It is just the p note

I suspect its amansa capital (akash prakash). they have built a sizeable position in sks too.

1 Like

We have previously discussed what the right discount Satin should be vs SKS. Given higher growth, improving but lower returns this was subjective in my view. However the recent reports on higher penetration in southern states of TN, AP might drive one to think if Satin should be at a premium given its geographical expsoure to relatively virgin UP, north? Just a thought

1 Like

Do you think 450-500 will be the right price if someone wants to accumulate more?

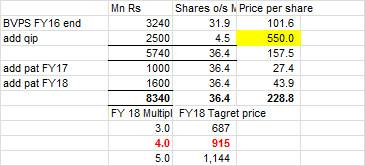

I would think so Akhil. I think at 4 x FY18 book of ~750-800 I would start worrying about valuations, not at current levels. I think the recent correction is good as it prices in skepticism into furture earnings. As Satin demonstrates earnings and executes QIP, skepticism will get priced out. Beyond 800 optimism starts getting priced in. Optimisim will be well deserved if they execute well for some time.

Why 4x? Growth of 40%+ over 3-5 years and ROE of 20%+ deserves more than that (see Gruha). Apply some discount on sustainability given the risks all of us are aware about and worry about.

Thats my view, who knows what Mr. Market thinks…

3 Likes

Satin Valuations. Below are my simple back of the envelope estimates on BVPS FY2018. We can get above 900 on 4x P/BV:

6 Likes

What is the comparitive calculation for GRUH

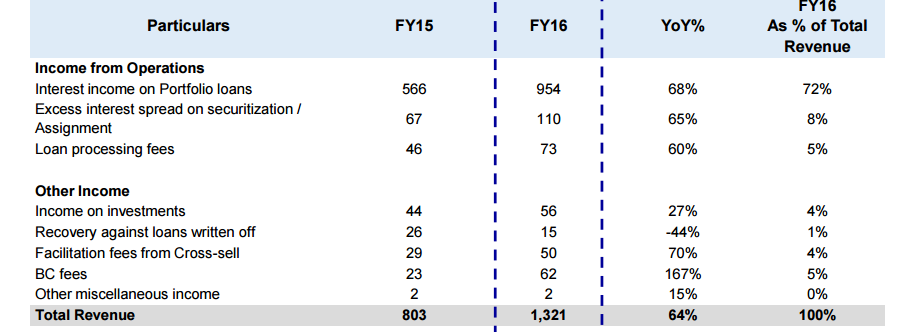

I think the the most important point that the market isnt fully appreciating yet is the merger of the Tarashana subsidiary (BC). BC is a 40-45% RoE business with pure fee income (no balance sheet expsoure, just originating for other banks). Since the Small Finance Banks (Ujjivan/Equitas) are no longer allowed to be BCs to other banks, this business will explode for Satin, given the markets it operates in.

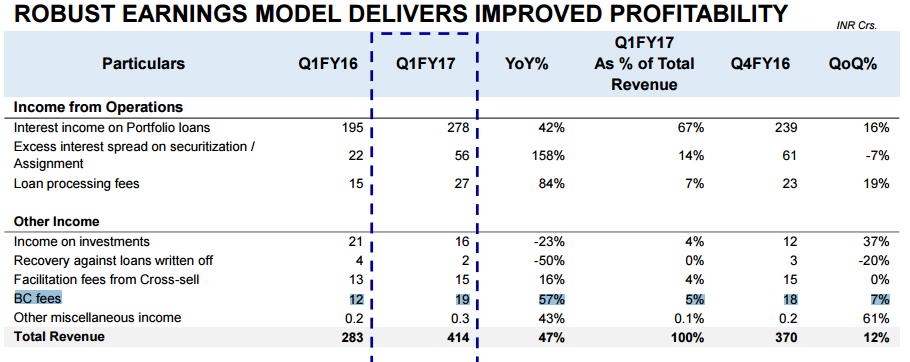

SKS doesnt do much of this, given its scale and its cost of funds but even there the number grew 167% this year (See BC revenues 23 cr to 62 cr in FY16) and again 57% in Q1 FY17.

