-

I made no comments about whether or not I’m going to invest in the company. Assuming such a thing and providing advice on that basis is unfair in my opinion. At this point, my research in the company is purely academic.

-

Nowhere in the thread is the issue with Vistaas Digital mentioned.

-

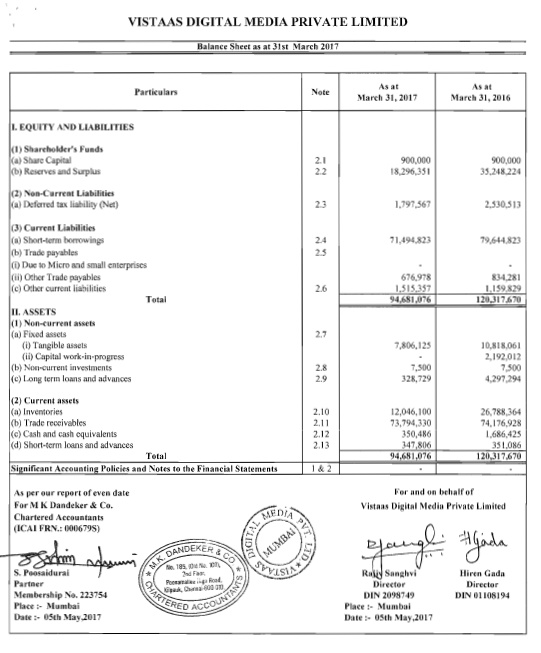

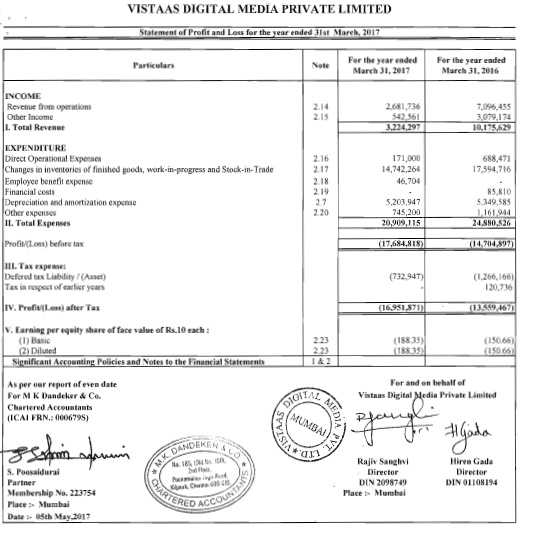

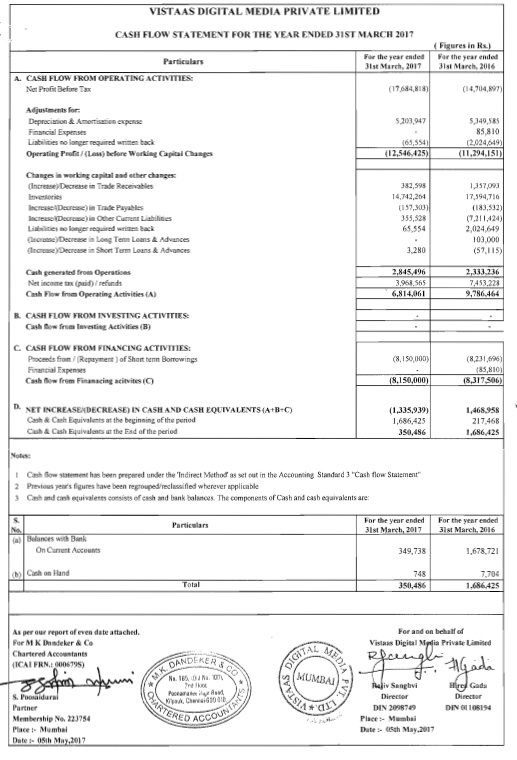

I did not doubt if the Shemaroo itself owned Divine content. They very well may. I doubted the integrity of the management which says they have invested in a company named “Vistaas Digital”, which supposedly sell all its content through Divine India, which is a non existent website. Even if the website was a mistake, why continue to show the Value of 10 Cr in the Balance Sheet specifically under that name itself?

1 Like

@dineshssairam divine India may not necessarily be a website. There is a YouTube channel divine India, section in Amazon and iPhone app in AppStore called divine India.

-

Point well taken. However, you are raising valid concern and my limited suggestion was that in case you are not comfortable with the company and management, please do not invest. I feel, irrespective of whether you invest or not, that is generic advise. Also, I appreciate you point and apologise.

