Doing a deep dive into this company and have few queries. If people who are tracking/invested in this company for quite sometime can take sometime out to answer then it will be really appreciated:

They target $100mn sales by 2020, which is like 670cr i.e. c.30% CAGR in next 4 years. Just want to know whether the management has achieved the guidance in the past (or this is the first time they have mentioned any targets)? Just trying to understand whether the management is very over bullish like Kitex and tend to miss the guidance every time?

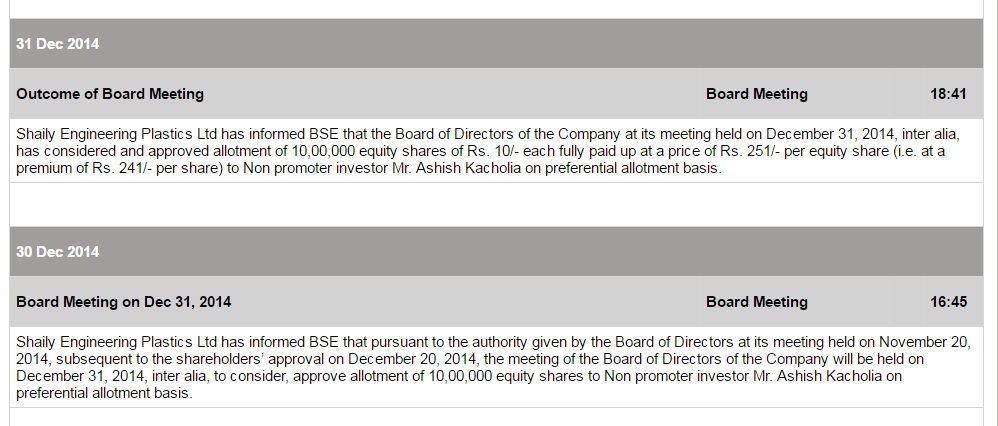

Looking at the FY16 numbers, it seem that equity dilution has happened i.e. they have issued new shares. Pardon my ignorance but what was the purpose of raising the money (expansion)? and is there any further dilution lined up in future?

Hi Mukul,

I do hold shares in this company and had been tracking regularly. I will take the 2nd Question first:

The company has diluted shares in private placement to Mr. Ashish Kacholia. You can find it in BSE Cop. Announcements. Screenshot is below

Thank you so much Brijwanth for replying. What are your views on the next year guidance of 20-25% growth plus 100bps margin expansion. I am trying to understand if historically they are aggressive with their guidance and not able to meet it OR they are prudent and more or less meet the guidance.

The reason I am asking this is because as per my understanding some of this high growth is already baked in the stock price (with a p/e of 30x).

IMHO they have all the reasons to grow Sales at 20-25%. They have capacities built up -CRC’s in the pharma side to gorw that aggressively. The 100 Mn $ does seems to be aggressive unless some inorganic acquisition happens which is highly unlikely. We can expect to endup at around Rs. 450 Cr. if no black swan event occurs. I may add here that the company will get a boost if crude/ plastic prices move up, then you can see the real growth.

As per latest transcript they have processed 66% higher volume but revenue increase only 25% all this volume growth will multiply when prices move higher.

On the valuation side the share is illiquid so expect some premium, moreover it’s running at 1 year forward of 24 pe which is totally reasonable for a 25% compounder.

They had already started de-risking themselves from single biggest client. Ikea sales used to be around 55% of revenue & now it is around 45% of total revenue. Shaily management completely understands it and hence there main focus now is in Pharmaceutical machinery.

Company started a new project, last year named CRC Project for development of business. The major products are CRC Cap, 120 ml Bottle, 100 ml Bottle, 60 ml Bottle, 40 ml Bottle etc., and is working with various Pharma Companies for sales of the same.

Company is targeting for $100 million sales by 2020, with current sales at around 225 Cr.

Not that it’s impossible. But to do this:

a) Company has to move up the ladder & cater only the high value added / High margin products. Even though the company is doing it currently to an extent, this clearly says targets are little aggressive in nature.

b) Not to forget Amit Sanghvi in his recent interview said the margins can expand upto 18.5% this year (on a positive note, there was a continuous improvements in margins year after year). This may boost the PAT little faster to achieve target.

c) Management has also said they are open for any acquisitions. And this can be a trigger to achieve the 2020 target.

d) Another major booster: IKEA to expand aggressively and plans to open 25 stores in India by 2025, with first store coming in Hyd by 2017. IKEA wing of Shaily had grown at 170% CAGR for last 3 years.

Over all, I feel Amit has set himself high targets. I will be happy even if they reach little close to it.

Krishna, Please rectify point one.

As per Annual Report,"The Plastics Industry grew by 13 per cent annually in the last five years and is expected to continue a double-digit growth beyond 2016-17, according to a study on Plastics Industry. In order to cater to the increased demand of plastics consumption, the plastics processing industry will need to grow from a current installed processing capacity of 30 MMT to 45 MMT per annum by 2020."

Thus, 30MMT is current industry capacity not Shaily’s

Today just looked at the fundamental side number.looks quite impressive but one thing that I have identified with this company is that in spite of such good fundamental why it is in t group?

When certain stocks get too frisky, they get sent to the T group to cool off. It happens all the time and is not always a reflection on the company. I recall times when current favorites like Avanti Feeds, MPS, CanFin Homes were T category stocks.

@parasonly Sorry I dont know about that. The exchanges do publish a list of which stocks are going into the segment and which are coming out of it. You can check on their websites.

Which comes to around 12%, is it not less than the past ?

2005-2015 -Consumption of Plastic polymer grew by 15%CAGR

2005-2015 -Export of Plastic products grew by 30%CAGR