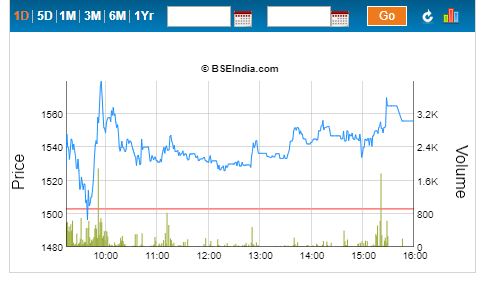

Real erratic movements in Shankara share price. See today’s chart and also the one I have put a few posts earlier:

Is it possible that someone is trying to manipulate the counter by spreading rumours? In fact just eyeballing the trading pattern it appears that the stock falls on small volumes in early part of the day, and rises on strong volumes in the later half. Of course I am just eye balling so can be mistaken.

I have an acquaintance who is on several market and trading groups on Whatsapp. I am myself not part of any groups. He showed me a message on the phone today (he had received the message on May 31) which said that 2point2capital has come up with a report similar to the one they had written on manpasand. However when I google “2point2capital Shankara” I do not get any results. While searching for “2point2capital Manpasand” takes me to their blog on that issue. So I am unsure if 2.2 has written anything on Shankara. Just seems a little bit like market manipulation.

Could someone check if there is any truth to the rumours. Please do let me know if this post is out of place, just a concern that I thought I should highlight.

Sir I humbly disagree with your accusation that I am spreading rumours. To spread rumours I have to present it as a fact. I have clearly identified that message as a rumour and also mention that my net searches support the contention that it appears in fact to be a rumour. Would request you to please not mis-characterize my post.

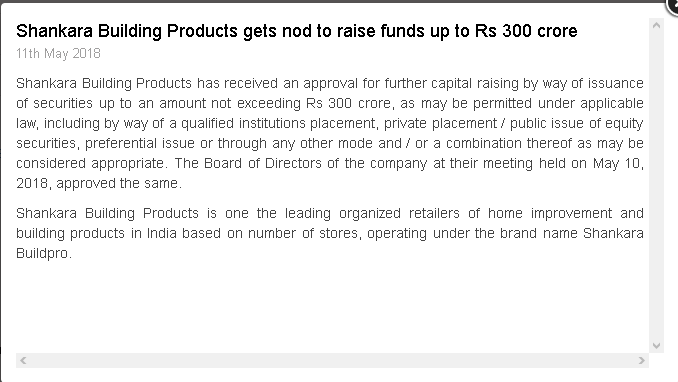

Why shankara build is again raising 300 cr via QIP though they just did ipo in last year? Why frequent dilution is going on for inorganic growth when organic growth is 25%+ ?or Organic growth is not sustainable?

Instead of creating new capacity (stores) in not so good locations it’s going after capacity in good locations at a fair price. It will then re model the stores to make more money. Not such a bad idea don’t you think ?

Here’s a couple of questions to ponder on. What’s the difference between organised and unorganised in retail? Is it only the ability to provide a fully paid tax bill? What then is Shankara’s competitive advantage?

Where’s the gap in the market it’s supposed to be servicing?

Shankara’s competitive advantage may not be organized retail. It’s just a general shift expected from unorganized to organized sector which will benefit all listed entities as they are part of organized sector which also includes unlisted players. This shift is because every transaction now requires a tax invoice to claim GST and therefore there are lesser rooms for cash transactions.

I think Shankara has the following competitive advantages:

First mover advantage. Being the only listed player in this space, they can easily raise money and expand at a faster pace as evident from the recent fund raising plans.

First generation entrepreneur with skin in the game and a high promoter holding aligning shareholder interest with management’s interest.

A number of moats (client, supplier, logistics) which will expand with expanding size.

Move from institutional sales to retail sales which has higher margin.

Both backward and forward integration with an ability to push more of their brands in their own retail stores which can increase margins.

Brand moat which will grow with increasing size.

