Have patience it listed on 27 aug 2016

yes sir. Just was hoping they execute quickly given market price action (getting nervous)…hope they raise at good valuatons

yes sir. Just was hoping they execute quickly given market price action (getting nervous)…hope they raise at good valuatons

Everyone wants to start their own microfinance business nowadays…

Exclusive: Satin Creditcare Network COO Vivek Tiwari steps down

BY JOSEPH RAI

…

Read more at:

I would have done the same. This on the ground expreience is super valuable. The hard to replicate on the ground network, intelligence and judgment is what makes these businesses moaty (besides the scale!). Great time to monetize this experience, if one has a long term positive view of MFI potential.

As an investor, top management switching from salary to equity (thus putting skin in teh game), shows their confidence in the medium to long term prospects of the MFI business in India.

1 Like

Why will a MiddleClass Household use MFI…?? Why will your family take loan at 22% when they will be easily able to get a personal loan at 14-15% max from ICICI

1 Like

The purpose of my post was to show that potential size of market can be calculated and those saying 2.5 lac cr. is 10 yr old estimate and current figure may be much larger etc. aren’t necessarily right.

Many poor and lower middle class people will go to MFIs for hassle-free smaller-ticket loans with comfortable repayment-instalments where the MFI will follow-up for collecting the instalment. you wont get this from banks . In a monthly instalment, interest rates make a difference of just 5-10 rupees. So, interest rate is not as big a factor for the borrower as it is made out to be.

1 Like

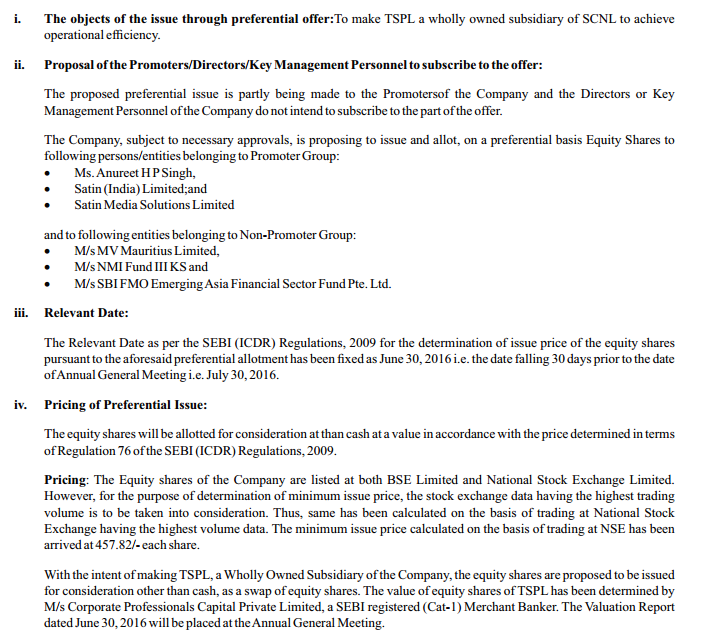

Satin has issued shares to promoters and current shareholders for ~50 cr Rs @ 457 Rs/share. I think it is positive that existing shareholders see value to infuse more money in the company, ie, they too see value Satin has highest promoter holding of all MFI’s and they are trying to retain % share.

Speculative but could be signalling ahead of external fund raising in QIP.

1 Like

Was it based on warrants issued earlier?

Is this is the 1.1mn share issuance for tarashna amalgamation? If yes then okay. Else this is not good.

Latest Satin investor presentation:

1 Like

According to the last few BSE filings, SATIN has done Asia roadshow meetings. For a QIP sized 250 Crs, Asia is usually enough to market the transaction. Let’s hope the feedback is positive and that the company is able to wrap up the fund raising process at the earliest.

2 Likes

SKS QIP for 750 crs launched got demand for 10x. Wonder when Satin will do its QIP?