-

There are another couple of business like US Subsdiary and also company for distribution content in airlines. So rather then looking for each business, in my opinion, one need to understand that shemaroo in busniess of distribution of content digitally. There are various arrangement and association for same. Bringing Vistaas concern is valid, but have you read whole thread? I am yet to get answer on same. Had you said that I have read whole thread and raised specific query, it could have been different discussion.

-

I felt the language you use in previous message was bit harsh.

Having said that, your question on Vistass resulted in some work from my side. I am encloding same for benefit of all members.

So the concern of yours whether, the company deserve valaution of Rs 10 Cr or not is valid in my opinion. The company is reporting net loss which mean Shemaroo shall have write down the valuation in my opinion. Having said that, it would be good also to understand the otherside view point as well.

Thanks for bringing out valid concern. We may agree to disagree but I would still suggest careful choice of word. Hope this lead to more meaningful disucssion and better pespective about the company on the thread. ![]()

16 Likes

Sorry for the late response. I guess I’ve been misunderstood out for context. I didn’t say Shemaroo’s management is a fraud.

I mentioned that in case it’s found out that Divine India actually doesn’t exist, it won’t have any relation to understanding Shemaroo’s business. It would be related to Shemaroo’s management being unethical.

Once again, I’m actively tracking Shemaroo and trying to understand their business model. I was playing the Devil’s Advocate to that extent. I did not mean to slander.

1 Like

“Gada also claimed that his upcoming application would be vastly different from Netflix in terms of both better online platform maintenance as well as imposing controlled spending on content. Shemaroo intends to increase its movie catalogue by at least 5% per year, and is thereby inclined to reach out and licence its library to other online platforms. Within the next 18 months, the library of Shemaroo Entertainment is expected to expand to such a great extent, that Hiren Gada is confirmed that they will be able to outsource their streaming platform in a monetized catalogue which will definitely ensure seamless streaming without any hitches.”

“Given the opportunities that exist in the market, we want to grow our revenue fivefold in five years,” Hiren Gada, the company’s chief executive officer, said in an interview in Mumbai. “The best way to play the digital boom is to offer services on all platforms in all forms.”

I think Managment is working in the right direction, as market demand for local & old content is huge, given the number of views they are getting on youtube, demand looks very robust but the problem with youtube is that ads revenue is shared 50-50 & shemaroo have no control/say in amount and type of Ads are being displayed.

So launching OTT service looks very good move and it looks low-risk high probability bet, if their app becomes successful they can further build on it and if it fails it won’t cost much as they are not paying for content, only app & basic infra cost which is very low these days.

Moreover, for start, I think it would be better to give the subscription-free app and better tie up with telecom & data service provider for revenue sharing also they can collect revenue from ad display.

the same kind of service is being offered by iflix.com, it very popular in Malaysia, Indonesia and middle eastern & other Muslim countries, they have tie up’s with all the major telecom player, and Telecom operators have special plans for iflix consumption.

Even in normal data bundle plan, some operator’s are giving iflix quota for free(whether customers want it or not, you will get the iflix specific quota) in order to promote the iflix, its very intelligent way of promoting the consumption, same can be easily done by shemaroo.

Disc: My views could be biased, Invested.

2 Likes

I love Valuations in general. And I love it more when I Value difficult-to-value companies such as this one. I hope I made logical decisions here. Comments, criticisms and feedback always welcome, either here or on the blog itself.

Thank you.

9 Likes

3 Likes

Strong results by Shemaroo in Q1 on consolidated basis

Revenue Grew by 18 % YOY

Profit Grew 22% YOY

even decent growth in QOQ basis as well

1 Like

Earnings Presentation and conference call details. https://www.bseindia.com/xml-data/corpfiling/AttachLive/38167f71-1943-413c-80d1-7b0a82b8888e.pdf

Note from AGM on September 11 2018, based on discussion with Board of Directors in reply to queries of various shareholders. Please note that Shemaroo is among my top 5 holding and my views may be biased. There is also possibility of some misunderstanding at my end while writing notes. Future investors are expected to do their own due diligence.

5X in 5 Years:

The Company did not answer specifically in figures about how it intend to achieve this target. However, it did not give some broad outline like customising content to various segment requirements and sweating the content library more effectively and slicing and dicing the market segment. For instance, while penetration of mobile in urban area is reached reasonable level, the next weave of growth would be driven by the rural market. The company intends to aggressively utilise its partnership and own content on devotional segment which it assume may have higher acceptance in rural/semi-urban market then metros.

Similarly, in order to improve understanding of NRI audience, it intends to go closer to the market which has high Indian Diaspora population. The new subsidiary to market content which focuses on North American market is step in that direction.