Unless something dramatic changes, I dont see why this cant be a 30% RoE business (adjusted for fund raising) that is growing at a 100%.

Even if you assume a business of such nature should trade at 18x trailing P/E (Nifty is at 19x), the P/B should automatically be 6x trailing P/B (P/E * E/B = P/B = 18x * 30% = 6x)

Disclaimer - Own since 300 levels and bought more around 550

7 Likes

Very interesting analysis pegiy, thanks for sharing.

If I give Satin benefit of higher earning growth in FY18 post Taransha full year and apply 6x P/B, I get FY18 BVPS of 250 and 6x would be 1500 Rs per share!!! Wow thats almost 2.5 x from current levels! Perhaps this explains why MS/MS client is building up such a huge stake and keeps buying at 650+ price also…

Is Tarashana a wholly owned subsidiary of Satin?

See June 30 BSE filing “3. Acquisition of Taraashna Services Private Limited (“TSPL”) as a wholly owned subsidiary of the Company by purchase of entire shareholding of TSPL from its existing shareholders through share swap and consequential preferential issue and allotment of equity shares of the Company to such existing shareholders of TSPL, in accordance with applicable laws;”

1 Like

Potential market size may be guessed -

25-30 cr. total households in India. Let us say 15 cr. of these households could potentially use microfinance of average amount of let us say 30,000/- taken for a couple of years.

Average outstanding debt for these 15cr. households will be the mean of 0 and 30,000 = 15,000/-

So, the potential size of market = 15000*15 cr = 2.25 lac cr.

so, when managements of MFIs or investors like Basant Maheshwari etc. say that size of market can’t be estimated, one shouldn’t believe them because it can be roughly estimated imho.

Disc: invested in Arman n Satin.

2 Likes

I don’t think Satin would get a book value of 6x FY18. Even biggies like Bajaj Finance don’t trade at such valuations (BAF touched 6x temporarily and then saw a 15% correction). Same with Bharat Financial as well.

Thats a scenario. My base case is 4x, as I mention in my posts above. However if Taransha merger related benefit and growth/qip execution is better than what I and market factor in, can see a scenario where it goes to 6x.

Further to teh post on PE/VC exits Satin Creditcare Network Ltd - Reaching out!

Interesting to note that Shore Cap is compeletely sold out in open market http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/4F62BB2D_64C9_4438_BC1F_E4DB3AAD8FE9_081809.pdf

Looks like MS Asia/clieng has picked up http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/A92E69C4_4B2C_43B3_9664_24BB4D9BD114_170354.pdf

Look forward to seeing how stock behaves with this overhang of Shore suppl;y removed…

1 Like

Shore Cap was old investor in Satin. If prospectus of the company is going to excellent why they sold completely their holding? Why they are not comfortable in so called excellent growth of MFI?

If you look history of Morgan Stanley for their major holding in any single equity, the equity crash like anything when they sell it. Their selling normally brutal. sometime its strategy is totally unpredictable!

Hnk_so this has been discussed and i have posted the link to the same in my post above also. Please make the effort to clikc and read. If yiu want to respo d pls respond to that so that their is incremental value add to the discussion instead of repetition.

3 Likes

Shorecap appears to be an early stage investor (VC type). They appear to be getting out because Satin would have matured as a business and their mandate will be to be early stage. NEws today of their series C funding an early stage MFI:

" Bengaluru-based Chaitanya Rural Intermediation Development Services Pvt Ltd, has raised Rs. 47 crore ($7million) from Equator Capital‘s fund ShoreCap II and a few high networth individuals.

Read more at: http://www.dealstreetasia.com/stories/49867-49867/"

Their objective, as stated before is not just profits. Timing and stage of venture are factors. Equitas/Ujjivan have appreciated considerably since smart money PE’s exited at IPO.

2 Likes

Shorecap invested in Feb 2011. I dont know of too many investors who stay invested past 5 years. Other PE investors who came in later are still holidng - MicroVest, Norwegian Microfinance Initiative, SBI FMO, IFU (investment fund owned by the Danish Government

1 Like