Quite a few people seem to have very negative perception of media industry and I was trying to find out why that is the case. Then I came across following excellent article which has been posted by @diffsoft in Eros thread.

I wanted to take findings of this article and try to apply them to Shemaroo. Following are some notes →

Aggressive Accounting

As per ASC 926, the film cost should be amortized in the same ratio as current revenue/expected final revenue. Also if there is negative change in expected revenue, write down shall happen.

Eros amortized 50% of the cost in the first year of release for high budget films and 40% of the cost for medium and low budget films. The rest of the costs are amortized over nine year period. Due to such aggressive accounting, Eros was consistently overstating the operating profits. Also Eros probably did not take the write off for flop films like Shamitabh, Tevar etc.

Shemaroo’s accounting policies have been mentioned in this thread. I feel that the accounting policy of Shemaroo is decent. They also take the write-off of entire amount if they are unable to sell the content in 18 months. I would like Shemaroo to go even more conservative in the accounting - especially in digital rights for both aggregated and long term rights.

High Receivables, Subsidiary Financials

Eros’s trade receivables had increased from 14-15. Also Eros’s subsidiaries had very high levels of trade receivables and they increased rapidly. For one subsidiary, trade receivables exceeded the total revenue booked. There has been aggressive revenue growth reported from non-core locations like UAE, Singapore for Eros.

