You can listen here

Thank you Mr Banerjee. This is extremely useful link. I did not know about it.

1 Like

Quarter and year ended 31st March 2020.pdf (3.5 MB)

QoQ good results.

Shree Pushkar Chemicals & Fertilizers consolidated net profit rises 47.06% in the March 2020 quarter

2 Likes

Increase in net profit is mainly due to tax reversals…so dont look at PAT…look PBT…it has halved 40pc compared to last quarter. Also comparing to last year’s quarter, no significant change.

Q4 FY20 Earnings call Transcript still not submitted/uploaded by company.

It is uploaded. Check the link:

2 Likes

Shree Pushkar looks interestingly poised due to a confluence of factors 1) nearing completion of capex cycle of 108 cr - fully funded through internal accruals, 2) favourable tailwinds for textile & fertilizer companies, and 3) attractive valuations.

The last fiscal saw a slowdown in the growth trajectory of the company as the main unit was being revamped. This is now completed, and the company has also integrated the two fertiliser companies it acquired (Kisan Phosphates and Madhya Bharat). The company remains debt free and has a cash surplus of ~50cr as of Sep 2020.

The recent Q2 con call was the most bullish I have seen the management in the last few years of tracking the company. A few highlights:

Comments on industry dynamics and demand environment

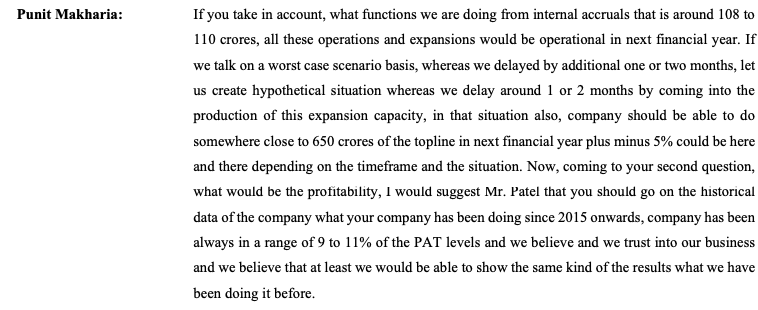

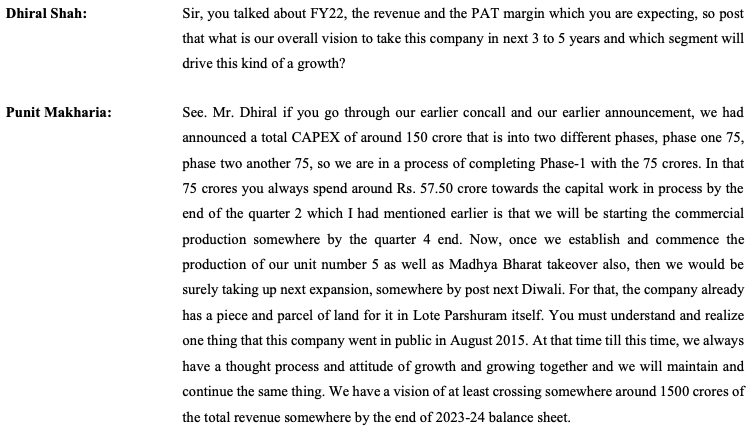

Guidance for 650 cr turnover and 10% PAT margins in FY22 (2x of FY21)

3-5 year vision and second phase of capex plan to reach 1500 cr topline

The company is currently trading at ~12x FY21e p/e, below its historical average of ~15x and significantly lower than leaders like Atul, Bodal and Sudarshan which trade at ~30x p/e. On an FY22 basis it is trading at 6x p/e assuming the company achieves the guidance of 65 cr PAT.

