Shemaroo up by 18% ,patience is paying off now -any reason of such sudden rise

One reason could be Nirmal Bang came up with buy rating with target of 612 rs for Shemaroo…

It’s just a guess…

Edit: The report was published by Nirmal Bang on 11/01/2018

1 Like

This does not impact Shemaroo’s youtube channels considering no. of subscribers and the views, however we just need to keep an eye on all policy changes by youtube for monetizing views.

2 Likes

A very exhaustive read available on Shemaroo Entertainment Limited:

Indian Television Industry- Marred by the Age of New Media.

https://drive.google.com/file/d/1iasl3sLiTvru2xaTkz5wU6uf8eAcn0mB/view

5 Likes

Conference Call highlight for Q3FY18 for Shemaroo:

The company revenue show expected growth of double digit in traditional business and more than 40% from non-traditional business during the quarter. As discussed in previous Call, the company has been over with investment phase and the investor shall expect decline in total debt going forward. The management also indicated that they expect Inventory at March 2018 being lower/flattish as compared with March 2017. Improving cashflow and balance sheet are main focus area vis profitability. On profitability, they look at getting Pre-tax IRR at 18% which may not be necessarily mean highest profits in particular quarter. During the quarter, the company entered to deal with Vuclip and Launched a marathi movie channel on Tata Sky DTH.

New Media

YouTube:

The company reported cumulative 3 billion view on all YouTube channel. During the December quarter, there were around 540 million monthly view vis 400 million monthly view in Sep 2017 quarter. Jio launch has been major catalyst to this growth in viewership. Sep 2016 (Pre Jio Lauch) Daily view were around 4 million which increased to 17 million per day in December 2017 quarter. However, YouTube continue to adversely affected by Brand pull out which resulted in lower total advertisement spending on YouTube and hence high growth in viewership did not resulted in commensurate revenue and profitability.

YouTube has further changed the minimum threshold of viewership and other factors. The intent of same was to improve quality of engagement with customer and improve appropriateness of content. This change is unlikely to impact Shemaroo as most of the channels are exceeding that threshold. This also indicate YouTube focus being change from only viewership to brand safety and engaging more with serious vendors. The company expect that in medium term many fringe players may out from business and it may be benefited in medium term.

Over past few quarters, due to YouTube specific issues, the share of YouTube which was around 30% of New Media has been declining. For the company to achieve more than 40% growth, YouTube adv. revenue has too catch up.

Telecom

Nearly 50% of New Media business is coming from Telecom Wallet. The company has grown at decent rate from this business in past. While Jio has increased challenge from domestic business, the international launch over last two quarters in Sri Lanka/South Africa/Dubai/Nigeria has assisted the comapny to maintain growth rate from this business. Going forward growth from this segment would be good however maintaining same at 30% may not be possible.

Syndication

This has been third pillar to New media business accounting now for around 15-20% of share in new media. Syndication business with Netflix/Amazon/JIO and other OTT platform get reported in this segment.

Netflix/Amazon are currently focusing of exclusive content of new movies in order to attract the customers. They are predominantly in first phase of marketing in which Shemaroo is not present. The management describe this strategy as "Hunting and Farming. While New movies would assist them in “hunting” the Customer (acquiring the customer) Enriched content would assist them to “farming” the Customer (engaging and retaining the relationship). Shemaroo describe its content as “Staple Diet” of distribution business.

The increased number deals and entry of new players would continue to drive growth rate of this business at around 35-40%.

Digital Advertisement budget

The advertisement budget from media planner is yet to accept new normal of high viewership growth in video content. That would take some time as media planner adjusts their allocation. Having said that all report on digital advertisement continues to expect growth of around 30-35% growth per annum for next 3-5 years.