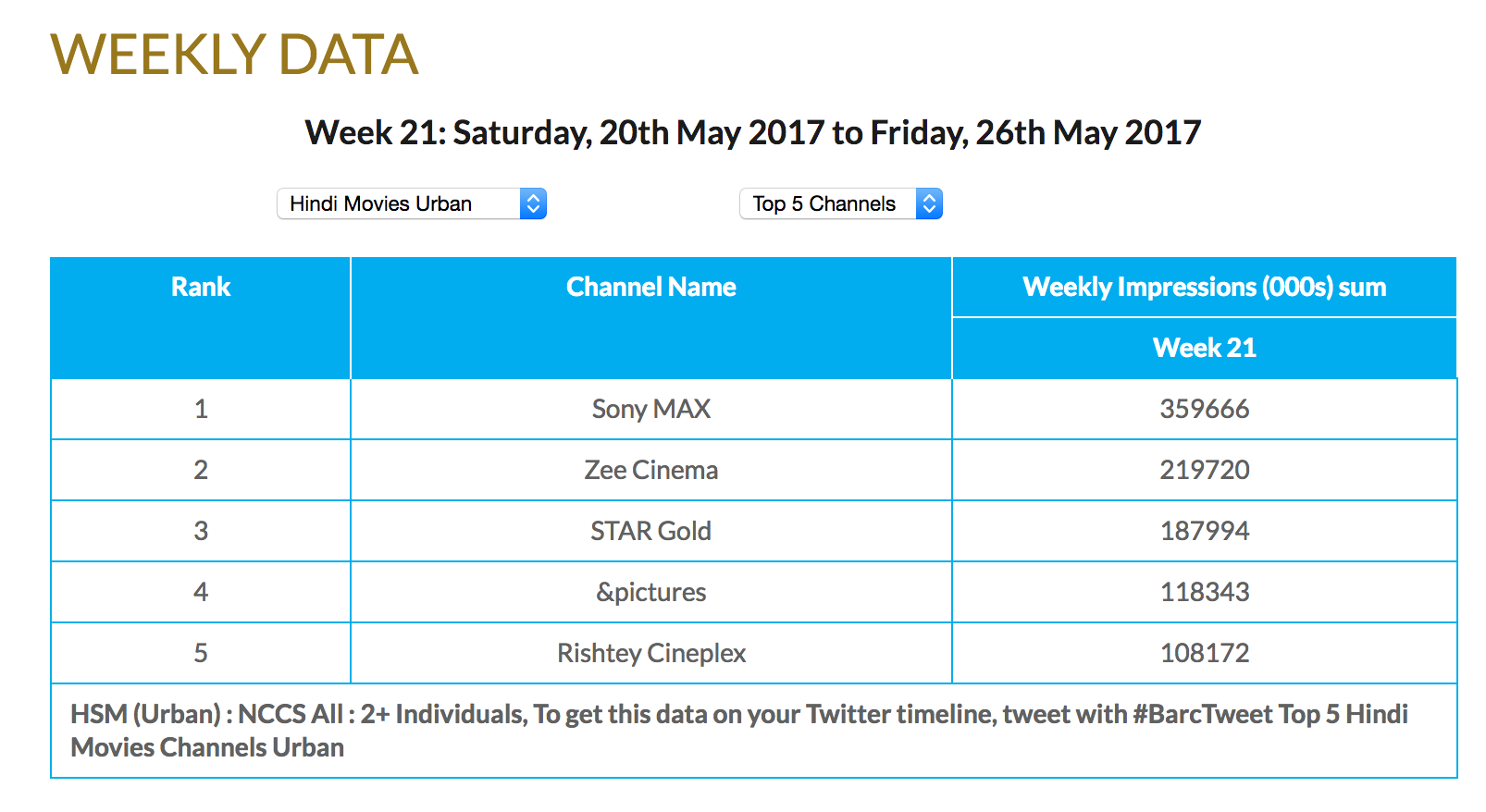

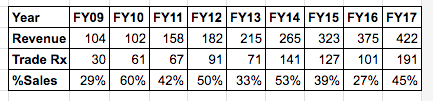

Following are the trade receivable figures for Shemaroo →

The receivable have fluctuated widely and on average more than third of revenue ends up in receivables.