Small base and a large addressable market.

There is a network effect in this type of business If the business can become huge. Being a first mover, this has a distinct advantage. Examples are Home Depot, bunnings in Australia. Even the second largest player finds it hard to compete with the largest.

Business will be selling a number of experience goods and hence very hard to be disrupted by online retailers.

This will be a relatively secular, stable business as GDP for India is expected to grow for a long period.

Franchising opportunity where the market is too small for the company to establish directly.

The market has identified this to be a solid business and hence the high valuations. Hope management can deliver.

Market certainly likes this stock - pretty clear from the way it is inching up from the recent lows.

Some questions that have been on my mind:

What is the sensitivity to raw material price? 50% of their revenue comes from own products. Q4 NP increased by 16% while sales increased 22% ( in fact company said retail sales increased 40+ percent adjusted to GST) . Given the low margin business (Q4 NPM was 2.85%) the sensitivity to any of the input costs is critical - I don’t think they have pricing power to increase prices in line with input cost increase.

Now that interest cycle is reversing, what is the impact of the interest costs? D/E seems okay (~0.5), but business seems fairly heavy on working capital.

Their NP fell from FY12-FY15 and then increased sharply from FY16 onwards. Do we know the reason for this? Is it only due to increase in retail share from FY16 onwards? I am trying to figure out is this really secular business or linked to some cycles.

Company is planning QIP ( I think about 300 Cr.). what is the impact of dilution on ROE/EPS?

They aren’t pure play retail as 50% of their sales is their own products. what would be the range of NPM for a manufacturer of similar products (I haven’t done that comparison yet)? Is their margin comparatively low/high?

Disc - not invested. On radar, but think it is expensive at trailing P/E of 50. I may be proven wrong by the market.

This Q was asked a week back when CNBC interviewed the MD. Please watch the video from 3:30 to 4:30 time mark.

Gist as I understand it is that the IPO was mostly to give an exit to PE investors and not to raise a lot of money into the company directly. Now that Shankara has also decided to add stores inorganically at good locations it may take advantage of market buoyancy to raise money for this purpose.

Being a B2C branded player, there is very little chances of margin contractions as it will be much easier to pass the swing in raw materials to customers. This will be relevant for the in-house productions. They will still be very low cost producers as they do not have a number of overheads such as advertising, sales etc. they will just have production lines. Also all retailers just pass on the cost swings so their retail side do not get affected by cyclical swings. So I think their business is not cyclical based on the commodity cycle. It may be cyclical based on GDP growth or construction activity. But the swing here will be much lesser and GDP for India is expected to expand for a long period to come.

Shankara will be in a better position to play the interest rate cycles than a number of unlisted entities as they can rise equity relatively easier and being a market darling raise at a substantially higher value than book value. So they can manage D/E ratio easier and use any opportunity in the market to inorganically acquire stressed assets as well. A number of Indian companies are in debt mess now. So it depends on the management ability to grow at the right pace and not do any debt fueled spending spree.

This is one of the rare companies at the beginning stage of its growth cycle. So I think we should not look much in to a couple of years blip as long as the sales are not contracting. Besides this was during the period it was unlisted. There could be a number of reasons like management band width, resources, economy etc for the subdued period. There could also be a few more such years to come in the future. I think what matters is how the management responds and bounce back. A branded B2C player has much better chances to bounce back due to stickiness with its customers.

QIP is for inorganic expansion. So we have to wait and see whether it will be EPS dilutive.

Their in-house production will only have production lines doing the basic commodity type products and selling at a premium through their own retail stores. So there is very little chance of this division not doing well. As the store count grows, in house production will grow. Even if at a low margin, they take the margins out of third party supplier and capture the profit ofentire value chain which will always be higher than the retail profit they get otherwise. So I don’t see them loosing here.

The biggest risk I see in this company is relatively less time being public. So management’s ability and integirty still is not well known. If there is any incidence like Manpasand, then all bets will be off! So portfolio allocation needs to be handled accordingly.

