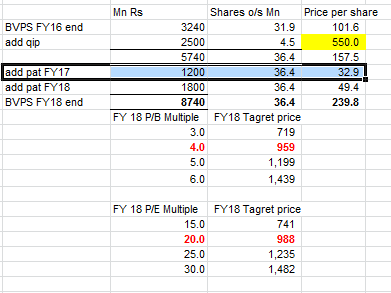

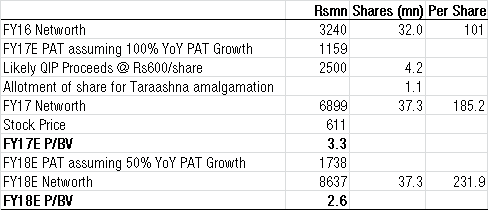

Satin has reported good results, ahead of my expectations. PAT growth 100% yoy and EPS growth ~80% yoy. I update my numbers for FY17 PAT to be higher by 20% vs previous expectation (assuming QIP is done in Sep).

Taraansha benefits not factored in yet, will wait to see before incorporating.

At 600 Rs its trading at 2.5x P/B FY18 and 12.5 P//E FY18. For a 20%+ ROE and 50%+ growth business, this does look attractive in the negative yield world

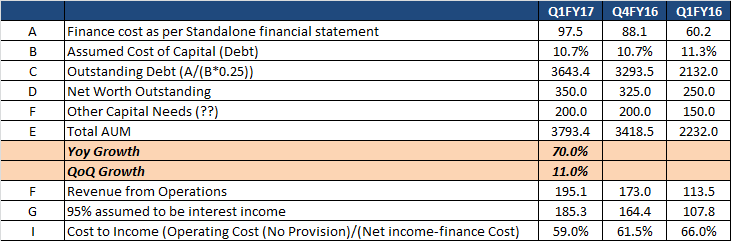

The investor presentation has not been updated yet and no balance sheet in the results. Have done a basic analysis to ascertain AUM. Looks like it has grown 11% QoQ and ~70% YoY

If the assumption about the AUM growth is true, then the interest yields have also stayed flat - which means no pressure from SKS entering the North Indian Markets (as SKS is known to charge lower interest on its MFI loans)

On the cost and operational efficiency front, again there is an improvement both QoQ and YoY-

Will do more detailed analysis and keep sharing. Happy Investing!

Thanks for the analysis Deebee. One thought is, I would be very surprised if pricing pressure shows up in thsi business. JLG borrowers do not switch for a few basis points like a soverign fund debt investor Remember this is a sticky business, even more sticky than our Savings account relation. How many switched Saving accounts when Kotak/Yes offered more rates?

Some borrowers have 2 relationships but low cost producer SKS has very litle pentration yet as you pointed out. Will take time for them to establish relations.

Good progress on cashless - 25% now

Strong network growth - 100 bracnhes, 1000 emp added

NPA - "They have been steady in the first quarter. I think they will remain fairly steady over the next three quarters also.

FY17 PAT of 1159 and net worth of 6899 imply an ROE of 17%. You are underestimating PAT input from Tarashana. ROE cannot drop below 20% inspite of dilution

Not arguing on conservatism but it makes sense to raise equity only if you can drive growth. Doesnt make sense to take the dilution and not grow either (double whammy). If that is indeed the preference then we should all invest in Equitas - capital raising without a consideration for ROE.

Both Venkatesh and my numbers are conservative on multiple reasons:

We dont giove the Taransha benefit that can be very positive for earnings and returns

As scale increases credit ratings will improve further reducing cost of funding

Scale and technology investments will help reduce ope/assets and

Value growth per customer as base deepens will be higher margin and higher returns

Management imho has multiple levers to raise and beat expectations which is comforting.

Like Venkatesh said, better be conservative I like margin of safety on both earnings and valuation (950-1000 Rs ps FY18 target in my post above is based on 4x BV and not 6x which Mr Market may give at some point). We are half way into FY17. FY18 will enetr the windshield in 6 months

“Time is the friend of the wonderful company, the enemy of the mediocre.” - Warren Buffett

A ratio where the numerator is as of today and denominator is two years hence is internally inconsistent. “Forward” ratio of any type such as Forward P/BV or P/E should discount the denominator to today’s date using an appropriate discount rate. Otherwise it is bound to give misleading results.

In some of the earlier conversations in this thread (may be by others), that has not been done. I was referring to the general principle only. Apologies if it was not clear.

Dont think MS PTE Holder or QIP buyers will get any space on the board. They are all capital market investors. its only the PE guys who usually get a board seat.

My understanding is, anybody with material stake can ask for seat, irrepsctive of where they bought from. The whole world of Carl Ican type activist investors work on this basis in teh west. Not sure if its different in India.

Remember this is a sticky business, even more sticky than our Savings account relation. How many switched Saving accounts when Kotak/Yes offered more rates?

Remember this is a sticky business, even more sticky than our Savings account relation. How many switched Saving accounts when Kotak/Yes offered more rates?