There are three factors due to which media budget may not increase directly in proportion to viewership. First, the issue of inappropriate content faced by YouTube would affect Media planner going on slow of the platform. The virtuous cycle of digital advertisement has paused after YouTube experience. When they advertise on traditional media, they are sure for audience and their brand image. Same can not be assured as seen from YouTube episode. Second, there still no matrix are develop to major effectiveness of advertisement on new media. Third natural decision making process which come with leg. From receipt of data, to ananlyse and them came with right decision.

Traditional Media

Traditional media business was adversely affected during Q3FY17 to Q1FY18 period. However, there was an improvement in sentiment post June 2017. Same has partially materialise in December 2017. Advertisement revenue for Channels are good and channels are now looking forward to more content acquisition in view on positive outlook. Hence, Shemaroo expect to show Double Digit growth in Traditional media during FY18. During 9MFY18, the company reported 7.5% which 6% in 6MFY18 and -2% in Q1FY18.

Subsidiary

The company subsidiary in content distribution in airlines have shown major jump in ebitda margin which result in lower loss. During the quarter, the company acquired specific distribution right on Airlines for Bahubal2. The Airline subsidiary business is showing good traction. The Company has one JV which is attempting to develop new product to monitise its content. Management expects that over next 3 years all businesses would break even and contribute positively in bottom line.

Balance sheet

Inventory:

The company continue to maintain marginal increment in inventory during FY18 full year. While around Rs 60 Cr is added during the first half, same is likely to be decline in second half with company having flattish/marginal inventory during FY18. The management did clarify that they would continue acquire new inventory for future growth. However, since last three years major efforts has given the required content library, the focus would be more to enrich library or for specific demand. Also, the fund requirement for same would be met from internal cash generations.

Inventory turnover ratio of 1.3-1.4 times before Content acquisition phase. The company expects to reach same level during next 3 years.

Debt

The company has paid back debt during first half cash flow. Going forward, the excess cash flow would be utilised to repay the debt and hence interest cost would also likely to decline and major decline is expected to observe during FY19 in interest cost. During the quarter, the company repaid some more debt which resulted in lower finance cost. The company did not share Balance sheet details on December 31 2017 as same were not reviewed by the auditor. Over the medium, after providing for inventory acquisition, the free cash would be utilised to repay debt till the company debt equity ratio reach to 0.2-0.25. On reaching this milestone, the company would take call whether to repay loan fully or to keep leverage depending prevailing market condition. The company expects to reach the expected gearing in next 2-3 years.

New Team

During FY18, the company added team of professional. Mr. Vaibhav (Ex- Reliance Jio) would be involved in marketing product to Telecom segment. Mr. Omprakash (Past experiece with Saatchi and Saatchi) is working on Deigial marketing in Social media. Mr Rahul Mishra (Previously with BBC) is looking at overall marketing. Mr. Subhash (Previously working with Videocon DTH) is working on DTH marketing.

The total team size of the company is around 500+ of which nearly 118 (or 180) are working in Digital business. All these team members have recently joined, which has increased cost and lower margin in last 2-3 quarters. However, in medium term, they are expected to materialise Shemaroo its potential of digital market.

Accounting Change

From April 1 2017, the company has charged 85% of content cost to Traditional media and

15% content cost to New Media for all content acquire From April 1 2017. In past, the company was charging 90% content cost to Traditional media and only 10% to New Media.

Impact of Limited acess to Song

The company would have right to distribute music video of songs for content acquired post 2000. However, in the company view, the value of music digital right is around 1/10 of digital Video film rights. Further, its posting of Filmi Ganne as vintage would continue to have benefit of large content library which is unlikely to be affected by lack of new songs.

Disclosure: I have investment in the company and my view may be biased. The investor shall do his/her own due diligence before taking any decision. I may have misinterpreted certain communications/discussion and reader shall take note of same.

16 Likes

Hi Dhiraj… That was exhaustive… I did not hear the concall… But you

made it irrelevant now.

