Deccan cement looks the cheapest on ev / installed capacity. 550cr for 2.3 mtpa.

In cement space, we are looking into KCP, Sagar Cements and NCL Industries and stuff like that. None of these are actually advice to buy or sell, we are just looking into it and in some we have positions. Since we do not trade, we will hold it for a longer term.

by @aveekmitra

Read more at:

//economictimes.indiatimes.com/articleshow/68153808.cms?utm_source=contentofinterest&utm_medium=text&utm_campaign=cppst

2 Likes

Sagar Cement up on robust cement sales for the month of May 2019

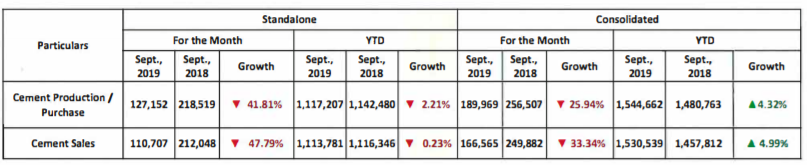

Cement Production up 12.91%

Cement Sales up 13.29%

Good Results

some CONCRETE talks

https://www.cmaindia.org/cement-industry/concrete-talks/

AND AN OLD ESSAY

DISC: Not invested but watching

It seems a good sign for the company.

1 Like

Sagar cements seems to have worst year in past 7-8 years, OPM at low of 7% as compared to 12%-14% average OPM. With fall in crude prices and moderate corrections in fuel cost, we can expect the margin to inch higher from here. The company is trading at EV/t of around $50-$60, as compared to $100/t replacement cost.

Disclosure: Invested, not a recommendation, only an opinion.

1 Like

Buy a stock having good management , low on speculation , having good long term prospect , available at low valuation ( historical and sector) and time when headwinds are high - Sagar cements is fit in all criteria. Even premji fund has bough 265 per share and today its available 15% discount to that.

I was holding this from 400 levels pre split and left the bus when it reached 1100 levels. Whole cement sector is a laggard. Valuation of stock looks fair in near term