In the meanwhile, gov is apparently already trying to address the subsidy issue within the existing framework:

In the stimulus 3.0 announced on November 12, the Centre has made an extra provision of Rs 65,000 crore for fertiliser subsidy for FY21, over and above Rs 71,309 crore budgeted. This will ensure that entire subsidy dues to the fertiliser companies, including `48,000 crore arrears, will be cleared in the current fiscal.

This is an unprecedented step, as a major part of subsidy for any year used to be released in the subsequent year/s, leading to liquidity problems for the fertiliser industry and shortage of fertilisers in many parts of the country. Given the agitation over the farm Bills, and the fact that the agriculture sector is proving to be silver lining on the cloud of economic slump, the government can’t afford paucity of fertilisers in the rabi season.

Hi, Can someone comment on what is the impact of Dye / Dye intermediate industry due to Chinese factor. I have read some articles / news about factories closing in China due to environemental impact in dye and dye intermediate industry. However, I couldn’t find any further updates / news around this.

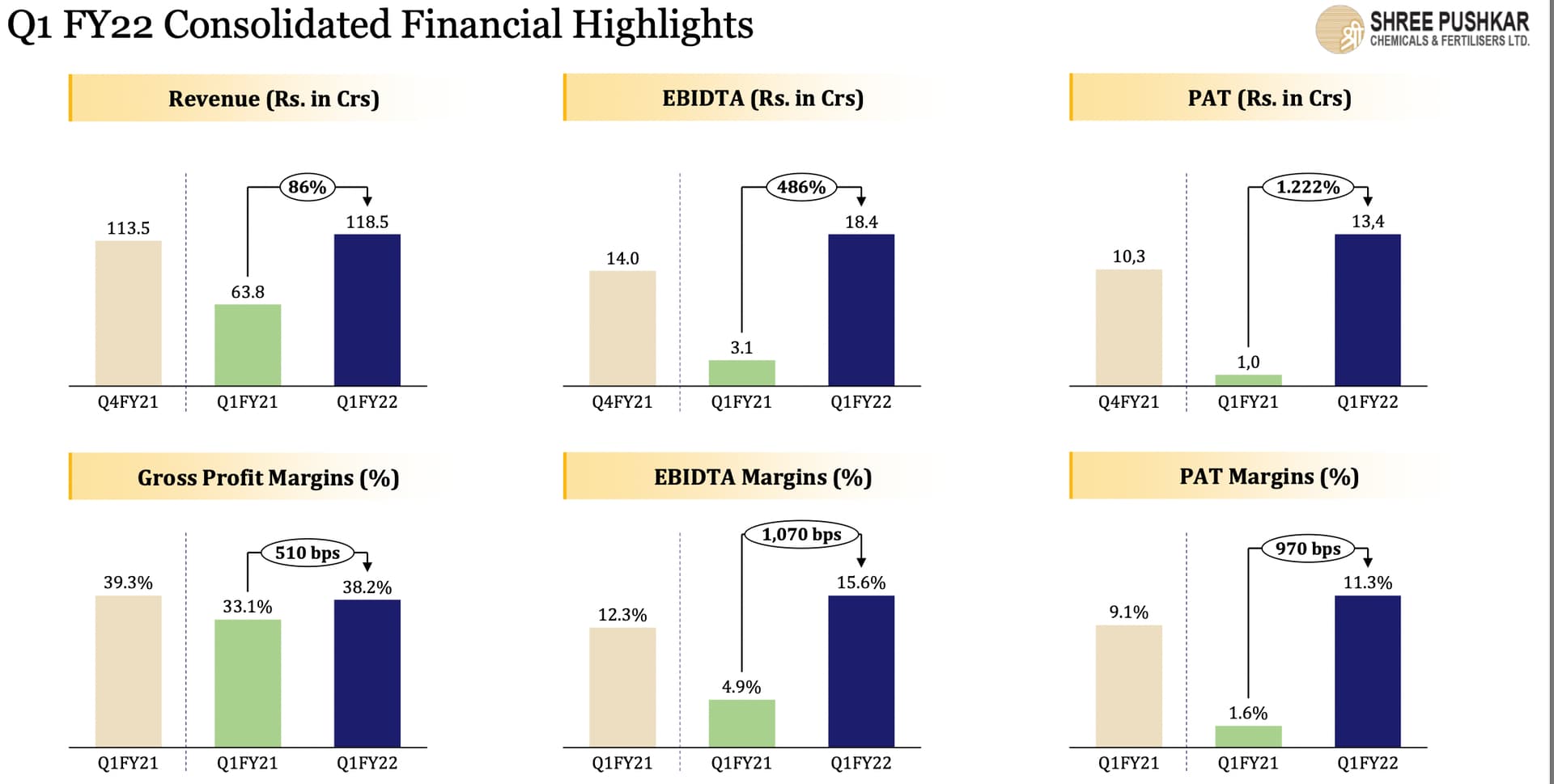

