the response from OEMs, ramp up is expected to be faster and phase 2 (additional 1 million wheels) of alloy wheel plant which was planned to be commissioned by FY19-20E could start earlier than expected. The other major players competing in the alloy wheel segment along with SSWL are Minda Industries and Enkei Wheels.

-

High value high growth alloy wheels segment to boost margins: Due to advantages of better appearance than steel wheels, enhanced aesthetic appeal, light weight, better fuel efficiency and adherence to stricter emission norms, the price of alloy wheel is 4-5 times the steel wheel which will have a positive impact on the margins of the company. SSWL is the only player in India to come up with diamond cut facility (~25% of alloy wheel capacity) which is a value added proposition and has better margin profile as compared to alloy wheels. Also it is the only player to come up with low pressure die casting which has lower rejection rate as compared to gravity die casting. All these factors will improve the average blended realizations of the product mix going forward.

-

Axis Brokerage view on SSWL Debt: SSWL’s debt levels stood at ~Rs 850 Cr as of Dec’17 (~Rs 600 Cr LT debt and ~Rs 250Cr ST debt). This includes entire debt taken for both the CV line and alloy wheels expansion as well as for Hot rolling mill. The management indicates the debt has peaked out and they are on track with debt repayment of Rs 85-90 Cr every year in the next 5 years. FY19E would be the year when SSWL would reap the real fruits of both its expansions (CV and alloy wheel). Alloy wheels and CV segment exports are expected to add significant value for the company going ahead. We expect revenues to grow at 19% CAGR and earnings to grow at 31% CAGR over FY17-20E.

Disc: Invested tracking position recently. All the above information is from the below sources.

3 Likes

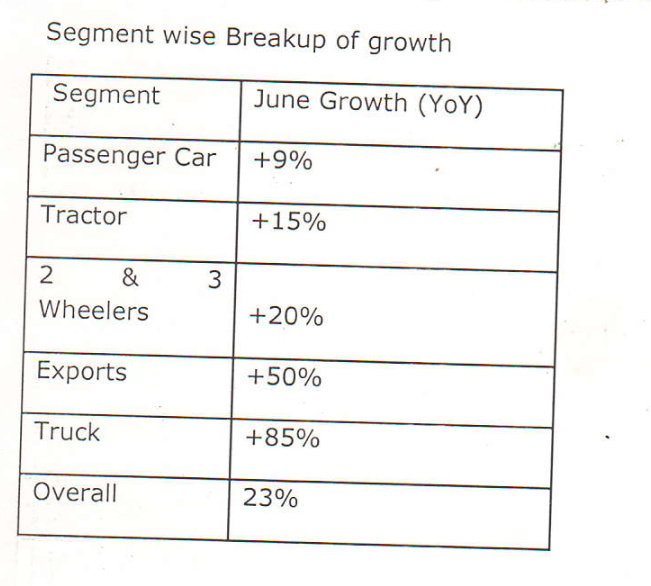

SSWL June 2018 Sales Turnover Up 76%, Sales Volume Up 23% Boosted By Truck, Tractor & Export Segment Sales.

SSWL achieved total wheel rim sales of 12.66 Lacs in June 2018 Vs 10.29 Lacs in June 2017 representing a growth of 23% YoY. The growth in June was all around segments and we expect this to continue going ahead with firm schedule indication 15% plus volume growth.

In terms of Value, the company has achieved gross turnover of Rs 197.60 Crs in June 2018 Vs 112.45 Crs in June 2017, there by recording a growth of 76% and achieved Net turnover of Rs.155.96 Crs in June 2018 Vs Rs.100.43 Crs in June 2017, recording a growth of 55%.

Chennai Car Plant Achieved Highest Production Ever in June 2018

https://www.bseindia.com/xml-data/corpfiling/AttachLive/bfcf0f6c-5e81-4922-a568-7a4ce52f57ff.PDF

2 Likes

SSWL Wins largest Exports order for Truck & Trailer Aftermarket from USA.

-

Order comprises supplies of 110,000 truck steel Wheels in 5 months from its Chennai plant from next month onwards. Total revenue generated by this additional order would be close to USD 5 mln in 5 months which is also expected to be repeated.

-

This big order will mark SSWL’'s arrival in the high potential NA Truck steel wheels market. Sswl is in discussions with other large truck & trailer makers in USA and expects to close similar big contracts in this segment in near future.

-

SSWL expects to significantly increase its presence in high potential Truck & Trailer wheels market in US & EU in the coming months and it’'s capacity enhancement at Chennai plant, which is in progress, will support this strategy.

SSWL Gets 18,000 Wheels Order From European Aftermarket

![]() Steel Strips Wheels Limited (SSWL) is pleased to announce bagging of Exports order of Steel wheels form European Aftermarket. Total order covers supplies of approx. 18,000 wheels in Aug 2018 from SSWL’s Chennai.

Steel Strips Wheels Limited (SSWL) is pleased to announce bagging of Exports order of Steel wheels form European Aftermarket. Total order covers supplies of approx. 18,000 wheels in Aug 2018 from SSWL’s Chennai.

![]() This order further augments SSWL’s strong presence in the competitive European Aftermarket for Steel wheels. We expect repeat orders from these customers in future.

This order further augments SSWL’s strong presence in the competitive European Aftermarket for Steel wheels. We expect repeat orders from these customers in future.

Attachment: https://www.bseindia.com/xml-data/corpfiling/AttachLive/2c065308-1d5c-4a29-ade1-675789aa409e.PDF