BTW, what is your overall sense from management commentary on the

potential of the biz going forward…

My Summary of conference call

1 Like

1 Like

Dear all,

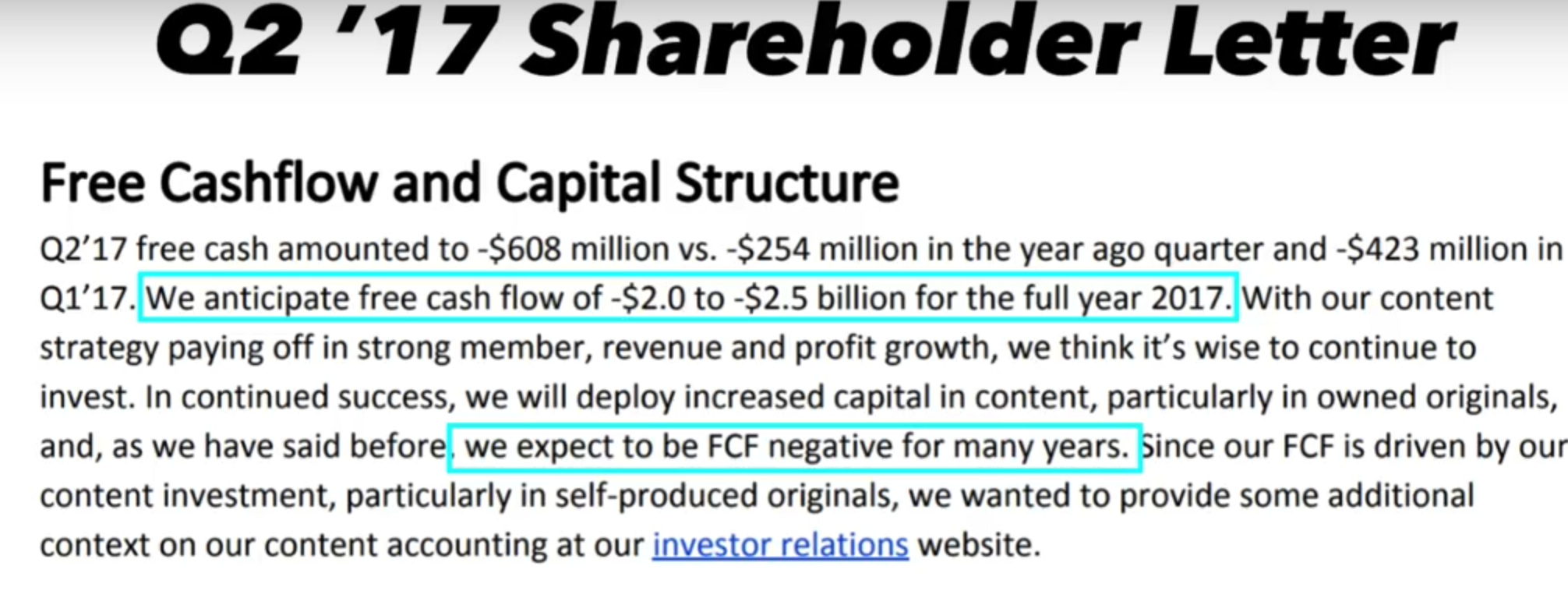

Just out of curiosity I was reading reports on Netflix, found some interesting notes related to -ive free cash flow, as the same concern is being highlighted for Shemaroo as well, although seniors already have shed light on this aspect and clarified.

it was interesting to see Netflix expect to remain -ive free cash flow for years to come seems like this is part of the plan for Netflix, as growing big is the first target and being profitable is 2nd, as Amazon CEO says, its foolish to focus on profitability when you are small, grow big and then add efficiency for 4-5% which will be huge amount…

it seems all these new age co’s are doing this way… so I think investors might have to lower bar on +ive cash flow in order to catch new age co’s where turning +ive cash is very probable and especially the business like shemaroo, where costs are front-loaded and revenue acure in many years in future…

i don’t think Netflix and Shemaroo are the comparable business but still, we could get some understanding on the nature of industry/business.

