Read the whole thread to understand business model

Ogilvy has helped to build some of the most recognizable brands in the world: American Express, Sears, Ford, Shell, Barbie, Pond’s, Dove, and Maxwell House among them, and more recently, IBM and Kodak.

3 Likes

An interesting article about Kranti Gada.

The article gives good insights about how management thinks about devloping new leaders in the company. From hiring employees from cos like Viacom, Jio, Zee to employing managment trainees from IIMs, it does seems that managment wants to have good talent in the company. Also, the last statement from the interview of going directly to the customers instead of a platform is pretty interesting.

4 Likes

Thread on recent actions happening in music streaming space. JioMusic merging with Saavn with combined entity valued at $1Bn. Reliance betting big time in this space.

Regards,

Suhag

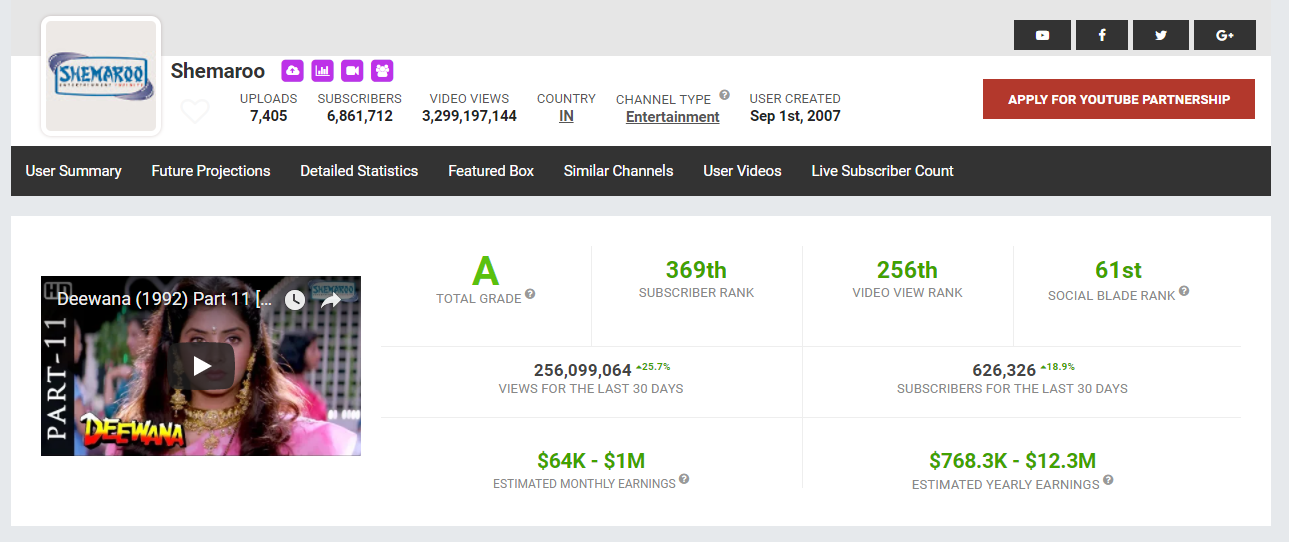

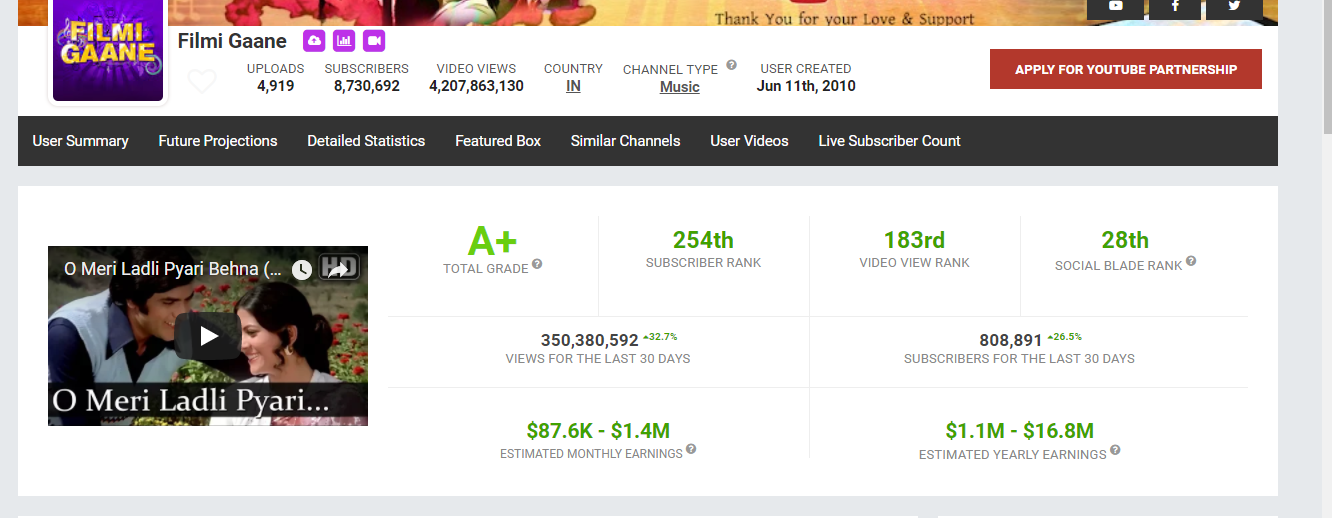

The above stats are for filmigaane and shemaroo channels from socialblade.com

Look at the pace at which the subscriber nos. and views are compunding every month (filmigaane views compounding 32% and shemaroo 25% M-o-M)

Last year around this time they had cumulative views of 3 Bn and 2 Bn , at the current run rate the channels will do that every 8 months and the views are still accelerating!.

My thoughts in no particular order

- CPM rates might not reach earlier high levels again as the new viewers drawn in by the cheap internet are not the earlier ones who where urban/higher income/middle class salaried.

But they might increase from current levels as online ad budgets catch to cater to these new audiences, hence advertisers might pay less for ad display as these might convert to sales less often.

2)There is a dearth of content for these new viewers and even youtube channels like TVF and AIB do not cater to these audiences (The shows like pitchers, tripling etc. are clearly aimed to towards the urban middleclass)

3)Vast majority of Indians are entertainment starved with low theatre penetration(Compared to other countries), Low availability and affordability preventing home entertainment such as dvds and vcds from sating the need.

