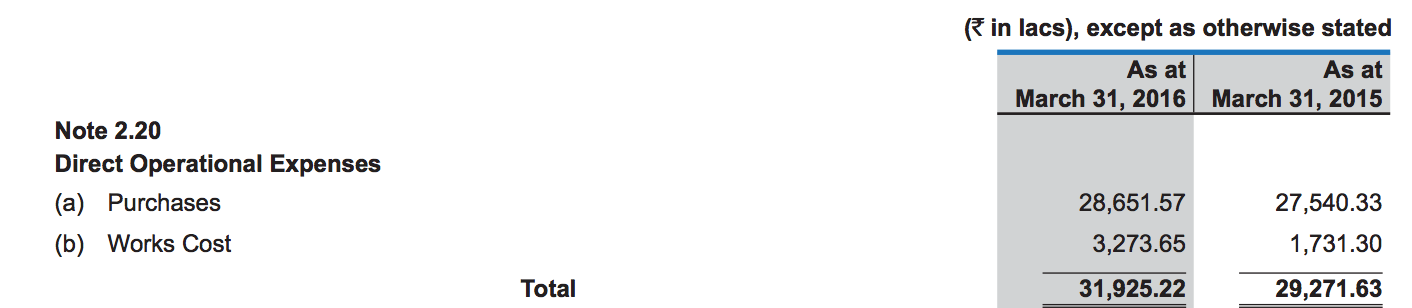

One of the important points for investment thesis is content acquisition at reasonable prices and marketability of content. Although we don’t have information about the acquisition price, we have the list of the movies. I wanted to understand what kind of movies does the company acquire along various axes like -

- Budget (Low vs. Mid vs. High)

- Genres (Comedy vs. Action vs. Drama etc.)

- Actor Bias etc.

To check above parameters, I decided to use the data from 1995 to 2017 for only Hindi movies. I felt this shall give us some insight into the company’s acquisition process.

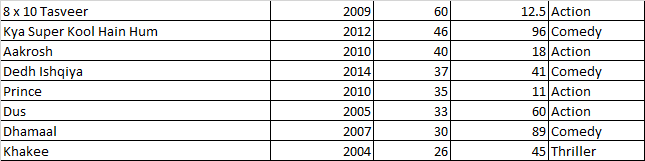

Following excel sheet contains all such movies -

Shemaroo.xlsx (15.8 KB)

Please note that I have looked up movies only from following website. If some movies owned by Shemaroo are not part of this website then insights might defer. Also, I have not tracked Kids, Devotional and Hindi Dubbed movies from the link below.

http://shemaroo.com/genres/

SOME INSIGHTS

BUDGET AND QUANTITY

First let’s just look at number of movies for which the company owns rights by release year.

For a lot of movies after 2010, second phase of monetization might not have started, so we can give less importance to that data. It would seem like company looks to acquire about 10 movies every year.

The company did not go after very big ticket movies in the past. Based on public information, company looks to acquire movies which have budget of less than 10Cr. It does acquire some movies with larger budget of 30+Cr, but that number is relatively small. We need to keep tracking this part post company’s investment drive.

One cursory observation is - if a mid budget movie flops really badly, Shemaroo seems to own it. Maybe they get a good deal on such movies?

Another thing I thought of doing is to compare the hit Bollywood movies of the year in which company has 10+ movies.

e.g. Company owns rights for 12 movies for the year 2010, out of which I know only two movies - Bheja Fry 2 and Ishqiya. Now if you search for movies in this year, I thought there are many movies which would fit company’s profile of movie acquisition - Udaan, Phas Gaye Re Obama, Karthik Calling Karthik, Housefull, Golmaal 3 etc.

Just to further make this point, let us look at one more year. Company owns rights for 14 movies for the year 2005. I recognize only two movies out of these 14 - Black and Sarkaar. There are still many movies which might fit Shemaroo’s acquisition bill like - Page 3, Apaharan, No Entry, Salaam Namaste etc.

Maybe producers/distributors of these movies are themselves in second phase of monetization, or competition is doing monetization or Shemaroo does not have great relationship with these producers or they are just too expensive. Maybe super hit movie does not mean super hit economics for company?

GENRE

Overall, the company seems to be strong in Comedy and Action genre. I feel this is very good sign, as these two genres shall have very good eyeballs. I mean who wants to watch serious drama again and again, right?

One area where company is weak and can do better Romance/Romantic Comedy. I feel this genre shall also have very good eyeball numbers but company’s collection seems to be a little weak.

Another observation is that - if the content has “adult” connotation to it, then company seems to prefer to buy such a movie (although not a large proportion). There are many such movies in the kitty of the company. This also would be very sticky business and good for digital business I suppose  .

.

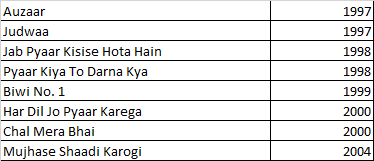

ACTORS

The company seemed to have acquired many (Pre-Supestar phase) movies of Salman khan that it can afford. I grew up watching a lot of his movies in school/college and almost all of them are owned by Shemaroo.

I also have had my fair share of being Govinda’s fan. Also Mithun movies still remain very popular when friends meet. The company has a large part of their movies which has both these actors.

Other two Khans (SRK and Aamir) and Akshay Kumar are completely missing from company’s kitty (Think Dil to pagal hain, Kuch kuch hota hain, Dhadkan, Baazigar etc.).

Also I felt young stars like Ranveer Kapoor, Ranveer Singh, Imran Khaan etc. are also missing. Again may be prices are too high for them? or not great relationship with these producers?

Overall, based on available information, I will say that company has average/satisfactory track record of acquisition and not an exceptional one. I would like to learn more information about acquisition side of things, how industry works etc. Based on that, these conclusions might change.

Views invited!

Disc - I hold shares of Shemaroo. This is not a buy/sell recommendation. I am not a SEBI registered analyst. Please do your own diligence.