Hiren Gada Interview on CNBC. Continue to suggest to grow at higher than industry growth for Traditional media (Industry growth in high single digit) and New Media (industry growth at 30%)

1 Like

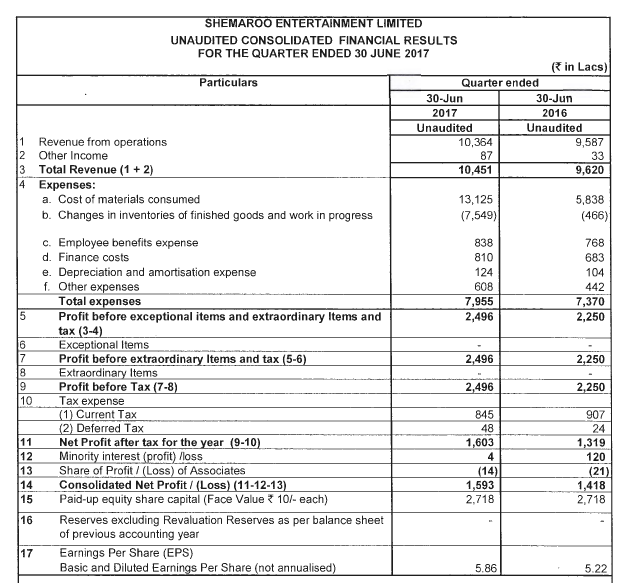

Shemaroo Q1FY18 results:

- Total Income increased by 8.6% to Rs. 10,451 Lacs (Rs. 9,620 Lacs in Q1

FY2017) - EBITDA increased by 12.9% to Rs. 3,429 Lacs (Rs. 3,037 Lacs in Q1 FY2017)

- EBITDA Margin stood at 32.8% in Q1 FY2018 (31.6% in Q1 FY2017)

- Net Profit after tax increased by 12.3% to Rs. 1,593 Lacs (Rs. 1,418 Lacs in Q1

FY2017) - PAT Margin stood at 15.2% in Q1 FY2018 (14.7% in Q1 FY2017)

- Basic and Diluted Earnings Per Share stood at Rs. 5.86 in Q1 FY2018 (Rs. 5.22 in

Q1 FY2017)

Source: http://www.bseindia.com/xml-data/corpfiling/AttachLive/1df47090-0fff-4302-bc43-ffb3e4babd21.pdf

http://www.bseindia.com/xml-data/corpfiling/AttachLive/fda6b204-b49c-467e-83b8-5f83b3e68f93.pdf

2 Likes

Q1FY18 Conference Call Highlights

Financial Highlights (Consolidated):

Total Income increased by 8.6% to Rs. 104.51 Cr Vs Rs. 96.2 Cr YoY

EBITDA increased by 12.9% to Rs. 34.29 Cr Vs Rs. 30.37 Cr YoY

EBITDA Margin stood at 32.8% in Q1 FY2018 vs 31.6% in Q1 FY2017

Net Profit after tax increased by 12.3% to Rs. 15.93 Cr Vs Rs. 14.18 Cr YoY

PAT Margin stood at 15.2% in Q1 FY2018Vs 14.7% in Q1 FY2017

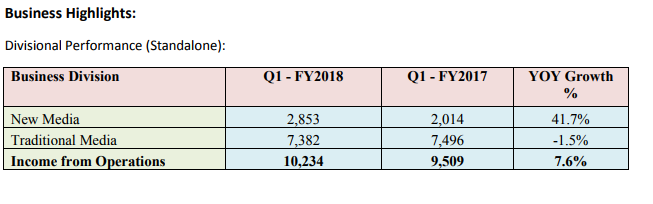

Revenue breakup:

New Media increased by 41.7% to Rs. 28.53 Cr Vs Rs. 20.14 Cr YoY

Traditional Media decreased by 1.5% to Rs. 73.82 Cr Vs Rs. 74.96 Cr YoY

Operational Highlights:

Crossed 12 million YouTube Daily views

Crossed 3 million subscribers on our flagship YouTube channel ‘ShemarooEnt’

Crossed 3 million subscribers on our YouTube channel ‘FilmiGaane’

Crossed 2 billion cumulative views on our YouTube channel ‘FilmiGaane’

Crossed 5 lakh subscribers on our YouTube channel ‘Indian Comedy’

Some brands have pulled their advertising out from YouTube since some of their ads were shown next to hateful and offensive content. As a result, YouTube has implemented stricter brand safety guidelines and therefore stopped monetizing certain videos

Traditional Media:

Expect double digit growth in line with Industry projections. Business growth is returning back to normal from a full year perspective. Revival in Ad spends have been reasonably good.