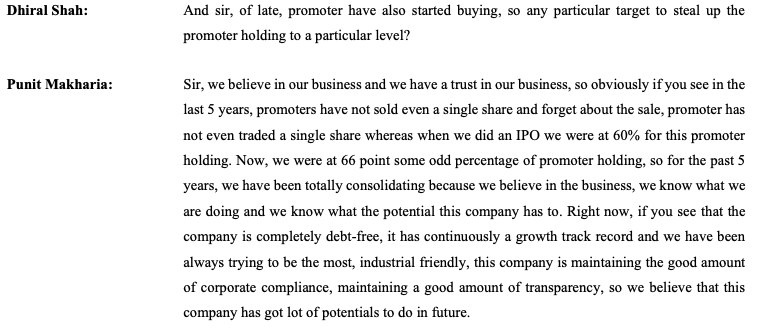

The promoters have been steadily acquiring shares since the IPO and have bought over 500,000 shares in 2020.

disc. Tracking position

7 Likes

Further buying by promoters… Promoter holding up from 62.72% to 66.50% in last 3 years

also,

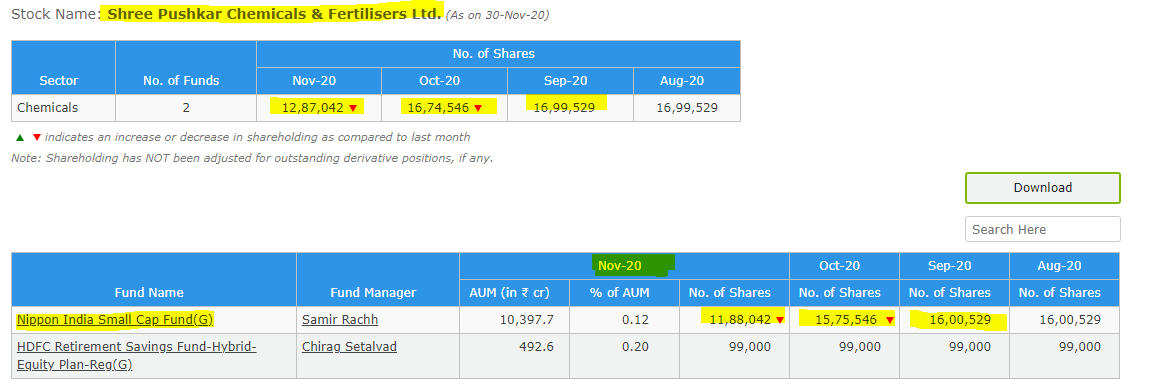

Reliance fund making full exit, this above, as per Nov20.

1 Like

I agree with your view.

Any idea regarding the dividend payout? Are they planning to increase it in the near future?

1 Like

Unlikely. This is a growth co and a good capital allocator, so it is better that they reinvest.

2 Likes

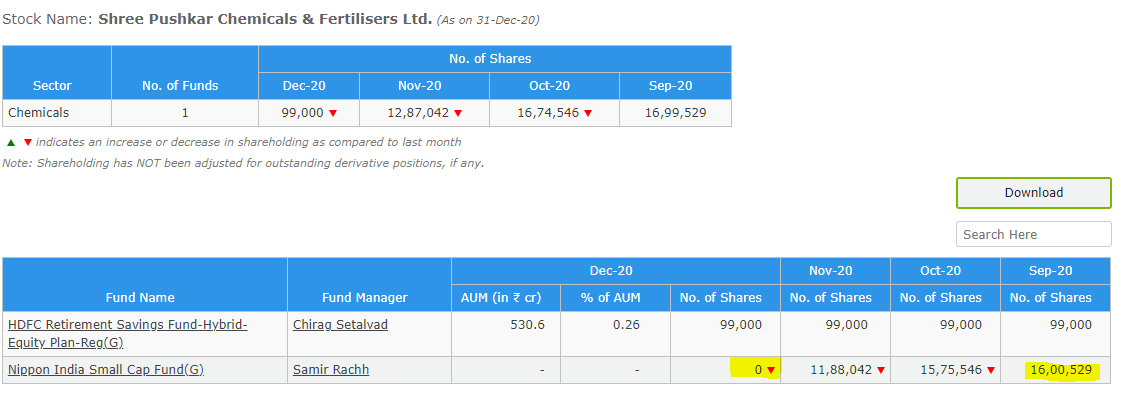

thanks for pointing this out RC…it seems that Reliance has made a complete exit given the high volumes in the first week of December and abundant availability at 100-102…I believe Makkya Jr (Gautam) bought 1.3 lakh shares during this period…stock has bottomed out

1 Like

On a related note the way Reliance/Nippon has exited this scrip is a sad testament to the lack of accountability in the Fund management industry in India.

