Comprehensive info on Shaily in a credit note by CARE.

Shaily Engineering Plastics: Firstcall are overweight for medium to long term investment

1 Like

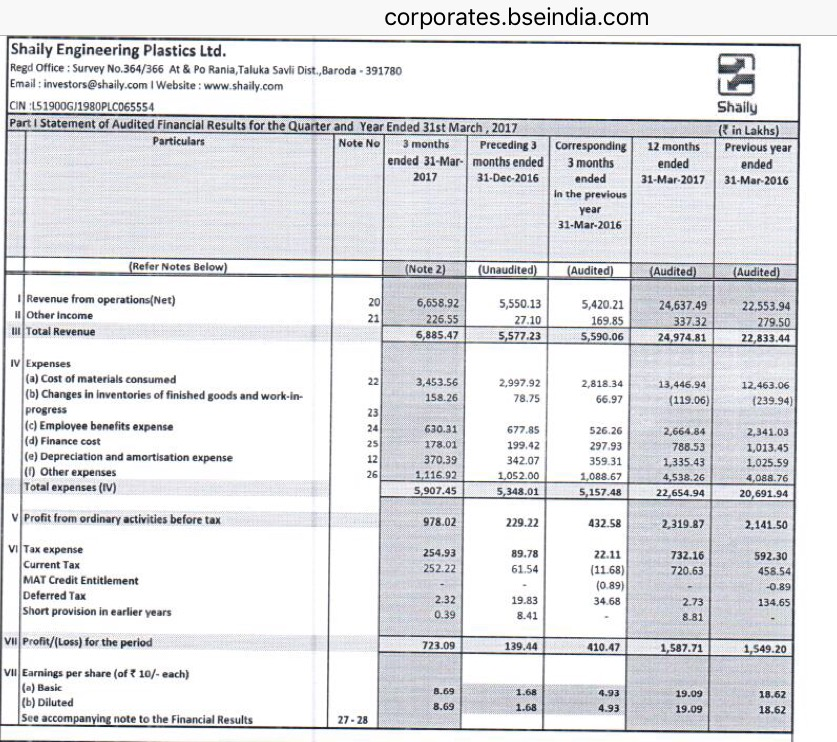

Q4 FY17 Results:

Investor presentation:

http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/fa1b25ad-863e-41d3-991f-9c48cb2a86ea.pdf

2 Likes

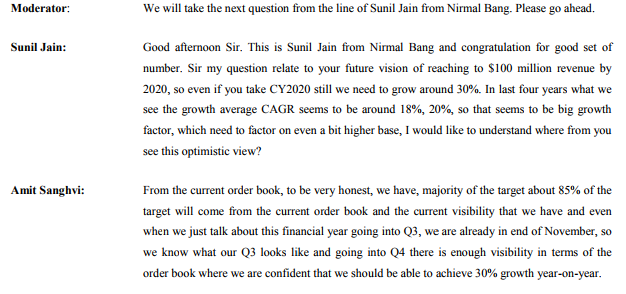

@ayushmit, Read the Q4 conall, saw your name, hope it is yourself, any views on the overall business here will be helpful : their target sales of 100MN $ by 2020, Pharma business and scale up, also home furnishing business, are the costumers are sticky for long association because of the quality of the products Shaily is doing ?

Regards

1 Like

Good set of numbers. here is the link to the Q1 presentation.

http://www.bseindia.com/xml-data/corpfiling/AttachLive/2861ea80-62da-47f9-a13c-441a9870ea7e.pdf.

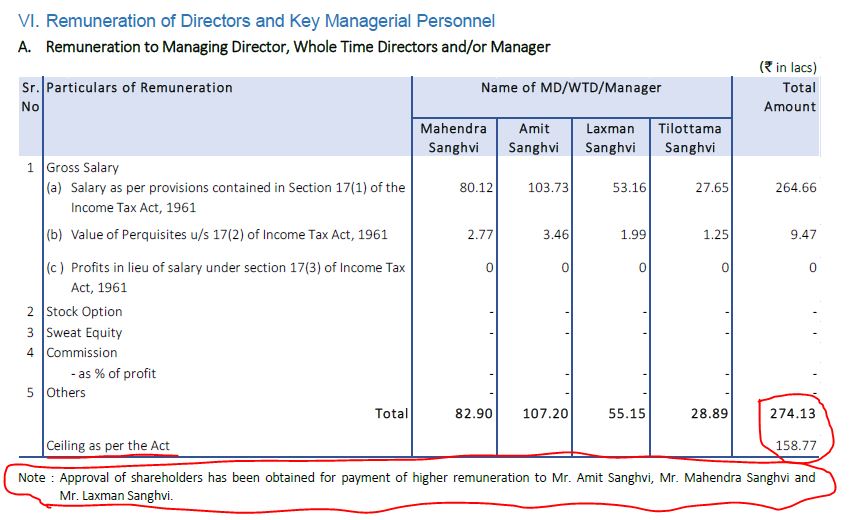

As was the case in the last year’s annual report, even this year the remuneration of the Key Managerial personnel is more than the Act allows for. The AR suggests that the company has taken shareholder’s approval for this. Is anyone aware of the reasons the company provided while taking shareholder’s approval for this?