New Media:

Industry projections are 30% CAGR growth for the next 3-4 years. We should do better than that, expect to have 40%+ CAGR growth (internal target to grow). Operating leverage will play out but hesitant to factor in any margin improvement at this moment. Does not want to raise high expectations. It’s a seller’s market, lot of demand is there. Demand for content and prices are going up.

YouTube:

Ad spend is not in line with views growth. The Ad rate is impacted due to Brand safety hit globally.

Growth in revenue is not according to growth in views.

Inventory:

Inventory addition 75 Cr this quarter. Some inventory carry forward from previous quarter. We are at end of investment phase now. Expect to have negligible inventory addition from a full year perspective. Inventory additions for next 3 quarters to be low.

Investment strategy

We have decided 4 years back to do an aggressive investment to build a large library from internal accruals, borrowings and equity. We have been making investment of around 100 Crs on an average every year for the last 3-4 years. Now we don’t need to be in an overdrive mode to invest. There will be a continuous need for investment but not at the pace we have had so far.

Debt:

Future growth requirements should be funded through internal accruals. We plan to reduce debt, however September number could be slightly higher. Current quarter debt levels are close to March numbers (1-2% higher).

Cash Flows:

Expect more FCF going forward than what is needed for investment.

Competition:

Balaji-Reliance deal is content play. Prices have gone up for digital content but Growth fully not caught up. Revenue lagged behind the growth but expect to pick up.

Amazon Prime buying content but not buying perpetual film rights. Generally 3-5 years deal.

General:

We made few Perpetual investments like Jab we met, Golmaal, Golmaal Returns, Bhagam Bhaag, Khattha Meetha, Blue – mostly from Ashtavinayak. 2600 films – Aggregate rights. Could be for more than 5 years. We target IRR 18% when we buy content.

Perpetual right is like when we step into the shoes of the producer. We own copyright of the film and become author of the film. Now music labels are retaining Songs video rights. We can monetize entire film or film in parts but not songs alone.

New films – Inflation 3x-5x in 3 years. Second/Third cycle where we operate – Inflation doubled in 3 years.

If someone explores feasibility to re-make a movie and if we own perpetual rights, then they have to make a deal with us. Did 1-2 such deals in the past but movies were not released. It is at a nascent stage at this moment, the results have been mixed

In non-film content, we have a category called Special Interest with following sub-categories:

a. Kids

b. Devotional

c. Health & Fitness

d. Television (classic serials)

The sub-category Devotional gives us a good edge as we were able to monetize across digital and traditional media

DTH tie-up:

Potential of Ad free/Paid service subscription. Services launched with several players and response has been satisfactorily so far. For an Ad free service, let’s say consumer pays Rs 30-60 per month and this is split three ways:

a. Govt taxes/license share (largest component)

b. Platform

c. Shemaroo (we get 40-50% of what remains after Govt share)

This is classified under Traditional Media

Disc: Invested

14 Likes

2 Likes

Shemaroo AGM notes

I and @dd1474 attended AGM of Shemaroo yesterday and here are the notes from interaction with management

Disclosure: The points mentioned below are my interpretation/understanding of the interaction and the articulation may have scope of inaccuracies to creep in

-

Positive cash flow generation: Before the investment phase begun in 2011/2012- Sales to inventory ratio was close to 2 (on 100 Crore on inventory, sales was close to 200 Crore), while currently it stands at close to 0.8. As company moves out of investment phase and enters “monetization” phase, the sales/to inventory ratio may inch up towards earlier steady state number gradually over next 2-3 years. Though, it may not mean that on inventory of 500 crore- company will register sales of 1000 Crore. In a more likely scenario, it will mean that 500 crore number may move down while sales will move towards 600-800 Crores. The process will happen gradually over next 2-3 years and sales/inventory may reach 1.5-1.8 range at steady state level. This will also mean that the cash flow from operation will become positive over a period of time