Disclosure: I am a novice and new to the investing, Shemaroo is the significant part of my portfolio, please pardon me if this post seems totally irrelevant.

1 Like

Netflix is following the age-old principles of monopoly followed by McDonald’s and Coca-Cola - It is to be bigger than anyone else and have an unassailable market share. Use the network effect to its advantage (People who watch stranger things will let other know and will make sure they watch). Create an addictive product (everything from the logo to the Netflix chime to the way the episodes start one after the other is geared towards this). To last longer than anyone else in the process. Negative cash flow is inevitable for its grand plans as they create more and more great original content and advertise (you must see the number of hoardings in just Bangalore) to expand.

Interesting thing is that they are able to charge a lot more than competition - Amazon Prime which is a lot of things is Rs.999/yr and on offer you can get it at Rs.499/yr or even free. Netflix has remained at Rs.650/month or Rs.800/month - same is the story everywhere else in the world. Despite this they have expanded drastically in South America and Asia and will continue to do so. Latest earnings numbers confirm what is happening as well.

I like Shemaroo but its a very unfair and incorrect comparison. Content providers like Shemaroo are at the mercy of the gatekeeper monopolies for their revenue.

7 Likes

Absolutely agree with you, both companies are worlds apart in their business model. Netflix is a content producer and distributor while Shemaroo is a content trader.

I recently travelled by Tejas, the new age train which has LED screens, to Goa. Seems like the movie content is being provided by Shemaroo. All the movies were from Shemaroo library.

This can be one more avenue for Shemaroo to sell its contents apart from airlines, with Indian Railways expected to add more such trains across routes.

What I also noted is you don’t need great/superhit movies in this case. A catalogue of normal/average movies is good enough. People will end up watching whatever is there and appreciate it

4 Likes

Shemaroo launches online app… Not just for music and video… But for receiving Prasad, booking poojas, live darshans, astrology etc…

Going B2C… Will it turn out positive for investors

some thoughts on HariOm app

1)Good idea to reduce frictional cost of booking pujas ,It can be one stop shop for people to book pujas, whenever they require a favour of god,are feeling guilty, exams etc. Can book puja from home , without the hassle of going to the temple.

2)Looking at the success of slow tv (reference:https://www.youtube.com/watch?v=sQ6ufnkXZFw) the video streams of temples also makes sense.

3)Monetization of content is not clear , as there is no ads in the app, videos or the streams

( maybe strategic move to not include ads to soil the user experience due inapproprite ads showing up)

4)Is all the content to funnel traffic to the app and money will be made through commissions on Puja and prasad orders??

5) Can be expanded to include various revenue streams as in ordering portraits, tanjore paintings , idols etc.

Earnings Call Q3 FY18 Key highlights:-

- Announced content deal with Vuclip, Spuul

- Digital media continue to grow at very high rate (Q3 FY18 growth – 40% y-o-y) and represents 26% of the revenue

- 50% of digital revenue coming from telcos

- Youtube ad revenue impacted in last Q due to implementation of stricter brand safety guidelines but it has to contribute more in future to sustain 30+% growth trajectory

- Value of old library in new digital environment: New films can draw customers to OTT/Digital platforms, but retention of customers will depend on old good library

- last 2 Q, a strong ad revenue guided traditional media growth

- Guided for no gross margin expansion in future due to higher content and employee cost

Key highlights of previous quarters - https://quotethemoat.wordpress.com/

1 Like

Any body assessed impact on Shemaroo due to launch of ZEE5 by ZEE? What is value proposition of Zee entertainment with ZEE5 and Shemaroo? Now ZEE has more stronger digital, TV and other platform for growth.

Both operate in different domains. While Shemaroo is a content provider, ZEE5 is just another OTT platform (and there over 30 such OTT platforms).

OTT is more profitable or content providers? Shemaroo has negative cash flow since many years? Any ideas?