Hello, thanks for the post. May I know how you arrived at Capital Invested?

Hi ajith

5 Likes

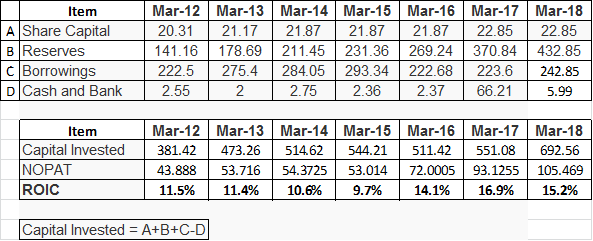

Thanks @bheeshma for the clarification. I broadly agree with you. There is quite some scope for Improvement in ROIC. Actually I hope for the price to come down. As a general remark, reserves are a snapshot of moment in time – i.e. reserves at the end of March 2018, how do we know if the company had the opportunity to deploy all the cash? This is something I was always confused about. How can we reliably correlate reserves and shareholder equity to the earnings since we do not know what was actually invested on the business. For all we know some funds could be parked in investments and were not actively deployed on the business. Perhaps that’s the idea, if a business is not able to generate better returns for the reserves it holds irrespective of how much cash was actually deployed in the business, it could imply that they do not know where to reinvest to grow. This could be an issue since if they generate enough cash reserves over a period of time, obviously ROC will go down.

I also see inconsistencies either because of sudden increase in reserves like in the case of 2018 w.r.t 2017 or stagnant growth in reserves between 2015 & 2016 coupled with improving NOPAT which increased ROIC from 9.7% to 15%. I believe the company is in a growth phase with huge runway. This coupled with margin improvements should aid better ROC. That being said, I also wonder what will the company do if and when they have cash reserves surplus so any capex should be easily funded by internal accruals.

Clearly for their plan of opening 20 stores per year – each with 1.5 crore of Capex, a total of only 30 crores. Perhaps acquisitions will increase it a bit but nothing too drastic I think. Over a period of time they will generate enough cash but can’t really deploy it to the fullest since their Capex requirements are not that demanding which might negatively impact ROC but Shankara is nowhere near that at this moment.

Disc: Invested a small amount but looking for entries.

The market pays this company a premium solely for its retail footprint and numbers. Maybe you could analyze it solely using retail figures. For eg with 1220 cr of retail sales growing at 35% a market cap of 3500cr isn’t too much. Maybe 6-8 months of time correction. A lot of people analysed Shankara on consol nos and missed out the entire rally. Technically maybe weak.

They will give the excess cash out as 40-50% dividend payout. This will cap the fall in stock price like Titan page etc. However this will happen after a long long time.

1 Like

Though I would not draw any parallels, could not help notice some uncanny resemblance between figures of Avenue Supermart (2012) and Shankara (2017)

1 Like

The fixed assets and share capital are obviously higher for Avenue Supermart as it has invested in its own stores. Other parameters too close and slightly on better side for Shankara.

1 Like

That is the reason i also like to call Shankar Build Pro the DMart of civil space.

Discl: Invested here.

1 Like

Thanks for drawing the comparison. There is a minimal but deliberate attempt at reducing the material cost for the Shankara, probably because they are dealing with raw materials rather than finished goods as Dmart. Fact that the former is giving dividends at the early part of it’s growth shows that the management is investor friendly.

Discl: invested in both

1 Like

The company claims to sell 4.5lac tons of construction steel in FY18 up from 4lac tons in FY17. If we take Rs 30k as weighted avg selling price, this comes to about 1300-1400 cr out of total sales of 2550cr during FY18 without taking into account steel processing margins (Could be another ~100cr). It was rightly asked by one buy side analyst during Q4 concall about inventory gains and surprisingly they had only 5cr of inventory gains. For all practical purposes this is a commodity steel processing and retailing company. My analysis suggests that all major steel processors are having strong inventory gains but the company claims to go for volume and customer satisfaction which seems ok. I am not sure why would one compare same store growth since steel must be directly shipped from the processing centre or warehouses. IMO, comparing it with other retail company like d’mart will be completely wrong.

My understanding of the Bangalore market suggests that upper middle class doesn’t count it as a preffered supplier/shop for their interior work. Discounts are less in Shankara while they do have large SKUs, nearby hardware stores do promise delayed delivery if something is not available immediately. Let’s face it - a guy building a house need not buy everything right away as it is ordered in advance. It is quite different from D’mart’s FMCG sales where a customer need to pick up the stuff right away from the shelf and hence store size matters. Only independent house builders find it convenient as they run credit account with it. It is not a characteristic of a company with deap moat as yet. I beleive they are in the process of graduating from selling steel to other related stuff like paints/plywood etc. Hence, I believe it is premature to justify TTM PE of 50. A detailed analysis of how are they reinforcing their competitive advantages must be carried out. I am not implying that selling commodity grade steel from organised channel is a poor strategy. We must note that there are no large scale integrated steel processor and retailer.

Dis - no holding

7 Likes

Curiously a group of insiders make a raid in the stock market and buy 100-1000 shares between 1st to 5th June. Don’t know what kind of signals they are trying to give.

How did you come to know such a low volume transaction is attributable to insiders? Pls substatiate

Recently… Crisil releassd notice for suspending their ratings for want of some necessary info for rating review.

Crisil mentioned that same is not provided by company inspite of repeated efforts.

Same is notified to exchange by company.

Any comment from forum members?

Since we have many people in this forum who have proficiency with valuations, I think it would be a good move to get their views and aggregate them to get a sense of the numerical range within which we could call the co fairly valued.

My sense is 18-20 times 3 year forward EPS would be reasonable to pay assuming a 20% growth in EPS. The valuation thus comes to 1116 - so a range between 1000 - 1200 would be a good range. I think its a good co but at current valuations, its not going to go up. Aggregate views on valuations could help in balancing optimism or pessimism and cut through the noisy bits of information.

Best

Bheeshma

6 Likes

Insert Shankara in the designated field in the link below

https://www.bseindia.com/corporates/Insider_Trading_new.aspx?expandable=2

Thank you for the info. This kind of token purchase may not in all probability signify anything except , may be, to rekindle investor interest.

I might be wrong in my hypothesis but a lot of earnings in Shankara is just steel inventory value gains which the company is not recognizing properly. I see annual earnings acceleration coincides with strong recovery in steel prices. Steel px have gone up in Q1 as well and that’s why they seem be in hurry to conclude fund raising. There is wide spread expectation of long stagnation if not correction in steel prices going ahead. I think there is valuation downside here and I would not touch it above 25-30X trailing.

4 Likes

Per my valuation, the stock is overvalued by 10% based on the current market price. My investment thesis in this stock is based on margin expansion (to be aided by move from institutional to retail sales, own brand sales, same store sales growth), accelerated sales growth (organic and inorganic route, long runway) and increase in ROE (aided by margin expansion. So while I agree a sales growth of 20% looks feasible (organic route which could increase from meaningful inorganic expansion), I used a higher profit growth of 25% for my valuation.

Q1 Fy19 - Overall flat results mainly because the Profit margin is shrinking.

Sales up 32.72% yoy

Net Profit 13.01% yoy

Operating Profit margin at 6.22% dipped -0.44% yoy

Interest cost up 41.46% yoy, up by 0.98% qoq

Shareholding Patttern

Promoter increase stake by 0.01% qoq

FII increased stake by 4.52% qoq. FII holding 19.21%

DII holding decreased by 2.40%

Amansa holding 5.42% - largest public shareholder

1 Like

Did any one analyse the latest results? Why did the profit margins reduce in spite of higher retail sales? shouldn’t it have been the other way round?