-

**Impact of shifting ad spend to digital media on traditional media business:**Share of digital ad spend in overall advertising pie is rising hence will it pose a threat to the ad spend for TV/traditional media customers?- Ad spend will follow eye balls in long run hence if the digital media consumption is rising- ad spend will rise to correspondingly in the long run. It also means, it will take away ad spend from some other medium. However, it is not likely to be Television. USA, inspite of almost a decade ahead of us in terms of digitization, has TV ad spend which is rising and TV viewership is steady. In US, typically, digital has taken away the ad share from print/OOH. In India, TV is still under penetrated, with 70% of household having access to TV, there is enough headroom to grow. Hence, at least for next 5 years, we do not see a threat for traditional media business. In fact, before demonetization, traditional media was growing at 16% in FY 17.

-

Traditional media growth in FY 18: We see 8-10% growth for traditional media business for FY18, not withstanding slight degrowth in first quarter. All indications from various stakeholders/participants is that festive season ad spend is going to be very good and hence the industry will return to growth trajectory. Also, we must keep in mind that at the end of the day, India is largely a consumption driven economy and hence over a period of time, companies will have to spend money on advertisement for building brands/new product introductions. In India, ad spend/GDP ratio is very low especially when we are primarily a consumption driven economy and hence there is enough headroom for ad spend to grow and the entire ecosystem to flourish

-

**Margin trajectory:**New media has higher margin as compared to traditional media business and also has operating leverage. Hence, ideally, as the share of new media increases in the overall revenue mix, margin shall inch up. Margin improvement thesis has played out like that in last 2 years. However, for next 2 years, company’s priority/focus is balance sheet, hence, cash flows/lightening of balance sheet may take precedence over increasing margins.

-

Youtube ecosystem facing headwinds and its potential impact on new media growth: Even though You tube remains an important contributor to the new media business, due to launch of many new platforms in last one year, our dependence on Youtube has come down. Because of that, inspite of challenges faced on that platform, we are able to grow above industry average consistently. Another thing that has happened is that inspite of very large increase in views, commensurate monetization of the increased viewership has not happened. Despite that, we are growing at current rate. Monetization of viewership will surely happen over a period of time, however, it is difficult to define time frame around that. For Shemaroo, we remain content focused company and it doesn’t matter where our content get monetized. Today, we have so many avenues to monetize content and we are present across all major platforms that growth moving from one platform to the other will not materially impact us

-

New media rights in overall content basket: In last 4 years, we have focused on new media and hence almost for 90% of the rights acquired during that period, we have acquired new media rights as well. For rest 10%, for some specific reasons, new media rights have not been acquired. For content acquired before 2012, there may be some content where the new media rights are not acquired. However, even in that library, large portion of content has come with new media rights

-

Increase in receivables from 106 crore to 190 crore: In FY 16 concall only, we had mentioned that reduction in receivable days is not permanent and was likely to normalize. In traditional media, receivable days range is 180-200 and for new media it is around 90 days. We are comfortably in the same range. Though, for March 17, receivables seems somewhat bloated because of the cash crunch faced by clients post demonetization. However, that bloat is gone now and situation is normalized now.

-

Rational for embarking on ambitious investment phase from 2012: There were mainly three drivers to that decision, one involving traditional media and two drivers for new media

-

Digitization of cable TV: Parliament had passed an act for digitizing the cable TV. Even though digitization was discussed several times in the past, passing the act was first concrete and almost irreversible step towards digitization. Even though timeline for implementation may stretch, it was almost certain that digitization of cable TV will happen sooner of later. This was very positive for broadcasters who will eventually use increased money to buy more content.

-

Penetration of smart phone and advancement in video viewing technology: The way video viewing technology was changing, it was possible to view high quality videos on low cost mobile phones too…which was earlier limited to high end phones. At the same time, adoption of mobile phones was happening very very fast. Millions of mobile phones with video viewing capabilities were sold every month. In other parlance, the hardware were getting in place, hence it was only a question of time before the software(content) will get consumed.

-

BWA and 3G licenses were awared: We could sense that this will change the landscape for data consumption and eventually, richer media like video will get consumed more and more as the speed/bandwidth will increase and cast of data will fall.