Further, the company also intends to develop market for content in niche segment like Airline industries where it has enter in arrangement with 70 airlines to content.

On specific query about YouTube growth in India, the company responded that they are among Top 10 viewed channel on YouTube in India and would continue to remain on YouTube. While, viewership on YouTube has gone up by almost 5x times in last 2 years, the advertisement spend on YouTube has increased only marginally. Having said that, YouTube Viewership in India has reached to around 30% of total Video viewership, hence it would be difficult for advertiser to ignore YouTube.

The company has recruited talented human resources which have expertise in various segments of media industry. All the new team members are working on developing new products for the market and addressing them with the company content. These new avenues would also contribute to the growth of the company. Average employee age 32 years which among lowest employee attrition rate in the industry.

The mobile internet user is currently at 25 Cr which is expected to increase to 50 Cr in 3 years and 75 Cr in 5 years. The increase user with technology, Video viewing is expected to gain maximum in media segments.

Content Library

The company has built sufficient content library. The company would continue to add content, same would be funded mainly from internal cash. Hence, the company library would continue to increase, but balance sheet would not be leveraged.

Use of Cash flow

After meeting content inventory requirement, the operational cash flow would be utlised to repay the debt. During FY18, the company repaid around Rs 70-75 Cr debt and Debt/Equity ratio is now at comfortable level of 0.35 times. The company would not increase dividend payment till it has large debt on balance sheet.

Key points from Annual report FY18

- Shemaroo’s ability to reinvent itself for over 50 years based on changing consumption patterns helps it to innovate and adapt to the ever-changing dynamic digital space and stay ahead of the curve.

- Shemaroo’s ability to understand the pulse of the consumption patterns has helped it become a trusted partner with almost all the major OTT players such as YouTube, Hotstar, Apple iTunes, Google Play, YuppTv, Vuclip, etc.

- From less than 10% revenue contribution in FY14, Shemaroo’s Digital Media Business has grown to over 25% revenue contribution in FY18. The company is aiming to increase this contribution to over 50% in the next 5 years with new, disruptive and future ready products and services catering to the new age digital consumer.

- Due to the fragmented movie production industry, Shemaroo adds significant value to both the

- distribution platforms as well as content right owners by bridging the gap. Shemaroo provides high quality content rights suited to the requirements of distribution platforms. The company is able to provide more value for money for the producers due to its expertise to maximise the monetisation potential of content.

- Shemaroo plans to increase its B2C presence amongst consumers in the next few years by offering innovative future ready products and services.

- Shemaroo is also looking to launch innovative B2C offerings in the international markets in the coming years. With a focus on the North American market, the company is set to open an office in USA.

- Before the launch of Jio, the average monthly data consumption per user was around 600 MB, which has grown to almost 4 GB per user per month in 2017. This is further expected to cross 18 GB by 2023.

- The growth of connectivity resulted in the proportionate growth of internet users to 481 million in 2017, of which 295 million were in urban areas and 186 million in rural areas. Approximately 30% were female users. Internet users are expected to cross 500 million in 2018 and reach 829 million by 2021. Rural Internet users are expected to grow from 38% to 52% of total base from 2017 to 2021.

- App downloads in India witnessed a 65% growth with the Introduction of Jio in Q4 2016. Entertainment apps grew 120% in 2017 and made up the 4th largest category.

21 Likes

Thanks Dhiraj for the summary.

Qn: In 2014, the size of their inventory was Rs 200 Cr. In 2017, it was 500 Cr. That was a 300 Cr increase in content in 3 years. In 2018, inventory size is Rs 529 Cr. The rate of content acquisition has come down drastically ( from Rs 100 Cr every year to Rs 29 Cr in last FY).

Given that they want to grow 5X in 5 years, is this level of incremental investment sufficient?

1 Like

Saw on a friends Instagram story that Shemaroo has the rights of Pyaar ka Punchnama. Must be limited to certain platforms only because the movie does not appear on Shemaroos YouTube page

Basically they want to showcase Zee Cinema and Sony Max wale movies on Internet, and public is going crazy after their shares. They are like this antique products seller …just because Antique can be sold online too, it doesn’t mean that underlying antique becomes valuable…yes for sure you get some more customers, when u operate an antique store out of 4 cities vs if u do so through online method, but in the end…there are many antique players, the customer set for antique won’t grow much and you are not doing anything to attract the modern art lovers (or doing it at such a slow pace, that the needle doesn’t move)

Think : If T Series was listed, would you have bought this stock of Tseries or Shemaroo.