Shemaroo has following important subsidiaries →

- Shemaroo Entertainment, USA

- Shemaroo Entertainment, UK

- Shemaroo Films

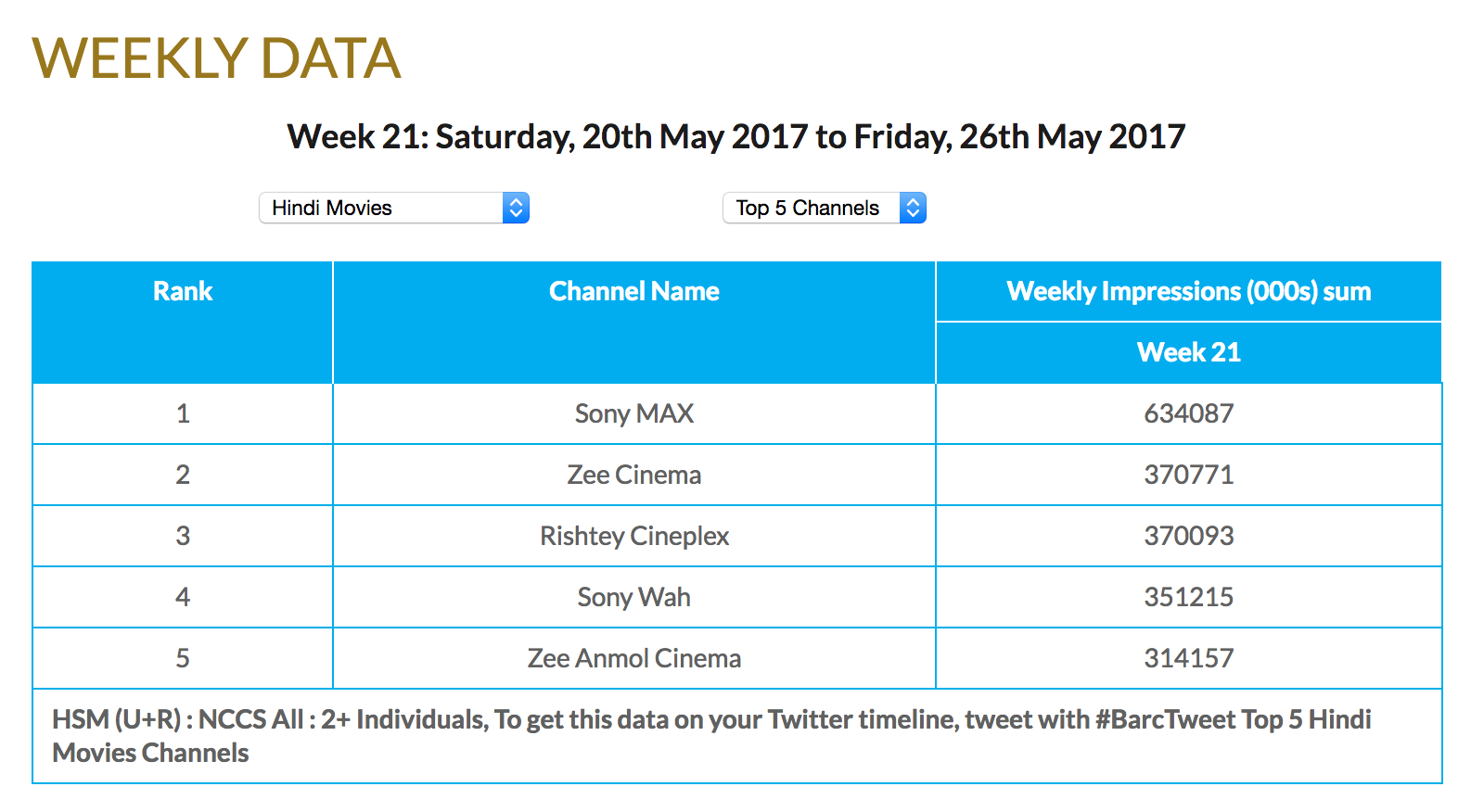

Following table provides trade receivables for company at both standalone and consolidated levels.

As it can be seen above, there is no difference at all between standalone and consolidated levels. Subsidiaries receivable levels are not an issue.

Related Party Transactions and Family

Eros has many family members as KMPs and there salaries grew at aggressive rates, from 5mn$ in FY13 to 23mn$ in FY15. Furthermore, Eros purchased 10% of films from a related party (NextGen films) and these films have been failure. Further Eros sold film rights to another related party (Drishti Creations) which was 10%+ of its total revenue. Further Drishti reported less revenue than what Eros reported sales.

Shemaroo also has many family members working in the company. Following table from DRHP shows relations →

Further there are more related people listed below →

Ketan Maru, Head, Film Production

- Associated with group since 1986

Smita Maroo, Head, Animation Division

- Associated with group since 2003

Harakchand Gada, Head, Accounts Division

- Associated with group since 1987

Mansi Maroo, Co-producer, Film Division

- Associated with group since 2005

- Daughter of Raman Maroo

Kranti Gada, Assistant VP, New Media & Technologies

The salaries are not alarmingly high.

Please note that, relatives of family at KMP position in renting business like Shemaroo is an ignorable for me.

Digital Business Numbers

Eros created a lot of hype for its digital business which was not matched by revenues on the book. Also there seems to be some exaggeration of subscriber numbers in the numbers reported by Eros. Also the number of movies reported by management vs. those available on various portals did not add up.

I haven’t done any work in verifying the number of titles reported by Shermaroo vs. those available on YouTube or other portals. For subscriber numbers, @dd1474 has done some work and they look okay.

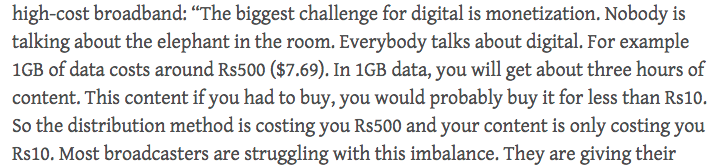

One interesting thing that came out of the link is following paragraph (in FY14) →

There was an issue where the delivery mechanism costed 500Rs. per GB whereas content delivered was only costing 10Rs. I would say that this imbalance has been largely corrected after JIO entered the market. JIO’s entry might cause the content consumption to go up over digital platforms consistently.

I am not very good at accounting and using triangulations. Views are invited (for/against/inaccuracies) etc.

Disc - I am invested in the company and it forms more than 5% of my portfolio. This is not a buy or sell recommendation. Investors are kindly advised to do their own due diligence. I am not a SEBI registered analyst.