I didn’t look at Shankara for a while since at the face of it valuations seemed stretched. But the recent market correction piqued my interest. My research and thoughts are as follows.

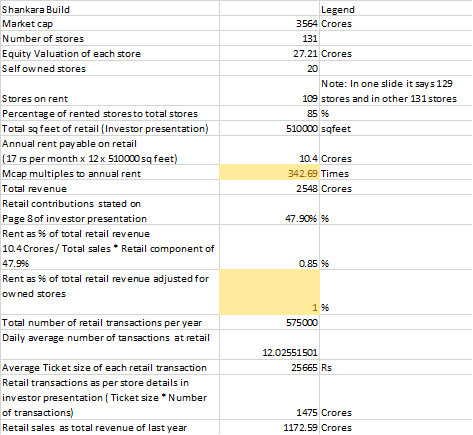

The runway growth is very long. India is at the nascent stage of organized retailing. This is more of a norm in developed countries where you don’t see a lot of one-off home improvement stores. This works because people find it easier to associate their needs with a known popular name. At this moment Shankara is not yet a known name in my understanding. So they have to build a brand and hopefully get there. But at a market cap of 3600 crores, I would say we are just scratching the surface of total home improvement market in India.

Growth to be propelled by sales growth in existing stores as well as opening of new stores. Management target 15 to 20% same store sales growth and intend to open 15 to 20 new stores every year. They are also open to inorganic growth via acquisition.

In Q4 concall management said that they do not have any competition in the listed space. They are going to get first mover advantage. The margins are not that great. After two decades of existence they managed an EBITA of ~6.9. This will actively fend off competition since it is not lucrative enough to attract them unlike for instance pathological labs. Even if we consider biggies like Walmart or IKEA they are strictly not in the same business, some products may overlap but is very minimal. For instance Shankara derives more than 65% of sales in construction materials. Besides the management clearly indicted many times over actually that they have established a process based on their learning of all these years that contributes to margin improvements. I don’t think a new player would be able to establish optimum process right from get going.

Management in Q4 concall said that capex per store is 1 crore (includes interior and structural work) and another 0.5 crore for inventories. So a total of 1.5 cr of capex per store. Somewhere I remember them saying (but could not find the source, so I could be wrong) that they break even roughly in over a years time which according to my estimates is bit of a overstatement. But still I think it is an asset light business - any incremental capital to service existing stores is almost nil except for working capital requirements. If they manage to build a name for themselves, the scope is very big.

Over time I expect them to accrue enough reserves which should propel capex for new stores since they only spend 1.5 crores per new store. So eventually for the kind of operations it does and the asset light capex that it demads, the company should become debt free and never have to raise capital. They should be able to fund themselves.