Shemaroo shareholders might be suffering from availability bias,

Go to the YouTube pages of Rajshri, Ultra and Eagle…They are also doing the same thing as Shemaroo… Shemaroo is just another me too player with no special edge.

13 Likes

I second his opinion . Very valid points , i think audience is getting matured day by day , anurag kashyap and the likes brought out the movie industry from the stereotypes formula films which was prevalent in the industry from many decades . With avenues like Netflix,Amazon prime opening up such creativity will find more and more expression,acceptance and also appreciation . I don’t think the Shemaroo content will be popular in the long run

2 Likes

Shemaroo’s business model is unlike typical content owners. For Shemaroo “old content” does not mean movies before year 20XX. It just means that they acquire rights for movies in the second cycle (typically after 5 years of first release), which is a moving window. For example in 2018 they will acquire rights for movies in 2013 and in 2023 movies from 2018. Hence the content library keeps getting refreshed albeit with slightly older content.

Let me try to breakdown their content in two large buckets (omitting nuances for simplicity):

-

Perpetual content ownership: Shemaroo has ~3500-4000 (IIRC) perpetual movies library. This content arguably will become less interesting for new audience. However given the video consumption in India is still in infancy there is large latent demand which will ensure reasonable growth for many years (though likely slower than consumption growth for “new” content). A case in point is the monthly views on their YouTube channel which has grown 4x in last 2 years despite no change in content. Also most of this content has been written off from balance sheet and inventory hence the revenue goes (almost) directly to bottomline.

-

Limited rights content: As I explained earlier they continue to acquire “new” content by participating in second cycle and most of this content is limited rights (time, distribution channels). Shemaroo’s role is a value add player like any other industry here - they monetize this content at a price higher than cost by differential packaging and leveraging their distribution channels. They chose to do this with movies in second cycle because of higher predictability of monetization. The opportunity and strength of business model is how big a spread they can create (monetization - cost_of_rights) with their expertise and not in the age_of_content or cost_of_rights. As long as they can acquire enough content and keep their margins the nature of actual content does not really matter, its just a raw material.

Counter views are very welcome.

disclosure: invested.

6 Likes

I suggest you move this post to TV18 thread. Let us keep this thread only to digital media industry growth and Shemaroo unless. You may create comparsion among the players in the space on various factor in which case same message can be shared on all the threads of related companies as same would be relevant for all players in that industry. However, just suggesting TV18 being better investment case with growth driver does not seem to be relevant post for this message. My apology for being very vocal.

1 Like

@dd1474 many thanks for your concise summary note on AR and AGM.

I just have one doubt. I see digital entertainment market shaping into two segments first is paid subscription model and second is more democratised world of YouTube. We have got good number of players in paid category now Viz. Hotstar, Altbalaji, Amazon Prime, Netflix etc and this segment becoming more competitive. I see many movies coming on Amazon prime only after one month of release. Shemaroo has clear strategy of buying content in second round (may be after 5 years of release). Would there be enough good quality content available to them in future? More importantly, any thoughts on how these OTT acquire the content, do they buy exclusive rights only ?

2 Likes

Netflix, Amazon and other OTT players are trying to develop own different quality content as their main strategy to attract the audience. This is supported with movie rights (New). The first two content acquisition while would be important to success of OTT platform, they would still need old film as well to address the population above 45+ going forward. Further, what is important is also acquition price of content and timing of content. Shemaroo acquired around 500 Hindi films perpetual right over 2011-2016 period when digital market was growing but not established. While that can not assure future certainty, but still with recent spurt in pricing, Shemaroo is well placed to utilise content on various platform and get moderate return from same. For more on strategy on acquisition and monetisation of content and way forward you may refer to various conference call and notes on thread. With so many moving parts, I would like to trust the wisdom of management which has survived and thrived during various transformation in market over last 4 decade then to become forecaster. I agree to your view about increasing competition, but also optimistic about increasing demand which has grown at more than 35-40% CAGR over last 5 years. Personally believe there is room for everyone in media who can manage the dynamic environment. Apology for not being able to directly answer your question, but it is better to accept ignorance then to give wrong answer in my opinion.

Discl: Shemaroo is among my top 5 holding and my view may be biased due to my investment. Investor shall do its own due diligence before taking any investment decision.