For a company like Shemaroo, which is highly content driven, confluence of these kind of factors was once in a lifetime opportunity and hence we embarked on ambitious investment journey. We had set in sight to acquire content across generes, startcast, timeframes to complete the whole basket. We have achieved those objectives and hence are nearing the end of investment phase

- Steady state dynamics for Shemaroo once monetization of previously acquired inventory is over: In steady state condition, we shall be able to generate enough cash flow to support our inventory addition for growth.

Overall, management seemed confident of executing as per plan of buying less,selling more, shrinking balance sheet and generating free cash flows.

@dd1474, please add to the points I have missed, or correct the any of the above if I have misinterpreted the management commentary.

36 Likes

Dhwanilbhai Thanks for detailed commentary & analysis of shemaroo Agm. It is so crystal clear which has cleared many questions about shemaroo. Great efforts

Regards

Its very Informative

Thanks Sir

Hi Dhwanil,

Thanks for the update. Can you also please share management’s view on competition? how do they see pricing for content going ahead? and more importantly how much competition are they witnessing in Stage 2 of bidding where Shemaroo competes.

Thanks

Kunal

Find enclosed some addition from my side.

On Traditional media growth point, Last year Second half was adversely affected due to demeonitisation.So despite not so good growth, the company expect H2 being good. Better monsoon and marriage/festival season would drvie demand for media space.

India ad spend as compared with GDP (for a consumption driven economy) is relatively low. As GDP growth increase, media multiplier to GDP may also improve which can drive growth for advertisement.

3 Likes

Though, some of the points have not been part of this year’s AGM interaction. I will try to answer them from my earlier interaction and management’s responses in concalls.

Competition: Barring few organized players such as Pen an Tips, there are not many pure aggregators. Even though, there are production houses who retain the rights of the films produced by them and sell them in second cycle. I think, at best 4-5 large players who have broad enough basket to be compared that of Shemaroo and they are much smaller. Another bigger player is Hungam group, however, their business model is based on monetizing content on their own platform and hence not too appealing to their competitors in OTT space.

_Pricing of content:_Management has always maintained that in second cycle, the inflation is much less than that in the first cycle. Also, traditionally, the value of film rights in second cycle double every 5-6 years so I think, it is reasonable to assume 12-15% inflation. However, the acquisition cost too grow at the similar pace unless there is some major dislocation in the market. Hence, net net, higher realization is accompanied by higher acquisition cost and hence not much impact on margins either way

Competition in stage 2 of bidding All the news headlines that we are seeing on amzon/netflix getting into exclusive deals is largely for first cycle. Direct dealing by the large production houses do happen in second cycle (i.e Rajashri deal with amazon), however, these players have been there as competition even in traditional media space and hence no major change in competitive intensity. Another barometer of competitive intensity not changing is that the inflation level in first cycle rights is much higher as compared to second cycle movies. So, all in all, not much has changed in terms of competitive dynamics.

Disclosure: As I mentioned the response, above points are my interpretation of management commentary during concalls and interaction during couple of AGMs. Though, I have endeavored to put up an accurate picture, I may have misinterpreted or worse, my biases may have creeped in while interpreting or articulating.

6 Likes

Why the company is recording its content as a part of its inventory? It should be recorded as “intangible assets” and must be depreciated at the relevant rate on the basis of its estimation of realisation of revenue from its content. It must be recorded as a CAPEX.

Can anyone clarify why its recorded as inventory?

1 Like

Kindly refer IndAS 2 and the definition of ‘Inventory’.

- held for sale in the ordinary course of business;

- in the process of production for such sale; or

- in the form of materials or supplies to be consumed in the

production process or in the rendering of services.

I think it is not held for sale in ordinary course of business. If i purchase a DVD of DDLJ, it doesn’t means i am purchasing its copyright of content. Neither it is in the form of materials or supplies to be consumed in the production process or in the rendering of services.

So i don’t think so it must be classified as “INVENTORY”. Other players in the same industry such as EROS are recognising it as INTANGIBLE ASSETS under “FIXED ASSETS” HEAD.