4)Netflix content wise does not sate these Mass Indian audience( content is probably relevant to less than 5% Indians) and is priced out of most of Indias reach.

Amazon prime while reasonably priced is better in the content front with regional movie offerings, but its original content is again catered towards the urban middle class.

Balaji telefilms targeting I think was spot on in their targeting in their AR:

“While, there is a plethora of content available on digital media, today. Most of it is foreign content or

content duplicated from existing television shows or content addressed to the English speaking, urban, educated, millennial population. There is a dearth of original content, which will appeal to different age groups, socio - economic strata and to the millions of new Indians residing in the category B/C towns of the country. It is this gap, which ALTBalaji is gearing up to fulfill. Firmly rooted in Indian-ness, this sort of content will transcend the barriers of age, class & location; where there will be something for everyone in their language of choice”

Or as I saw Ekta Kapoor put it as such : they are “targeting audiences between Narcos and Naagin”.

The Narcos watchers being an insignificant no., but those who are willing and have wherewithal to pay. The Naagin watchers already being catered to on TV , being geared to families and show format itself not necessarily amenable to binge watching.

- shemaroo+ balaji should be a nice combo to ride this theme of catering to this market , with allocation based on what one is more comfortable betting on , shemaroos library distribution model or balajis content generation and b2c business.

disc . invested in both

3 Likes

Dear members, inventor days & cash conversion cycle is increasing yoy (on ratestar). Which means inventory is getting piled up.

3 Likes

Has anyone tried building a simple pricing model which can forecast the top line

Keshet International inks in-flight deal with Shemaroo subsidiary to cover ME airlines

Brokered by Keshet India, this distribution deal will see Contentino Media(Shemaroo Subsidiary) exclusively represent KI’s finished tape catalogue to its client-base of more than 50 airlines operating across the Asian and Middle Eastern regions, including Singapore Airlines, Emirates and Jet Airways.