Some background: Reliance Mutual Fund took a 5-6% stake at the time of the IPO along with small amount of subsequent buying. The scrip listed at 65-66 in 2015 and was at 320 at the peak of the last bull run. Reliance Mutual Fund has held the scrip throughout the last 5 years and sold it with a vengeance in November-December 2020 knowing the promoter is buying on the opposite side.

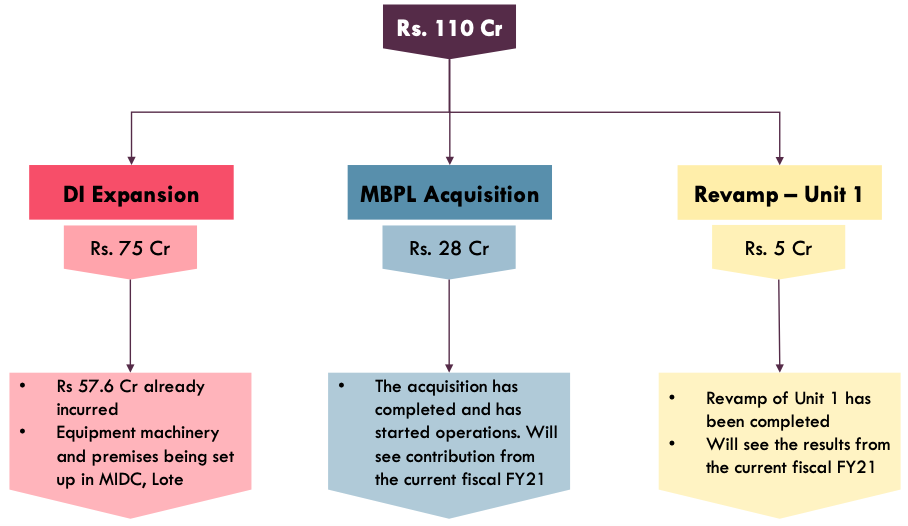

Anyone who has studied SPCL knows that the promoters are sharp capital allocators. Their earlier acquistion Kisan Phosphates had a payback period of less than 2 years and they acquired it by issuing shares (priced at 200+ at the time). Even the latest acquisition of Madhya Bharat Phosphates, acquired through NCLT at 28 cr, appears to be a shrewd one. Additionally the company has completed a CAPEX of 75 cr and has another 75 cr CAPEX planned next year.

Coming back to the original point Shree Pushkar was a low hanging fruit at 100 (mcap 300 cr) and the price of exiting will be paid by the unit holders of Reliance/Nippon over the next few years (as I write this the scrip has moved up by 30% within a fortnight of Reliance finishing its selling). This lack of accountability is not unique to Reliance but is characteristic of the entire fund management industry. The mutual fund industry is a wealth transfer mechanism from the middle class to the rich.

Cheers!

9 Likes

The last two years have seen steady accumulation by promoters and DII while Retail Shareholding is steadily going down. Usually, such a pattern leads to outperformance in the near future. Infact there are traders who look for these holding patterns as much as charts before investing, and for good reason!

4 Likes

Thanks. Looks like a lot of supply was absorbed last month. Where do you get this data?

1 Like

Rupeevest website. .

2 Likes

I went through all recent conf calls, investor presentations and annual reports and would like to share some points that stood out:

Positives:

- Highly undervalued given strong capacity additions and expected revenue to almost double to 650Cr in FY22. Current Price to Sales in a meagre 0.60!

- Good financial metrics: negligible debt (only small short term/working capital loans); interest coverage ration at 19.8; paying taxes at ~26%; NPM has been consistent around 10% and better than Sudarshan (7%) despite cyclical industry; CFO last 10 years is 1.3x of PAT

- Strong balance sheet with ~Rs 59cr held in financial investments (17cr MF + 42cr in Bonds) and available to invest in future growth without need to take on debt.

- Company has been aggressively pursuing growth both by adding capacity & also inorganically and mostly funded by internal accruals and without significant equity dilution since IPO

- MD & Chairman only 50 years old and appears to be very hands-on (e.g. answering most questions himself in conf calls). Joint MD (brother) is 47 and so far no apparent succession issue or family fued.