Inventory is the easiest thing to manipulate profits in accounts. Morever, there is no statutory requirement to provide details of INVENTORY in Annual reports to its shareholders. Company biggest asset is in the form of Inventory and no details have been mentioned about Inventory in Its Annual report or Investor presentation.

1 Like

IAS 38 requires an entity to recognise an intangible asset, whether purchased or self-created (at cost) if, and only if:

It is probable that the future economic benefits that are attributable to the asset will flow to the entity; and the cost of the asset can be measured reliably.

This requirement applies whether an intangible asset is acquired externally or generated internally. IAS 38 includes additional recognition criteria for internally generated intangible assets.

INTANGIBLE ASSETS held as sale should be recognised as Inventory. But Intangible Assets(content) which is used for providing services on rental basis or pay per use basis should be recognised as “FIXED ASSETS” and sub head “INTANGIBLE ASSETS”.

1 Like

Coming out of long-consolidation (From Jan-Oct 2017) on the weekly charts.

3 Likes

OTT technology underpins new strategy

To help it to achieve its business objectives, Shemaroo engaged with SotalCloud, an innovative global provider of OTT online video platform technology for VOD and linear TV, based in Toronto, Canada.

SotalCloud successfully delivered a streaming video network and app for Shemaroo, based on its innovative OTT technology. SotalCloud modified the Shemaroo platform to cater for certain cultural south Asian perspectives, allowing the insertion of pre-rolls or post-rolls, and providing the capability to upscale to a level of quality that can be plugged into major networks.

Ravi Dani continues: “SotalCloud has provided us with a flexible and cost-effective platform that has enabled us to be fleet-footed in terms of our brand and extending it to the rapid creation of new and tailored channels, with key content for consumers who like the musical, travel or comedic aspects of our content, for example."

“We were determined not to create a typical app that would simply offer the same on-demand stuff as other providers. SotalCloud made sure that our solution is a level (or more) above.”

Ravi Dani explains: “SotalCloud’s technology and high levels of support have enabled us to create our own content channels in just a matter of days. With carriage fees, licenses and other costs associated with providing content to major TV channels, this level of experimentation was not previously viable in financial terms."

“The technology is just so accessible now. We can provide telcos and content owners with a full video streaming service, branded under their own name with targeted content, at a fraction of the previous price.”

Planning for international distribution

“We look forward to developing more bespoke channels and working with third party providers in south Asia and internationally, based on our unrivalled media content.

“The volume of our content means that we can package it up in a professional and sustainable manner to attract other content owners. And, with perpetual rights to this content, we can extract any scenes, music or dialogue from this material."

“We’re looking at distribution agreement with every major telco in India, then extending to the Middle East, south Asia, the UK & US, South Africa, New Zealand, Canada and the rest of Europe. Our aim is to create a global distribution network, partnering with organizations to help with distribution in multiple areas and regions."

“We couldn’t have dared to dream all of this without the technology underpinning our model and that is all thanks to the innovation of SotalCloud,” concluded Ravi Dani.

Along with expansion of professional team with new key hires, these above seem to be significant developments. Good to check back with Management on new plans being chalked out.

6 Likes

Jai Maroo, Director, Shemaroo Entertainment, shares his thoughts on the occasion “We are glad to be associated with a leading OTT service like Vibble TV which is targeted at South Asians worldwide. Our aim is to offer our audience easy and legal access to high quality South Asian Content on every possible platform where a consumer may want to consume entertainment. This tie up is a step towards the direction and will help us to reach a much wider range of audience on these new modes of consumption.”

4 Likes

Conf Call highlight for Q2FY18 for Shemaroo:

The company revenue show expected growth of double digit in traditional business and more than 40% from non-traditional business during the quarter. As discussed in AGM and previous Call, the company has been over with investment phase and the investor shall expect decline in total debt during the period. Further the company shall now on show decline or stable inventory going forward as acquisition is broadly match with sale/usage of content.

New media.

In new media business, while video content consumption has increased, YouTube business was affected due to global problem about some major brand withdrawing from YouTube platform as they believe that YouTube content on which their brand were advertised in past was not appropriate for their brands. The videos consumption of content has continue to benefit from lower broadband rate by Jio and other telecoms players in India.

The margin of the company were declined as there were New initiative in digital business which resulted in higher cost and also addition in manpower to address requirement of new development in digital business.