1 Like

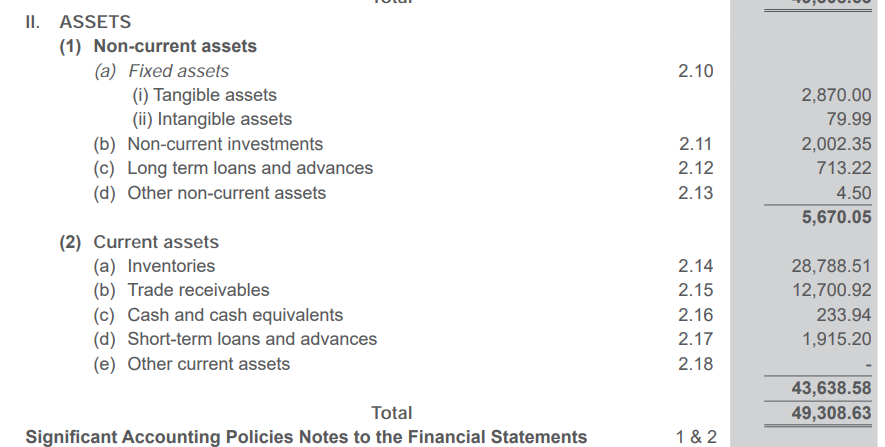

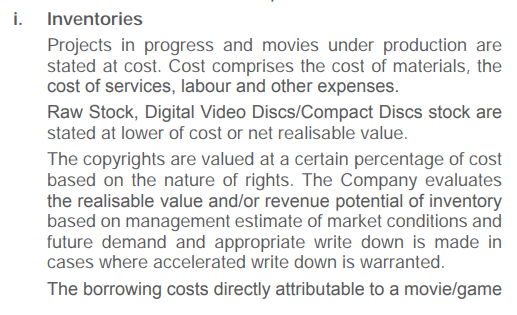

Can anyone here help me understand why Shemaroo considers Copyrights, Movies under Production (Essentially WIP) and DVDs as Inventories? The way I see it, since these Copyrights and DVDs allow them to earn cash flows over a long time period, they should be classified as Long-lived (Fixed) Assets (Except for the WIP, that’s fine). This weird classification distorts their Working Capital-related calculations such as Inventory Turnover and Cash Conversion Cycle. For a content company, understanding these Ratios become very important and it does not help that the company’s Accounting policy stands in the way.

In fact, if you look into the Assets of the company, it’s even more daunting:

Break-up of Shemaroo’s Assets:

- Fixed Assets (10%): Buildings, Fixtures and Intangibles

- "Copyrights" and others (57%): Valued by the management itself, based on their own estimate. No visibility of real value to the public.

- Trade Receivables (29%)

- Others and Cash (4%)

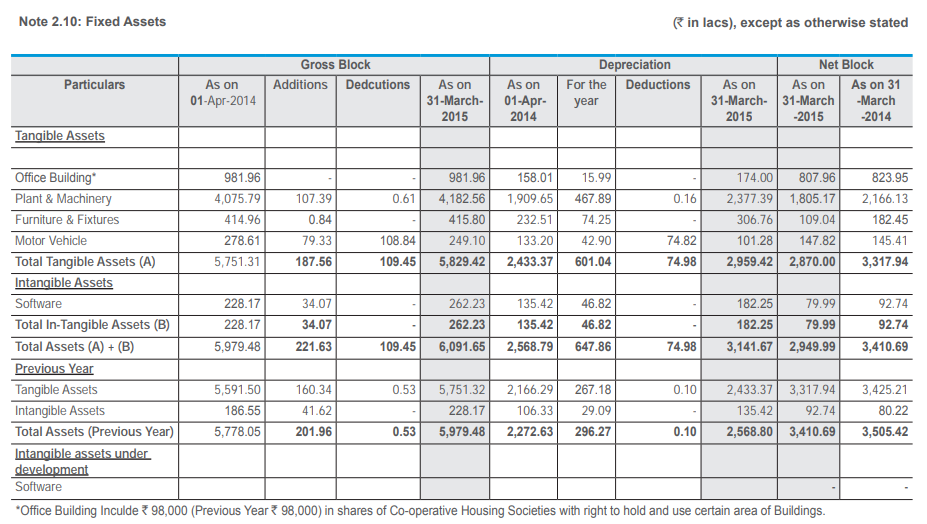

1. Fixed Assets (10%)

I fail to understand why a content based company needs a 10 Cr Office building and 40 Cr worth of Plant and Machinery (Again, we are offered no further insights into what is actually Plant and Machinery). ‘Tangible Assets’ make up of 50+ Cr , but there is no mention of what those Assets are. Software is worth 22 Cr.