Results out. First impressions: Looks like the business is getting back on track - highest revenues in last 6 quarters. Sharp increase in Other Expenses however, need further clarity on this from the company.

Bullish comments again by management on today’s con call. Did not take notes so just jotting down the points that I recall:

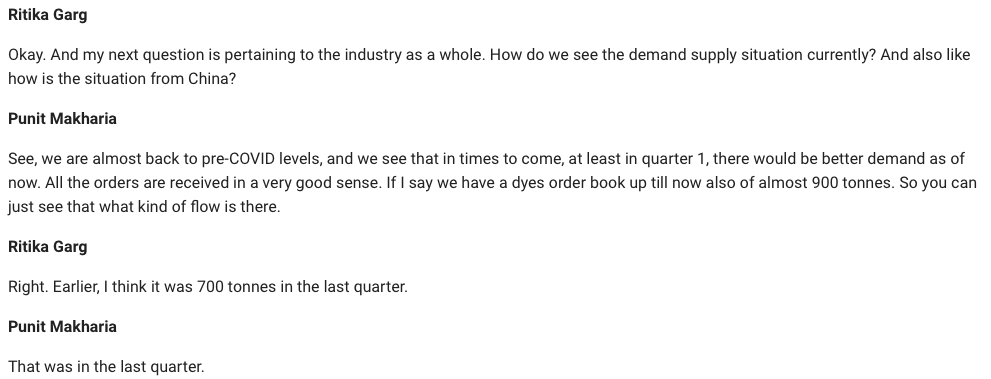

Seeing a V shaped recovery in demand. H Acid & Vinyl Sulphone prices are up 5-10% currently from Q3

Unit 5 will be commissioned during Q1Fy22 and will have 3 full quarters of production

Reiterated top line guidance of 550 cr - 600 cr “conservatively” for Fy22. Margins should be similar to previous years

Currently have ~50 cr in cash. Have given a mandate to a consultant to scout for M&A opportunities

Confirmed that Pushkar is now one of the top 5 SSP players in India by operational capacity

Reasons for increase in other expenses - inclusion of Madhya Bharat, continuing high labour & freight costs due to the pandemic, one off costs for restarting operations. These expenses should normalise soon

Gov has not released subsidies yet for their segment since Sep 20. Around 20 cr of subsidy is approved and pending disbursal