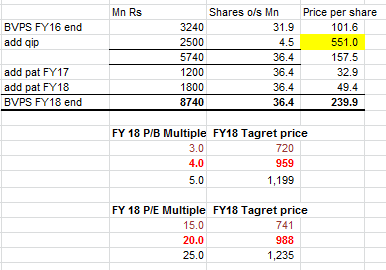

QIP update: Satin announced full subscription and issuing price today. I have updated my numbers based on that:

8 Likes

Kotak acquires small MFI business with distribution in UP, Karnatakas, Maharashtra for ~10 P/E ~2 x P/BV.

From the MFI point of view smaller ones will want to be acquired by large insti to access capital. Capital is the fuel for growth.

What increases my confidence in MFI and my holding period horizon is how the smartest money in Indian banking - Kotak, Indusind, IDFC - is investing in this space. This is super smart money with long horizons. They are planting seeds that will grow into trees…gives comfort to be aligned with them

From Satin’s perspective, it is interesting that their book <40 Bn Rs is very interesting for Indsuind (~30 Bn MFI book with aspiration to reach 100 Bn in 3 yrs). Distribution is also complimentary (North vs Indusind’s CV in SOuth) Off course Satin already have access to capital on equity and debt so promoter may not have interest to sell.

4 Likes

Why satin credit–company- cash from operating activities are standing negative ?

hi friend can u tell me, debt per share at present is 376 per share and it is rising why?

1 Like

Those are not relevant numbers for analysing a lending business. Focus on ROE.The cash flow statement is meaningless here.

3 Likes

You mean are we not concerned of our money blocked with improper customers when we are doing lending business which increases our cost of funds, As we know owners funds dont carry interest but funds borrowed carry interest, if funds borrowed are locked with customers and realising at slower rate…cant it pressure on balance sheet???

Not justified reply : You mean are we not concerned of our money blocked with improper customers when we are doing lending business which increases our cost of funds, As we know owners funds dont carry interest but funds borrowed carry interest, if funds borrowed are locked with customers and realising at slower rate…cant it pressure on balance sheet???

If that is the case , Why ROE is at reducing rate with increasing long term borrowings?? Any thing wrong with cash management?

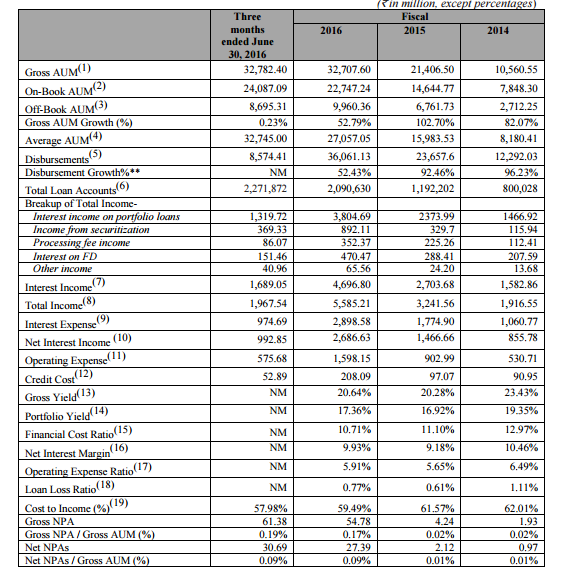

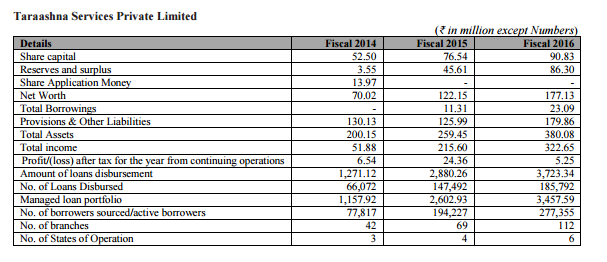

The QIP document is uploaded, great read. Couple of interesting tables below. Tarashana numbers look great but their profits seem to have dipped in FY16. I am assuming its because promoters took a big salary hike or paid a big dividend before the merger.

http://www.satincreditcare.com/pdf/le_imp/Satin_Creditcare_Network_Limited_Placement_Document.pdf.

2 Likes