2. Copyrights and Others (57%)

Further, a bulk of the company’s Assets is in ‘Copyrights’ (About 57%), whose value is entirely dependent on the management’s own idea of how well they are able to monetize these copyrights. This is their accounting policy. Does anyone have a logical way of understanding how we can manually calculate the Value of these Copyrights for our own verification? I see no way to do that.

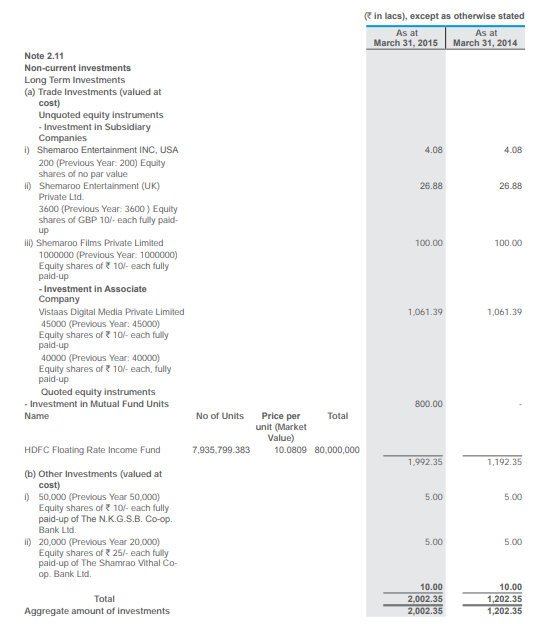

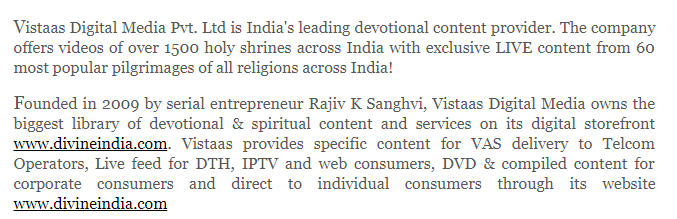

The other long-lived Assets include Investments in a subsidiary called ‘Vistaas Digital’.

The subsidiary supposedly sells divine digital content:

But the domain Divine India is unregistered:

If a content-based subsidiary has not registered and so, not doing business via the domain mentioned in its own website, how is it worth 10 Cr at all?

3. Trade Receivables (29%)

Almost 50% of Sales is stuck in Trade Receivables. Why is this the case?

I’m just trying to play the Devil’s Advocate here. Any answer to any of the above questions would be useful.

8 Likes

Appreciate your efforts and comment on Shemaroo. While most of the points valid, I would suggest you would get some of issues clarified by reading the thread. In fact, Dhwanil note on Shemaroo and also many past posts dealt with inventory valuation and working capital intensive nature of the business.

Let me also try to address the concern your raised to best of my understanding. Do look forward to revert on same.

- Why company need fixed assets in distribution business and plant? Well the company also in business to improve the old content in film moving into digital space, plus adding feature of Dolby sound, improve quality of print in digital medium and, above all, converting wherever possible in HD equivalent formate. That would require studio which I believe is essential and core capex. Find enlcosed link which provide more detail about what Shemaroo do in its studio. http://studio.shemarooent.com/Index.aspx?pg=serv_digi_film_res

Having said that what shall be cost of such studio, I do not have perfect answer to same.

- Your concern is valid that there is no independent asseseement for valuation of key component inventories. Having said that, the current acquisition of liberary of peers (like Eros liberary acqusition by Reliance group) and also recent deal and company conference call does give indication in increase in the cost of digital rights significantly over decade. Dhwanil note specifically address that issue.

On Vistass Digital Media, it is very valid concern that domain not being registered. However, as the website suggest, the company is associate and Shemaroo has investment with Hiren Gada as director on the company. Even so be the case, non- registeration of domain is not good sign and appreciate your efforts in highlighting same.

On Trade receivable, there is detail disucssion on conference call and also on this thread in past. I suggest you read whole thread, or specifically Dhwanil Note which provide great insight. After reading same, you still have concern, please make effort to pen down.

Thanks once again for good efforts.