Revenue share from YouTube for company has not matched with growth in viewership. However, other avenues from new media business have made up for same and the company is confident to show similar growth in new media for FY18 despite YouTube revenue continue to show same issue.

The advertisement budget from media planner is yet to accept new normal of high viewership growth in video content. That would take some time as media planner adjusts their allocation. Having said that all report on digital advertisement continues to expect growth of around 30-35% growth per annum for next 3-5 years.

The lower broadband cost has resulted in jump for company content viewership from 130 MN per month on YouTube to 490 MN per month post Jio launch. Very soon media budget would adjust to this new normal which means high as spend on digital media. YouTube issue with inappropriate content is global issue and the company is trying to resolve that issue, nevertheless same would continue to have YouTube revenue.

Shemaroo however Manage to benefit on other segments of digital media.

The company see reduction of broadband rate resulting developing in many business opportunities in digital area. In order to get benefit from these opportunities, the company has been appointing new experts in various areas which have resulted in higher cost. While what would emerge as major business as of now is not certain, it would definitely provide immense opportunity in digital area. The previous comparable could be the Internet development in late 90s.

For example, Facebook is also trying to show streaming of content in service. Facebook till now not operated on ad revenue share with partner with Google (YouTube). However, it also exploring various options. Such development may provide altogether new area of opportunity to the company for utilised it library.

In all evaluation and encashment of library, 18% pre-tax IRR is always goal to achieve for the company

Subsidiary

The company subsidiary in content distribution in airlines have shown major jump in ebitda margin which result in lower loss. While the business is still

Loss making, the loss of business is declining as scale of operation is improving. The company is already distributing content over more than 17 airlines which are major flier in India related routes. There is some discussion about distribution of content even on railway. Currently, on pilot basis already showing content on Tejas express. While railway is looking for proving video content service to Passengers, the company would be keen to participate only on content distribution. The distribution would also require developing technology for railway, for which company may enter into tie up with technical partner.

Receivable position;

The company normally has 180-200 days of receivable in traditional media and 90 days in new media. However, at time some major payment received or sales book give unusual movement in receivable days for a quarter. During last March 2017, the receivable days were high due to such deal which got normalised during the September quarter and hence receivable days decline vis March 2017.

Inventory:

The company continue to maintain marginal increment in inventory during FY18 full year. While around Rs 60 Cr is added during the first half, same is likely to be decline in second half with company having flattish/marginal inventory during FY18.

Content:

The company Closing stock of inventory was around Rs 500 Cr as on March 31 2017 (239% growth from Rs 146 Cr as on March 31 2013) while during same period, library increased to 3585 as on March 31 2017 (27% growth over March 31 2013). Average cost of closing stock per content right increasing from Rs 5 Lakhs to Rs 14 Lakhs. The increased duration, higher perpetual right, increased share of digital right and inflation were the main factor which resulted in such jump in the cost . The company generally now prefer digital rights being combined with content and has walked out from many deal due to lack of same. Hence, just looking in pure acquisition cost may not give correct picture as various type of rights are being acquired. Further during the period, the company also some prominent successful new films from Red Chillies (for broadcasting), Jab we Met, Golmal/Golmal return/Welcome/Phir Herapheri (all perpetual). The improving and recent quality of content has also increased the cost.

The company would try to get rights on Black and white movie some of which would start losing copy right from 2020 (released in 60s) as colourisation. That would provide additional 60 years copyright for content. However, that would be after proper evaluation of marketability and also cost benefit analysis.

Music right and option to exploit video rights like Carvan:

Shemaroo would continue to operate only in video content and would not like to venture in music right business at present. However, there are various options in Digital area like developing apps, streaming services etc. which would continue to provide opportunity to encash it library.

Traditional business growth

Despite single digit growth in traditional media in FHFY18, the company is hopeful to achieve double digit sales growth for FY18.

Debt

The company has paid back debt during first half cash flow. Going forward, the excess cash flow would be utilised to repay the debt and hence interest cost would also likely to decline and major decline is expected to observe during FY19 in interest cost.

Discl: I have investment in the company and my view may be biased. The investor shall do his/her own due diligence before taking any decision. I may have misinterpreted certain communications/discussion and reader shall take note of same.

18 Likes