Risks

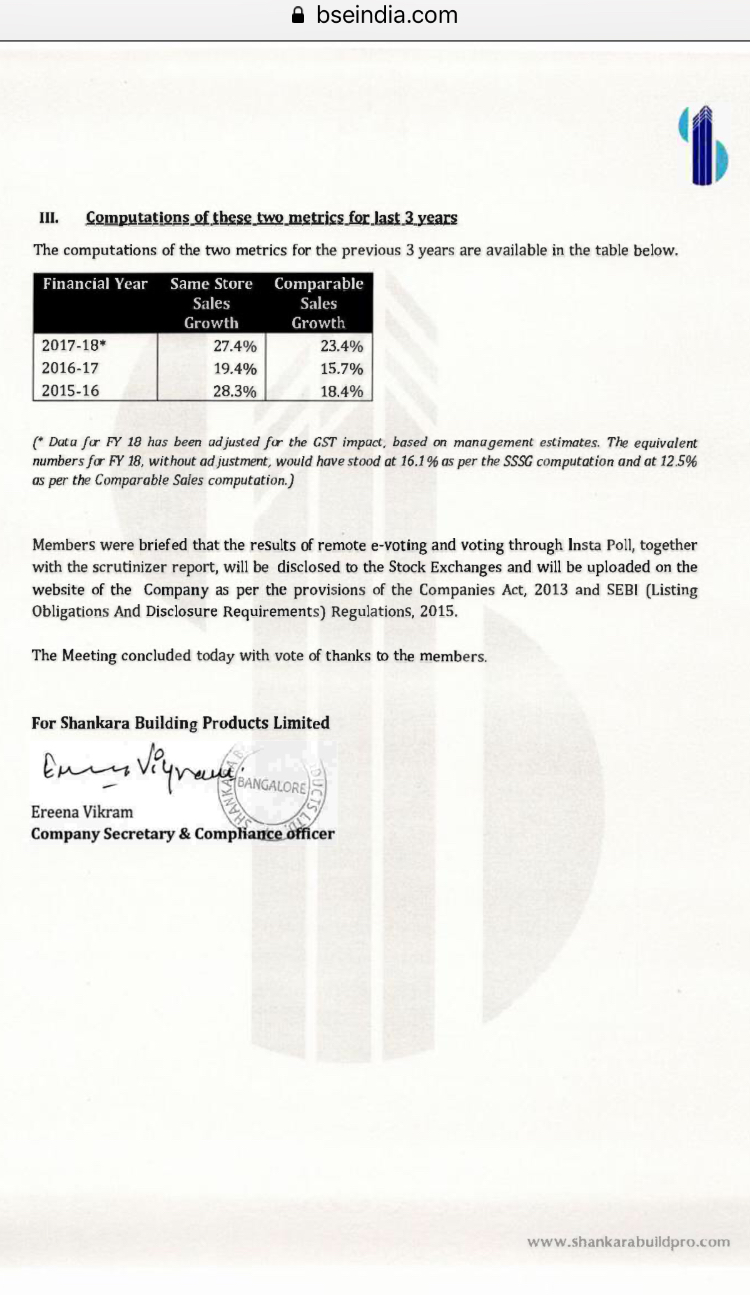

Same store sales number are consistently down. The management indicated that numbers between FY18 and FY17 are not comparable due to GST impact. Barring this, the revenues are up by more than 40% is what management said in Q4.

This is a cyclical business, although retail contribution will help a bit for consistency at the end of the day, these products are mostly one off usages. You will not see repeated customers if there are no new homes built. That being said, India’s average population is very young and I think we will have a lot of construction in the next 10 years aided by nuclear families.

This is strictly my opinion, may not be based on facts - I get a feeling that we are at the middle of the cycle. I read in many places FDIs on construction is peaking. Also a former employee of IIFL told me that IIFL recently created a realty fund for HNI with expected returns of above 14% whose only aim is to invest in realty. If we are at the peak of the cycle, these sales figures are positively influenced. What happens if the cycle reverses, will we see any growth?