- Consistent promoter buying from market. Interestingly, it appears Mr. Gautam Makharia is increasing his stake to level up with his elder brother Punit.

Concerns/negatives:

- EBITDA margins at Kisan continue to decrease instead of improving even after the addition of 100 TPD Sulphuric Acid plant along with the 750 KW captive power? Margins were 16.6% in FY19, 15.1% in FY20 and 12.4% in H1FY21

- Working capital: worsening trend from 79 days in FY17 to 99 in FY20. 5 yr avg at 87 - lowest amongst peers. Due to lowest payable term (47 vs 60+ for peers). Moreover, 5 yr sales CAGR at 3% vs receivables at 6% - so rcvbls growing faster than sales. This is probably due to increased contribution from Fertilizer segment and related longer payment cycles (subsidies).

- Slow recovery in Dyes/textile market(Q3/Q4 21). Recent runup & positive buzz in textile stocks may indicate to demand pickup.

- I feel management has been hesitant in disclosing commercial info. E.g. customer names, geographical breakdown, market share, Dyecol sales/growth breakdown, etc. They answered only vaguely in recent calls o questions raised around this.At the same time peers such as Sudarshan & Bodal seem less hesitant to share such info. Could it be due to sensitivity because of Huntsman issue?

- Related Party transactions: Rs. ~4.8cr RPT excl. salaries etc. pa or ~12% of PAT. For instance, 0.6cr rent paid to mother (Bhanu), payments to spouse of Director (Ms. S Mahapatra), etc. - refer attachment. Moreover, 6.4cr loans given by MD & jt MD (3.6cr interest-free loan from Directors and 2.9 cr from inter corporate deposits (AR20 pg 109, 165)). I will however not rate them as a major red flag yet given it is still fairly a newly listed company and expect they improve on his front with time.

- Poor monsoon forecast causing Fertlizer demand (area sowed) to dip. Is there any good website or resource to track this variable?

Indicators that will help solidify my conviction:

- Trial batch runs in Unit 5 starts by end of Q4FY21

- Improvement in Kisan Phosphate operating margins from 12.4% to around 15-16% in next 2-3 quarters

- Q3 and Q4FY21 revenue to come around 100cr as management has guided for FY21 to come close to FY20 sales despite Q1 being a washout

Any counter / supporting views on above mentioned points highly welcome!

Discl: SPCFL forms ~3% of my portfolio and holding/adding since 2017

RPT_Sep2020_Q2FY21.pdf (1.0 MB)

11 Likes

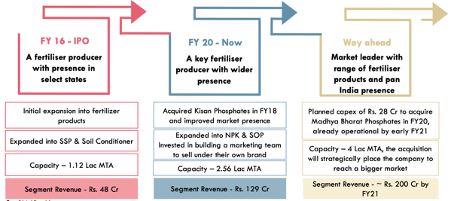

I have been studying the Fertilizer segment (specifically Single Super Phosphate – SSP product) of Shree Pushkar and highlighting some findings below. I believe the scale of this segment of Shree Pushkar is not fully appreciated yet. The company initially got into Fertilizers as part of their backward integration and “zero discharge” strategy, but now with the acquisition of Kisan Phosphates and Madhya Bharat the segment has now become a full-fledged vertical at par with their Dyes and Dye Intermediate segments. From a marginal SSP player in FY16 at the time of the IPO, Shree Pushkar is now probably the 4th largest SSP manufacturer in India after Coromandel, Khaitan and Rama Phosphates.

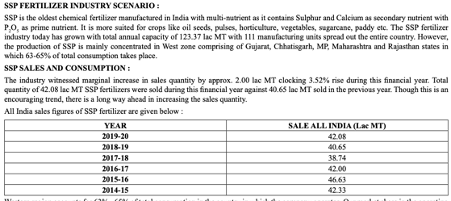

First a quick look at the Single Super Phosphate Industry:

Extract from Rama Phosphates FY20 Annual Report:

Total All-India sales of SSP in FY20 was 42.08 lakh tons.