3 Likes

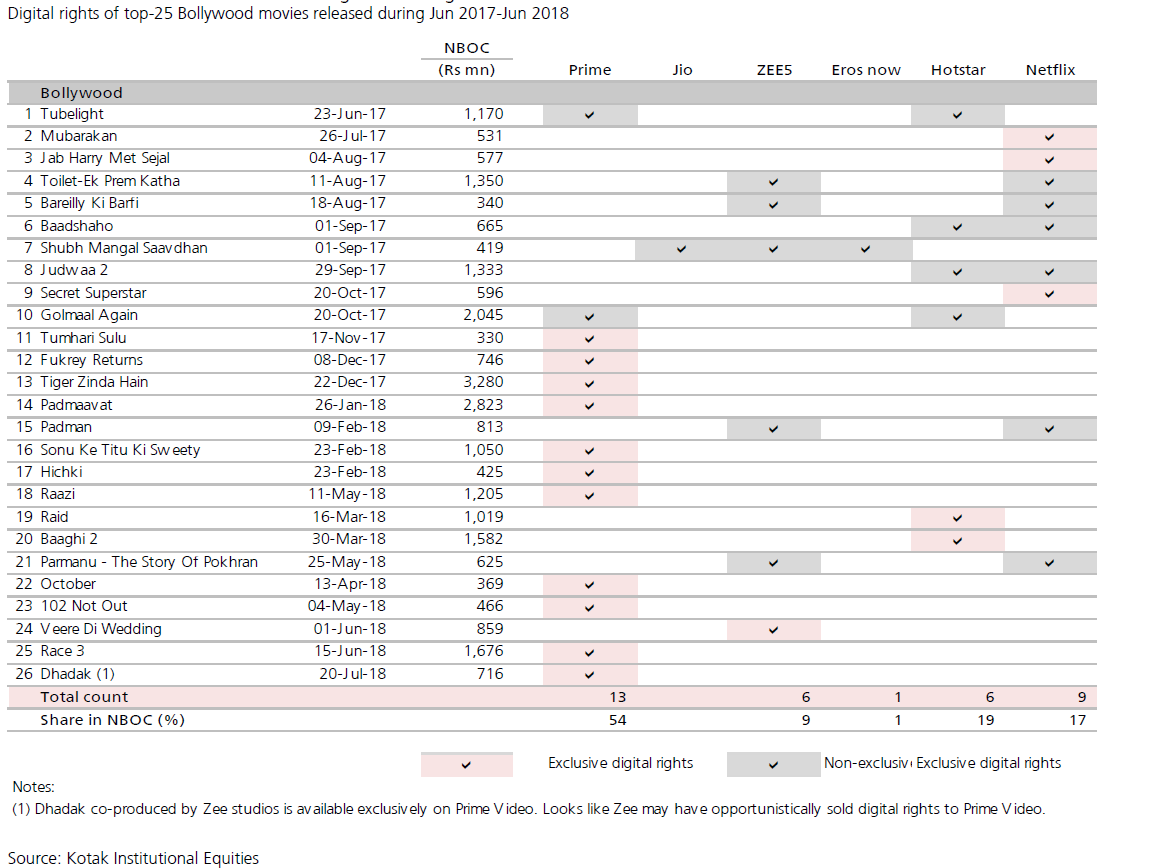

Kotak Securtiies has came out with report on OTT players in India recently. Find enclosed one of interesting table about Digital acqusition right of new release. While not relevant to Shemaroo as Shemaroo enter in second round and value is substantially lower than first round, still it provide broad indication of interest in First lifecycle for digital rights.

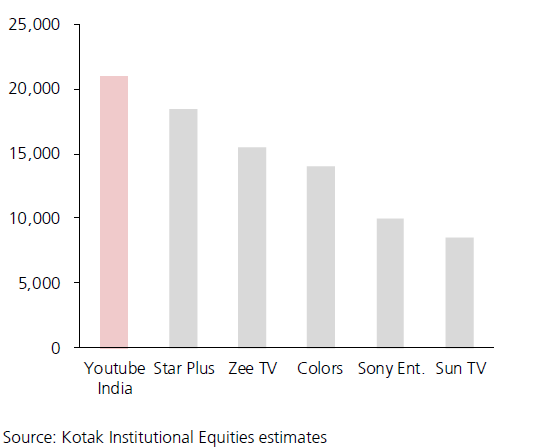

Another interesting informaton about YouTube having large Advertisement share then any other Hindi GEC Broadcaster.

Disclousre: Shemaroo is among my Top 6 investments and my view may be biased. Investor shall do his/her own due diligece before making any decision.

5 Likes

Same report…it’s winners takes all game.

It will be tough for Shemaroo to sustain in long run of disruption. Currently, it burning lots of cash and future is not sure due to disruption risk by big players. Even kotak has reduced target price of Indian OTT