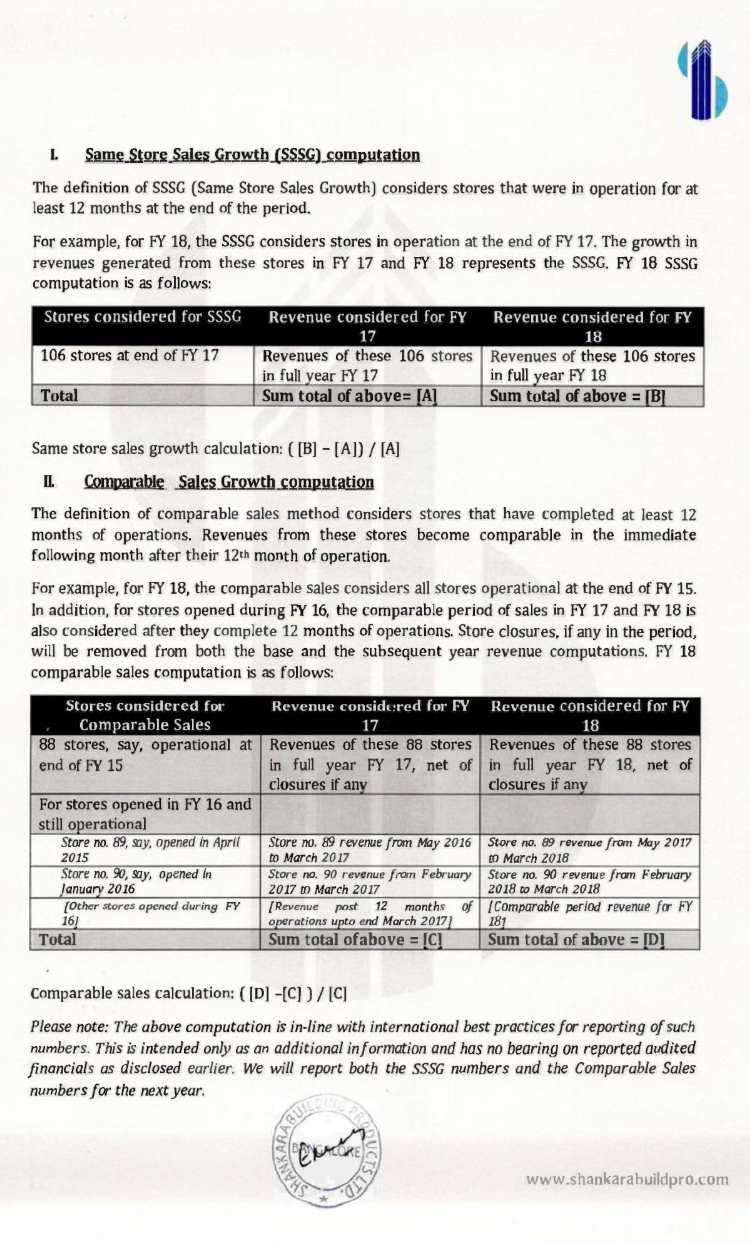

More of a question to fellow members. In Slide 27 of Q4 presentation lists same store sales growth at 16.1% but if I calculate the overall sales growth of FY18 w.r.t FY17 I only get a growth of 11.03% which is ominous. I do not understand how could that be mathematically feasible. Even if you assume 0 sales contribution to new stores, if the same store growth rate was 16%, should not the overall sales growth be more than 16% at the least? They however say that numbers are strictly not comparable due to inclusion of excise duty.