The demand for SSP within the fertilizer industry has been increasing. This is well explained in the Khaitan thread by @RajeevJ:

The primary reason for the continued improvement in performance is due to the change in Govt policy in the distribution of subsidy. It has now kept the subsidy for the SSP sector separately within the overall Phosphates & Potassium segment. This has led to faster disbursement of subsidy & improved liquidity & made a material difference to the working of the SSP fertilizer companies.

The Govt. has further initiated the process of Direct Benefit Transfer , linked to Aadhar for payment of subsidy directly into the farmers accounts. This process should be completed sooner rather than later as is being done for various other Govt. subsidies. As & when that happens, it would be a watershed moment for the fertilizer sector as it would mean that these companies would get the full value of goods sold directly from the consumer & not wait for subsidy from the Govt. It could potentially re-rate the entire sector. The subsidy would be a matter between the Govt. & the consumer. The farmer will know the true value of what he is buying. The subsidy bill too would come down meaningfully as currently there is no incentive for manufacturers to produce efficiently & modernize their plants.

The H1 FY21 sales of SSP for players like Coromandel and Khaitan Chemicals have been excellent and bear this out.

A recent news article indicates that demand for SSP in H2 FY21 will increase to 25 lakh tons from 17 lakh tons in FY20 (+47%)

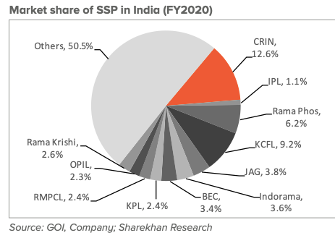

Who are the Key Players in the SSP Industry?

Coromandel is the largest player in SSP in terms of sales (Khaitan claims to have the largest capacity). The next two major players are Khaitan and Rama Phosphates.

Below is the SSP sales comparison for these 3 players in FY 20:

Coromandel - 5.7 lakh tons

Khaitan - 4.0 lakh tons

Rama Phosphate - 3.69 lakh tons

Shree Pushkar Fertilizer Division

As mentioned earlier, Shree Pushkar started manufacturing SSP as a backward integration strategy but in the last 3 years has made 2 acquisitions (Kisan and Madhya Bharat) to establish this as a standalone vertical.

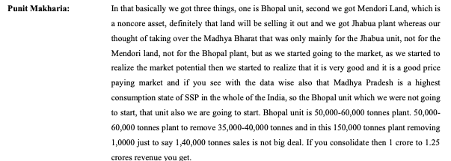

Below is some colour on Madhya Bharat from the Q2 FY21 concall:

What does Shree Pushkar’s Fertilizer segment look like post this acquisition?

- SSP capacity doubled from 2.0 lakh tons p.a. to 4.0 lakh tons p.a

- This puts them in 4th place in terms of operational capacity:

o Khaitan Chemicals - 11.1 lakh tons / year

o Coromandel - 8 lakh tons / year (estimated)

o Rama Phosphate - 7 lakh tons / year

o Shree Pushkar - 4 lakh lakh tons / year - Based on management comments (shown above), they expect to more than double SSP sales from 1.25 lakh tons in FY20 to 2.60-3.05 lakh tons (65%-75% capacity utilization). This can put them in 4th place in terms of sales:

o Coromandel - 5.7 lakh tons

o Khaitan - 4.0 lakh tons

o Rama Phosphate - 3.69 lakh tons - Become a pan-India player with presence from Western UP in the north, through Himachal Pradesh, Haryana Rajasthan, MP, Chhattisgarh, Gujrat, Maharashtra and reaching right up to Goa and Karnataka in the south.

- Key player in MP which is the largest SSP market in India

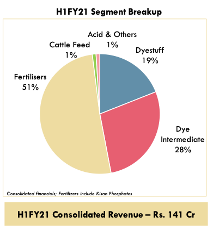

Madhya Bharat sales of 5.11 cr in H1 21 have not been included in the consolidated results of the company as yet and should be included from Q3 onwards. As seen below, the Fertilizer segment is already contributing significantly to the overall revenues of the company and is expected to generate 200 cr+ of revenue annually from the existing asset base going forward.

Disc. Invested

12 Likes

@enelay Very good write-up on fertiliser sector. What is status of Direct benefit transfer to farmers instead of paying subsidy to fertiliser companies?