Discl: I have invested in the company for more than year and my view may be biased due to my investment. Investor shall do his/her own due diligence before investing.

3 Likes

Q$ results Snapshot

consolidated Revenues up 20% Yoy

consolidated EPS 37% yoy

Operational expenses have comne down from corresponding quarter significantly

Trade receiveables came down significantly.

Debt reduction seen

1 Like

Thanks a lot. Dhwanil’s note was indeed enlightening. My queries are as below:

-

Management has given clear guidance about why inventory has been ballooning (Indeed, Inventory Turnover has dropped drastically and Inventory Days is almost 1.5 years now). But my major contention was with the Value of these “Inventory”, which is completely lost on us. Even Dhwanil’s note vaguely talks about Economic Value, but I personally don’t see any way to pin a number on this. But one test is waiting and seeing if the Managenent’s guidance of reducing inventory and trying to convert them into Sales actually works out. After all, Cash is king. A company cannot afford to be a Run, Baby, Run company.

-

This is how Shemaroo’s Office Building looks like (Google Maps Link). Since Land is reported at Cost, one has to see when this land was acquired and check out property prices in East Andheri at that point and arrive at a rough estimate. I have no clue here, so maybe some native residents of Mumbai can try this exercise. Regarding Plant & Machinery, only insiders in the content creation/distribution can help us understand if they actually cost this much.

-

My contention is that it says right there in the Vistaas homepage that they sell all their content through Divine India. But Divine India is an unregistered website, meaning nothing is being sold through the website. How can the value of a company which sells nothing be 10 Cr?

One positive note I’d like to add is that, something I usually check is the employee’s comments about the company. Shemaroo’s Glassdoor site has some very good reviews, with only one being a very negative review.

Find enlcosed my response to your points.

- This is business risk. Either you trust management or do not trust. It is finally an individual investor call.

- I feel just valuing fixed assets in growth business is not helpful particularly for service industry. Office industry value may range from say Rs 10-50 Cr (my guestimate without even knowing anything about real estate). When market cap is around Rs 1200 Cr, I would not like to focus on asset valuation. This is my personal view and each member can have their own opinion which may be completely opposite to my view.

- I think the company distribute content throug DTH services (like religious channel on DTH TV), or on mobile service platform on Reliance JIo/Airtel and YouTube. While not sure on this, I do not see subscription/ad driven business for online streaming of live darshan in my opinion on Divine India. My understanding might to wrong here as well. Enclosing YouTube link for channel.

https://www.youtube.com/channel/UCzszIh4jH06kYp7k_DxhH5A

Finally, investor need to develop understanding of business/management and also valuation. What is good for one investor may be bad for another investor. One need to undersatand risk return profile while investing.

Discl: My view may be biased due to my holding. Investor shall undertake their own due diligence before making any investment decision.

1 Like

Agreed on the other two points. Regarding Vistaas, it says right there on the website that they sell content exclusively via Divine India, which is an unregistered and hence, non existent website. How can a non existent website be valued at 10 Cr, was my actual question. This bring the integrity of the management into question.

I think the first point is also applicable to third point. You trust/distrust management for business. We have universe of 5000 stock to invest in India.

Valuing a non existent company at 10 cr is not a business risk. It has nothing to do with understanding of the business. It’s outright fraud. Maybe it’d be interesting to ask the management this question on the next Concall.

Fair point, if you feel not comfortable, please do not invest. However, without putting efforts to even read whole thread and passing glaring statement is unfair in my opinion. All of us here are suppose to read full thread and then ask specific issue which can be discussed.

Further, please understand, the company is already is existence. The website of the company to sell content is missing. In my understanding, company does not intend to distribute content at this point content over web and get adv/subscription revenue. Also, when Siddhiviyak/Shirdi Saibaba and many such website are streaming content freely, I do not potential for distribution on web. In fact, it might be possible they may distribution right of streaming on dedicated channel (Hathway Mumbai cable has Divine channel and likewise Tata DTH and other operator also have paid channel which stream various temple live streaming) Hence, not registeration of domain is not so high risk in my opinion. That does not mean you could not have different view. However, I feel it would be appropriate to put some more efforts before calling outright fraud.

Find enclosed link for Hathway and Shemaroo deal for Video on Demand for Om Shakti Channel

1 Like