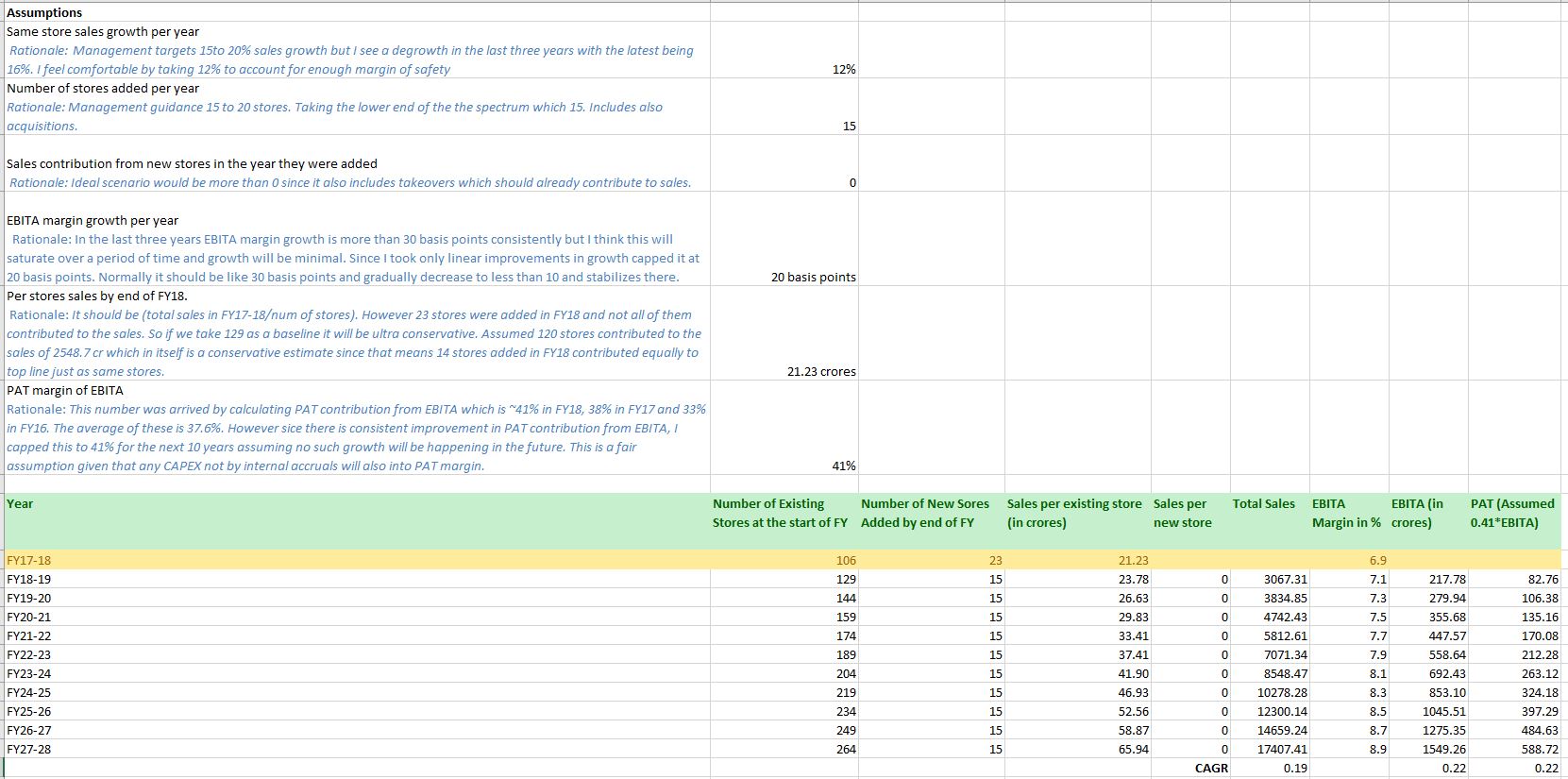

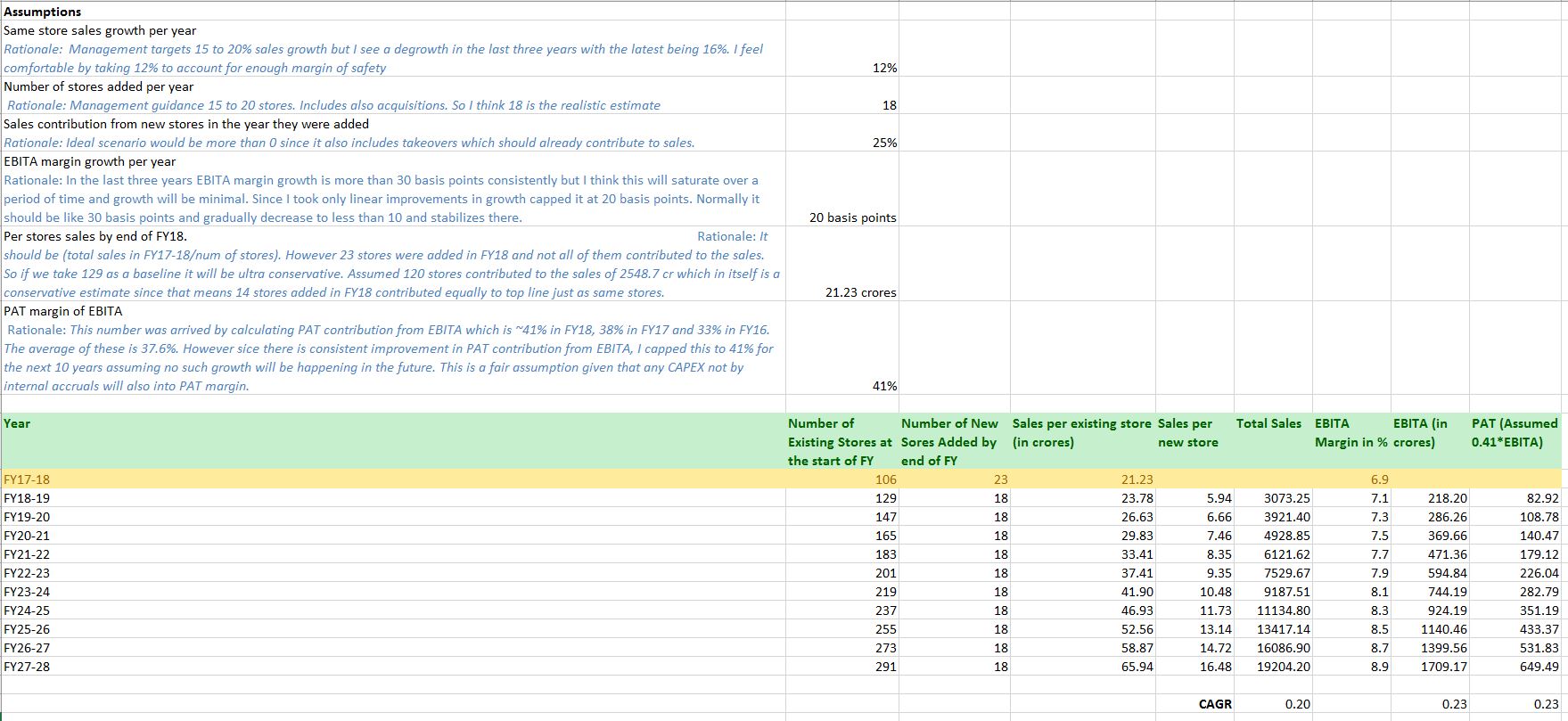

I did some guesstimates of future numbers. I made two estimates, a conservative one and a realistic one. The rationale for my assumptions are in the sheet as well.

The following is the conservative guesstimate of future numbers. Capex is not considered, perhaps I will extend it later with capex as well. Obviously these are based on information known to date. Any changes that affects these assumptions in the future will also affect the numbers. So these should be watched periodically to see if the assumptions are intact.

As you can see even assuming a sales growth of only 12% and new store sales of 0 for the respective year, overall sales CAGR comes to 19% and EBITA and PAT at 22%. This could be the reason market has a premium valuation.

The following is the realistic guesstimate of future numbers. Also for realistic I only considered a sales growth of 12% as I believe the present numbers are positively influenced by cycle tailwinds and when it changes we will see an impact.

The retail sales growth is 24%, 9807 to 12197 (same slide). Seems like you comparing total growth (not retail segment) to retail segment same store growth?

BlockquoteMore of a question to fellow members. In Slide 27 of Q4 presentation lists same store sales growth at 16.1% but if I calculate the overall sales growth of FY18 w.r.t FY17 I only get a growth of 11.03% which is ominous.

Shankara has corrected by 30% from its peak in the demonetization week. Technically the chart doesn’t look great to me and in my view there is a strong possibility of further downside after a failed cup and handle. There is a strong resistance at the 38.2% fib level and price action has failed to break this level consistently closing below it week on week.

The co is growing and taking on debt however its current return on capital is just about average and unless this piece improves in the future , it may not be able to sustain its current earnings multiple of 50 odd. In my view, those interested in the co should wait because there is strong possibility it may be available at lower levels in the future. At a 15% ROC , the multiple could further drop to maybe 20 levels in line with other cos having the same economics.