1 Like

Any idea how is the ceiling for remuneration determined ?

By section 198 of company’s act. Shouldn’t be more than 10% of profits but the profits here are not the same as PAT or Pre-tax profits. I think the Act allows for certain deductions to arrive at the quantum of profits considered for this purpose.

1 Like

Shaily Engineering Plastics is showing good growth in both topline and bottom line. The kind of customers company acquiring in pharma and home furnishing sectors and the fact that company is completing a major expansion plans in tooling parts and CRC plants & the ambitious target to increase revenues by more than 200% in next 3 years does augur well for the future prospects of the company.

Current quarter(Q2FY2018) company has shown an increase of reveues by 21% YoY basis and 33% increase in PAT YoY basis which again shows company’s capability on executing its vision of reaching a revenue target of $100Million by 2020

Disclosure: invested a month or two back.Might increase holding based on company’s ability to execute on it’s vision in coming quarters.

Where did you get this ?

This is from company’s vision statement

"Become a USD 100 million plastics manufacturer with a Global footprint by 2020”

So company has some INR 200+ crore now, which translates into close to 200% increase in revenue…

Even if the company can increase by sales by 100% and if operating leverage kicks in that translates into 30% CAGR in profits…which is something I still consider as a good performance

Note: I considered 1 USD=65 INR today and with a differntial inflation rate of 4% between USD and INR IN 3 years USD will be 73 INR…so 100million should translate to a revenue of INR 730crore in 3years…whether sales target can be reached or not depends on firm’s ability to execute on vision and how the operating leverage will play out

But how come, currently its revenue is 250 Cr , So it comes to around 38% CAGR to make it to 650Cr in 3 years, I remember couple of concalls back they gave 15-20% CAGR growth projection for FY17-FY20. With these kinds of oscillating statements now I am getting concerned with management.

Pulled research bytes(https://www.researchbytes.com/webcast.aspx?WID=128858), I think 15-20% was FY17’s projection, FY17-FY20 was 30-35%, around 19:00 min he speaks about 30-35% growth.

Plastic being low margin business means he will need to increase their debt substantially to get that growth, currently it is around 65Cr which I don’t think is enough to fund the planned capacity. I am comfortable as long as they can keep debt to equity below 1.5. Remember how PAT squeezed in 2010-2011 when it went beyond 2.

Let’s hope company executes on its vision…i just don’t want to jump to conclusion. Every contract manufacture starts with low margin and depending on how it transforms itself and its capabilities through R&D investment, determines their future prospects and margin expansion. I strongly believe not all companies need to be seen from existing moat perspective but how they can reinvent themselves to execute and build a moat over a period of time

1 Like

The encouraging aspect has been the greater share non-cyclical sectors like home furnishings and healthcare. This may lower volatility in both top line and bottom line. Custom manufacturing is also reducing Volatility in margin as RM cost can be passed on.

Brief notes from the Shaily Engineering concall today

Shaily Engineering Plastics – 2QFY18 results concall update

- During 2Q, revenue, EBITDA and PAT increased by 21%, 23% and 33% respectively. Achieved, 1HFY18 revenue and PAT growth of 20% and 31% Machine utilization is up to 82.1% compared to 67% last year.

- Volume of polymer processed at 3,374MT is up 22% YoY. 72% of total sales are exports for the 1H.

- During the quarter, the company received new business confirmation from 3 large pharma companies for pen devices. The company also successfully converted a metal part to plastic for Honeywell. It is currently catering to 15-16 pharma companies worldwide.

- CRC cap facility is currently operating at 60% utilization. However, the actual CRC production is much lower as the commercial dispatches for the product have not materialized yet. The management mentioned that the gestation period for the product has turned out to be much longer than expected.

- Based on the current capacity, the company can achieve Rs425-450 cr of revenue without incremental capex. The target for US$100mn revenue by FY20 still stands. The company needs to grow at 30% rate to achieve the same from the 20% rate seen in last four years. The management mentioned that the capex of Rs30cr per annum is enough to generate the targeted revenue.

- The stock is currently trading at ~30.0x to FY18 PAT.

3 Likes

2 Likes

Q2 HY1FY18 Earnings Call Transcript:

http://www.shaily.com/webfiles/InvestorPresentation/Q2-HY1FY18-Earnings-Call-Transcript.pdf

1 Like