Will announce further expansion plans later this year

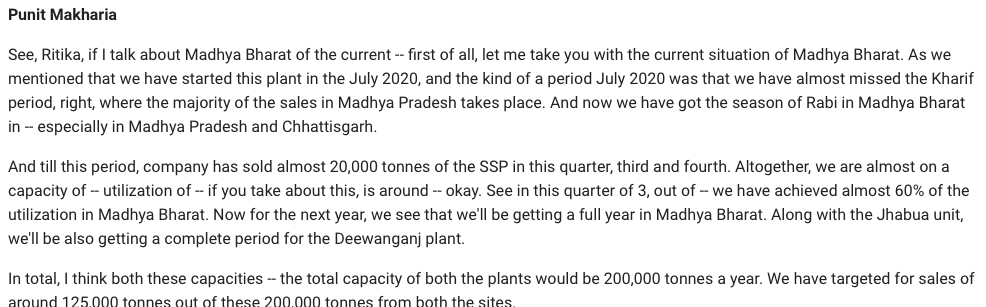

Madhya Bharat results: In Q2FY21 concal management had stated that they sold 25,000 MT of SSP from MB from June 6 to Sep/October However, in the latest earnings presentation they state 20,000 MT sold only from July to now?

Q2 call, Nov 2020

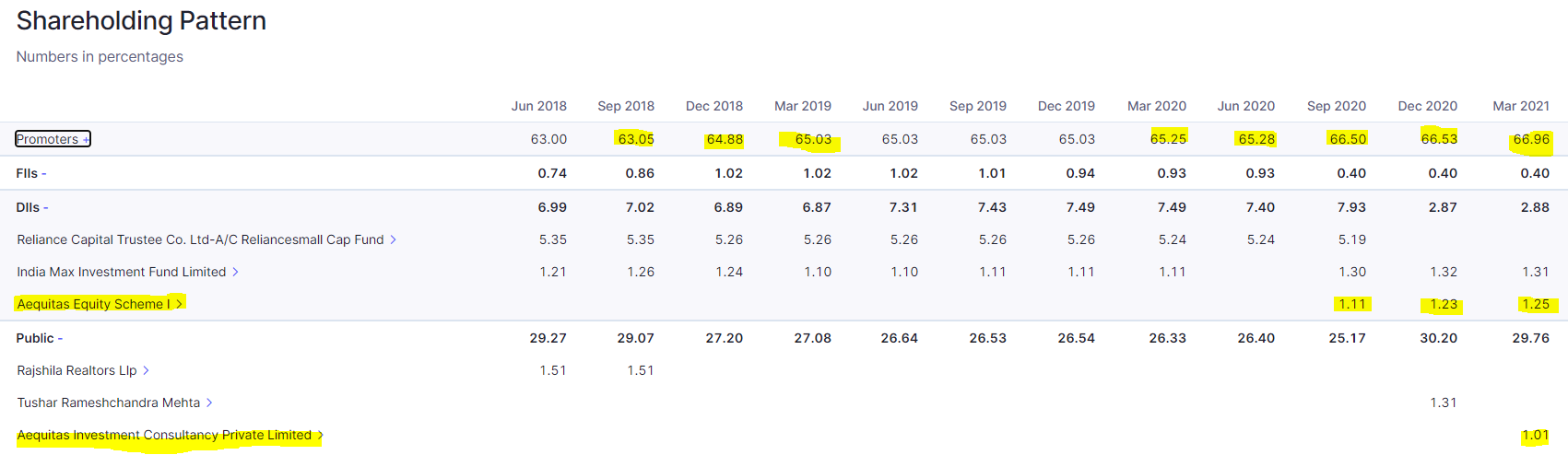

Updated shareholding pattern. Promoters increase stake again. From 63% in Jun18 to 66.69% in Mar21. Reliance MF exits, Aequitas Funds enters. Aequitas is known to pick out real winners.

Severe cyclonic storm “Tauktae” caused damage to the factory sheds resulting in temporary production halt in Units 1 to 5 at Ratnagiri plant. Production is partially shut. Adverse impact on company’s operations is not immediately assessable.

Good interview with Punit Makharia. They are targeting 550 cr revenue and 50 cr PAT in FY22, and 650-700 cr revenue in FY23. Still trading at reasonable valuations in this frothy market.

This is one of things that I don’t like about the company. They claim that they have sufficient internal accruals to meet all Capex requirements but then keep issuing warrants together inject money that is not needed. Isn’t this reflective of shareholder unfriendly behavior by the promoters?